|

Title: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: jimbobway on December 05, 2012, 07:19:38 PM So housing is another market not commonly discussed in the Speculation forum but I thought I'd reveal some things that have been happening. Earlier this year housing prices were really low. The fed decided to lower interest rates, which made it easier to borrow money to buy homes. In San Diego from around March to December the housing inventory has been steadily dropping because people have been buying. Because there is now a lower supply of homes the prices of the homes have now gone up. (This is basic supply and demand logic.)

It appears housing prices will continue to go up if the supply of homes continues to decrease. But, there are some conspiracy theories out there. One theory is that banks could be holding onto foreclosed homes and not selling them, thus keeping the supply low. Some people are theorizing that there could be a flood of foreclosed homes on the market next year when Obama goes back into office. (This same theory was mentioned early this year but it never materialized near the end of the year.) So, will the housing market continue to inflate? Or, will there be a flood of homes put on sale next year? What is going on here? Speculate! Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: adamstgBit on December 05, 2012, 07:44:20 PM well if the banks are holding to artificially increase the price of homes, they will continue to do just that... so no worries there

I guess it all depends on whether or not the economy recovers. if it recovers, then people will continue to pay their mortgages and more and more people will be buying homes, even if the interest rates rise a little. If the economy doesn't recover, and people start to default on their homes once again, this will create deflation. If deflation happens, paying the mortgage will become increasingly difficult, making even more people default, creating even more deflation! if the government tries to combat deflation by printing money like crazy, that wont help because cost of living will increase, and home owners will be no better off. so everything hangs by a thread as we wait for the economy to recover. did i get it right? lol Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: adamstgBit on December 05, 2012, 08:00:15 PM You can still buy a house for a dollar (http://quezi.com/15889)! Ill Buy them all! Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: myself on December 05, 2012, 08:06:58 PM if you want to get a house at a low price better use tax lien certificates that to buy one, the risk reward is awesome

Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: Qoheleth on December 05, 2012, 08:12:49 PM One theory is that banks could be holding onto foreclosed homes and not selling them, thus keeping the supply low. That's not a theory, that's common sense. If they put everything they have on the market at once, they'd flood it and recoup pennies on the dollar instead of dimes. Better to empty their queue at steady, careful pace.(Of course, that means they won't flood the market next year either.) Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: smoothie on December 05, 2012, 08:27:55 PM The inventory is only low because the banks that own the majority of the bad asset homes are keeping them off the market to help keep the prices propped up.

Nuff said. Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: SgtSpike on December 05, 2012, 08:34:14 PM You can still buy a house for a dollar (http://quezi.com/15889)! Not in Oregon! :(What time period are we speculating on? If the Fed is holding interest rates low and essentially re-inflating the bubble (and probably stimulating the housing market through inflation of the currency) then short - medium term prices would probably rise, but they can't artificially hold rates low forever can they? Well perhaps they can if the Fed just keeps expanding the money supply, but that is unsustainable. Long term when rates inevitably rise and /or the economy weakens then more people will be underwater on their mortgages and supply will rise causing prices to fall. But if the "normal" state of the economy is one of inflation (3%), then when we achieve that inflation rate again, can you really call it a bubble?Regardless, these waves of booms and busts seem to be a normal part of the economy. A way of self regulating and testing the boundaries. I don't think we'll see another recession as bad as this one for a while, but you never know... it could happen. I think many people (with exception of the government) have learned their lesson about taking on too much debt with this 4 years of lowered incomes. Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: Comodore on December 05, 2012, 08:43:21 PM We will see extreme lows in real terms. In terms of nominal values... hahaha helicopter Bernanke

Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 05, 2012, 08:52:12 PM http://www.nytimes.com/2012/12/02/business/in-an-fha-checkup-a-startling-number.html?emc=eta1&_r=1&

Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: SgtSpike on December 05, 2012, 10:10:36 PM http://www.nytimes.com/2012/12/02/business/in-an-fha-checkup-a-startling-number.html?emc=eta1&_r=1& Interesting article. I'm an FHA borrower myself (big mistake), and recently refinanced my home to take advantage of much better loan rates. When we bought in late 2008, the mortgage insurance cost was about $50/month. When we refinanced, that went up to $150/month. Yikes! On the upside, the difference in interest rate still made it a worthwhile deal, given that we pay almost $200 less per month and about $50 more per month is going to principle. It just sucks to have that $150 tied up as well, because that could be an extra $150/month in our pocket (and for 5 years, even if we pay off more than 25% of the loan in that time!). Oh well...Also, lol @ FHA... go figure, you loan to people with sub-600 credit scores and they default at a very high rate! ::) Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 06, 2012, 01:44:48 AM http://www.nytimes.com/2012/12/02/business/in-an-fha-checkup-a-startling-number.html?emc=eta1&_r=1& Interesting article. I'm an FHA borrower myself (big mistake), and recently refinanced my home to take advantage of much better loan rates. When we bought in late 2008, the mortgage insurance cost was about $50/month. When we refinanced, that went up to $150/month. Yikes! On the upside, the difference in interest rate still made it a worthwhile deal, given that we pay almost $200 less per month and about $50 more per month is going to principle. It just sucks to have that $150 tied up as well, because that could be an extra $150/month in our pocket (and for 5 years, even if we pay off more than 25% of the loan in that time!). Oh well...Also, lol @ FHA... go figure, you loan to people with sub-600 credit scores and they default at a very high rate! ::) well that's the thing. everyone thinks the banks are lending again but they're not. they only have lent to students whose debts are guaranteed by Sallie Mae (gov't) and lent to homebuyers who qualify for Fannie/Freddie/FHA (gov't). they never hold the loans cuz they know they're bad and only want the fees generated by the loans. personally, i think its a very risky time to buy a house b/c interest rates are at all time lows. if you qualify and i doubt you will if you can't get a gov't subsidized loan, make sure its fixed rate otherwise when interest rates rise you will be crushed. the reason prices have been rising is that the banks have been keeping foreclosures off the market and any price rise will see an increased release of these foreclosures/REO's back onto the market acting as a price suppression mechanism that's built in. also, much of the buys made the last few years have been cash buys from big investors whose goal is to flip these things when the price is right; if it ever gets there. http://www.acting-man.com/?p=20728 http://www.acting-man.com/?p=20622 Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 06, 2012, 02:03:40 AM btw, the author of those 2 articles i posted above is Ramsey Su; from San Diego.

Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: jimbobway on December 06, 2012, 02:05:10 AM well that's the thing. everyone thinks the banks are lending again but they're not. they only have lent to students whose debts are guaranteed by Sallie Mae (gov't) and lent to homebuyers who qualify for Fannie/Freddie/FHA (gov't). they never hold the loans cuz they know they're bad and only want the fees generated by the loans. personally, i think its a very risky time to buy a house b/c interest rates are at all time lows. if you qualify and i doubt you will if you can't get a gov't subsidized loan, make sure its fixed rate otherwise when interest rates rise you will be crushed. the reason prices have been rising is that the banks have been keeping foreclosures off the market and any price rise will see an increased release of these foreclosures/REO's back onto the market acting as a price suppression mechanism that's built in. also, much of the buys made the last few years have been cash buys from big investors whose goal is to flip these things when the price is right; if it ever gets there. http://www.acting-man.com/?p=20728 http://www.acting-man.com/?p=20622 Thanks for the links. I wish I had hard data on what the bulk buyers and banks are holding. All of this could be speculation. It is possible there is low inventory because people don't want to sell for a loss? Everyone is waiting for the market to go back up and home prices to go up. When the market does go back up then will everyone sell at the same time? Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 06, 2012, 02:09:41 AM well that's the thing. everyone thinks the banks are lending again but they're not. they only have lent to students whose debts are guaranteed by Sallie Mae (gov't) and lent to homebuyers who qualify for Fannie/Freddie/FHA (gov't). they never hold the loans cuz they know they're bad and only want the fees generated by the loans. personally, i think its a very risky time to buy a house b/c interest rates are at all time lows. if you qualify and i doubt you will if you can't get a gov't subsidized loan, make sure its fixed rate otherwise when interest rates rise you will be crushed. the reason prices have been rising is that the banks have been keeping foreclosures off the market and any price rise will see an increased release of these foreclosures/REO's back onto the market acting as a price suppression mechanism that's built in. also, much of the buys made the last few years have been cash buys from big investors whose goal is to flip these things when the price is right; if it ever gets there. http://www.acting-man.com/?p=20728 http://www.acting-man.com/?p=20622 Thanks for the links. I wish I had hard data on what the bulk buyers and banks are holding. All of this could be speculation. It is possible there is low inventory because people don't want to sell for a loss? Everyone is waiting for the market to go back up and home prices to go up. When the market does go back up then will everyone sell at the same time? that certainly is a theory that is circulating. just to present the other side of the story to be fair; Calculated Risk is bullish on housing even though i don't agree. lots of clues can be gleaned from the stock market. yes, i think we're in the process of rolling. Toll Brothers had their earnings call yesterday at 11:00 AM and the stock went straight down a total of about 7% since by the end of today. Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: SgtSpike on December 06, 2012, 06:25:23 AM http://www.nytimes.com/2012/12/02/business/in-an-fha-checkup-a-startling-number.html?emc=eta1&_r=1& Interesting article. I'm an FHA borrower myself (big mistake), and recently refinanced my home to take advantage of much better loan rates. When we bought in late 2008, the mortgage insurance cost was about $50/month. When we refinanced, that went up to $150/month. Yikes! On the upside, the difference in interest rate still made it a worthwhile deal, given that we pay almost $200 less per month and about $50 more per month is going to principle. It just sucks to have that $150 tied up as well, because that could be an extra $150/month in our pocket (and for 5 years, even if we pay off more than 25% of the loan in that time!). Oh well...Also, lol @ FHA... go figure, you loan to people with sub-600 credit scores and they default at a very high rate! ::) well that's the thing. everyone thinks the banks are lending again but they're not. they only have lent to students whose debts are guaranteed by Sallie Mae (gov't) and lent to homebuyers who qualify for Fannie/Freddie/FHA (gov't). they never hold the loans cuz they know they're bad and only want the fees generated by the loans. personally, i think its a very risky time to buy a house b/c interest rates are at all time lows. if you qualify and i doubt you will if you can't get a gov't subsidized loan, make sure its fixed rate otherwise when interest rates rise you will be crushed. the reason prices have been rising is that the banks have been keeping foreclosures off the market and any price rise will see an increased release of these foreclosures/REO's back onto the market acting as a price suppression mechanism that's built in. also, much of the buys made the last few years have been cash buys from big investors whose goal is to flip these things when the price is right; if it ever gets there. http://www.acting-man.com/?p=20728 http://www.acting-man.com/?p=20622 It's a great time to buy because of the interest rates. Has nothing to do with the risk of ARM's - that's a bad idea regardless when you buy. Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: Kluge on December 06, 2012, 07:06:28 AM Not really sure why banks keeping foreclosures off the market would be considered a "conspiracy theory."

I spent a long, long time looking at short sales and foreclosures before settling a few months ago. Ask any realtor why the Hell banks are letting $300k+ homes suffer severe water damage, house abuse by gangs making foreclosures a hangout, and other effects of nobody giving a damn. In one house I looked at, it would've been worth well over $200k if the bank had bothered to maintain the house since it was foreclosed on over two years ago. Instead, it went into disrepair and was listed at a price of $25k, about the value of the land (the water damage was so bad, the subflooring had given out in some places during previous showings). I also don't see why banks wouldn't consider these houses as more of liabilities than assets given how many don't appear to even bother maintaining their properties. I'd be pretty eager to get a $150k current-value house with $6k/yr in maintenance and taxes far away from my hands, even if there was a $200k amount in default, rather than banking on a kind of supply-reducing oligopoly on the US housing market working out. Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: johnyj on December 06, 2012, 10:11:47 AM ... but they can't artificially hold rates low forever can they? Well perhaps they can if the Fed just keeps expanding the money supply, but that is unsustainable. Fed is printing money to buy those foreclosed homes (or indirectly, mortgage backed securites), and they keep it as a reserve These homes will worth a little if all goes to the market. But, like FED could destroy money as well, when the economy is fully recovered, they could sell these homes at a later time to cool down the economy (just like they sell the government bonds, home or government bonds, which has higher credit?), Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 06, 2012, 04:52:18 PM http://www.nytimes.com/2012/12/02/business/in-an-fha-checkup-a-startling-number.html?emc=eta1&_r=1& Interesting article. I'm an FHA borrower myself (big mistake), and recently refinanced my home to take advantage of much better loan rates. When we bought in late 2008, the mortgage insurance cost was about $50/month. When we refinanced, that went up to $150/month. Yikes! On the upside, the difference in interest rate still made it a worthwhile deal, given that we pay almost $200 less per month and about $50 more per month is going to principle. It just sucks to have that $150 tied up as well, because that could be an extra $150/month in our pocket (and for 5 years, even if we pay off more than 25% of the loan in that time!). Oh well...Also, lol @ FHA... go figure, you loan to people with sub-600 credit scores and they default at a very high rate! ::) well that's the thing. everyone thinks the banks are lending again but they're not. they only have lent to students whose debts are guaranteed by Sallie Mae (gov't) and lent to homebuyers who qualify for Fannie/Freddie/FHA (gov't). they never hold the loans cuz they know they're bad and only want the fees generated by the loans. personally, i think its a very risky time to buy a house b/c interest rates are at all time lows. if you qualify and i doubt you will if you can't get a gov't subsidized loan, make sure its fixed rate otherwise when interest rates rise you will be crushed. the reason prices have been rising is that the banks have been keeping foreclosures off the market and any price rise will see an increased release of these foreclosures/REO's back onto the market acting as a price suppression mechanism that's built in. also, much of the buys made the last few years have been cash buys from big investors whose goal is to flip these things when the price is right; if it ever gets there. http://www.acting-man.com/?p=20728 http://www.acting-man.com/?p=20622 It's a great time to buy because of the interest rates. Has nothing to do with the risk of ARM's - that's a bad idea regardless when you buy. that's really not true at all. those who speculated on homes during the run up who had ARM's have been "bailed out" essentially by the rest of us as Ben has lowered interest rates over the last 4 yr. their monthly payments have actually decreased allowing many to stay in their homes. look at municipalities that were duped into buying ARS's which were essentially bets that interest rates would rise. these were sold by Wall St as a hedge against the muni bonds which municipalities sold. Jefferson County and many others have lost millions if not billions on these bets. a conspiracy theorist would say that Wall St sellers of these instruments knew that Ben would be there with the free money to bail them out via further suppression of rates as the bubble popped. they have made fortunes at the expense of the municipalities. Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 06, 2012, 04:55:32 PM Not really sure why banks keeping foreclosures off the market would be considered a "conspiracy theory." I spent a long, long time looking at short sales and foreclosures before settling a few months ago. Ask any realtor why the Hell banks are letting $300k+ homes suffer severe water damage, house abuse by gangs making foreclosures a hangout, and other effects of nobody giving a damn. In one house I looked at, it would've been worth well over $200k if the bank had bothered to maintain the house since it was foreclosed on over two years ago. Instead, it went into disrepair and was listed at a price of $25k, about the value of the land (the water damage was so bad, the subflooring had given out in some places during previous showings). I also don't see why banks wouldn't consider these houses as more of liabilities than assets given how many don't appear to even bother maintaining their properties. I'd be pretty eager to get a $150k current-value house with $6k/yr in maintenance and taxes far away from my hands, even if there was a $200k amount in default, rather than banking on a kind of supply-reducing oligopoly on the US housing market working out. if you were a bank and were faced with going thru the normal foreclosure process and losing money in a declining market vs. keeping those homes on your books and getting bailed out by the Fed at mark to model prices (inflated) which would you do? who cares about the homes anymore? they've essentially been bought by the rest of us via the debasement of our currency. Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 06, 2012, 05:29:13 PM https://bitcointalk.org/index.php?topic=68655.msg1382461#msg1382461

Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: jimbobway on December 06, 2012, 05:41:22 PM https://bitcointalk.org/index.php?topic=68655.msg1382461#msg1382461 Those graphs show mortgage debt growth going down and student loan debt growth skyrocketing. So less people are borrowing to buy a house...which means possibly...institutions are buying with cash? Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 06, 2012, 05:45:54 PM https://bitcointalk.org/index.php?topic=68655.msg1382461#msg1382461 Those graphs show mortgage debt growth going down and student loan debt growth skyrocketing. So less people are borrowing to buy a house...which means possibly...institutions are buying with cash? yes, but look at those 2 articles i posted from Acting Man. its a huge gamble for them and most likely not gonna pay off. student loan growth is in a bursting bubble. i think its a particular predatory form of lending by banks in that their objective is to enslave the younger generation into a lifetime of debt servitude. i will never let this happen to my sons and all you young guys should be fighting like hell against this. Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 07, 2012, 04:11:49 AM the latest from Ramsay: http://www.acting-man.com/?p=20839

Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 07, 2012, 06:07:24 AM here are some very practical reasons to wait at least until after the 1st of the year to find out what's gonna happen: http://ml-implode.com/viewnews/2012-12-05_FiscalCliffandTaxChangesaThreattotheHousingMarket.html

Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: Melbustus on December 07, 2012, 06:54:54 AM the latest from Ramsay: http://www.acting-man.com/?p=20839 Why is there a paypal donation button but no bitcoin donation button on that site? Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 09, 2012, 06:01:41 AM http://www.mortgagenewsdaily.com/12072012_mortgage_interest_deduction.asp

Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: Elwar on December 09, 2012, 05:03:25 PM Banks are holding those homes because selling them will result in a loss on their books.

If the bank has a loan on a house valued at 300k and the owner forecloses, their books show that they now have a 300k asset. With the drop in the market that house may now be valued at 100k or less. If banks dropped all of their foreclosure homes, their earnings reports would show huge losses and scare off investors making their stocks plunge. So keeping the properties at their inflated value is to their advantage even if the house crumbles into a heap of wood. It is a flaw of only appraising a home's value at the time of purchase. If there were yearly appraisals these homes would be dumped left and right. Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 09, 2012, 06:25:29 PM Banks are holding those homes because selling them will result in a loss on their books. If the bank has a loan on a house valued at 300k and the owner forecloses, their books show that they now have a 300k asset. With the drop in the market that house may now be valued at 100k or less. If banks dropped all of their foreclosure homes, their earnings reports would show huge losses and scare off investors making their stocks plunge. So keeping the properties at their inflated value is to their advantage even if the house crumbles into a heap of wood. It is a flaw of only appraising a home's value at the time of purchase. If there were yearly appraisals these homes would be dumped left and right. yes, the drop in housing values should've forced a mark to market event thus blowing a huge hole in most banks balance sheets on the asset side thus forcing bankruptcy and clearing out the bad lenders. but NO, Ben has to step in a buy all those bad assets, bring them into the Fed under the guarantee of the US taxpayer who is responsible for paying those things off if and when they default, paying in terms of the minimal debasement of the USD by taking the balance from $800B to $2.8T, and the continuation of the same institutional corruption that should've been cleared out by BK's. thus we get the wipeout of the middle class with the elite getting their incomes shoved ever higher and the lower classes seeing their incomes get shoved ever lower. an elongated hourglass configuration. Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 10, 2012, 01:10:04 AM CITI'S MATT KING PRESENTS: 'The Most Depressing Slide I've Ever Created'

http://www.businessinsider.com/matt-kings-most-depressing-slide-ever-2012-12 https://i.imgur.com/0Tc7L.jpg Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: adamstgBit on December 10, 2012, 01:51:16 AM I bought my condo for 160 i could probably sell it for 180 (only 1.5 year later), and now the astronomical prices for homes on the Island of Montreal is forcing more people to look in my area, prices are sure to BOOM some more!

housing always goes up Up UP, no bubble here ;D Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: SgtSpike on December 10, 2012, 05:25:10 PM According to Zillow, housing prices in Eugene have risen from their low of $191k average in February 2012 to $197k as of October 2012. Not much of an increase, but it is an increase. The peak was $250k in August 2006.

Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 10, 2012, 07:25:34 PM http://www.zerohedge.com/news/2012-12-10/real-estate-bottom-or-head-fake

Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: cypherdoc on December 10, 2012, 09:39:51 PM this is a fantastic article to read about California housing: http://www.doctorhousingbubble.com/home-equity-net-worth-figures-us-housing-debt-home-equity-near-record-lows/

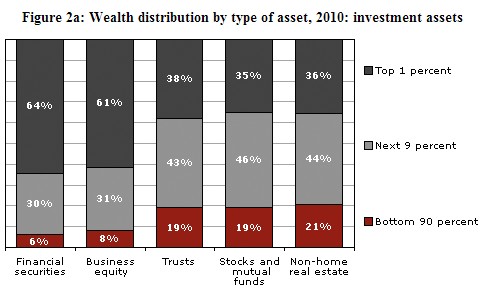

from the article, look at this: http://www.doctorhousingbubble.com/wp-content/uploads/2012/12/wealth-held-by-bracket.png what it shows is that 90% of the American ppl own only 6% of the financial assets in this country and specifically only 19% of stocks and mutual funds. the vast majority of QE has gone to reinflate those assets and have done much less for housing (the average American's source of wealth). remember what i said about how a stock mkt crash is something only Wall St and the elite should fear? well, this proves that i'm right, and if anything, a stock mkt "crash/cleansing/deflation" will only level the playing field. it is not something to be feared, but in fact, encouraged. Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: trogdorjw73 on December 10, 2012, 10:53:36 PM remember what i said about how a stock mkt crash is something only Wall St and the elite should fear? well, this proves that i'm right, and if anything, a stock mkt "crash/cleansing/deflation" will only level the playing field. it is not something to be feared, but in fact, encouraged. The problem is that all of the wealthy elite that you reference control everything else in various ways. They'll get their money, regardless, so a crash serves to shake up the system and then the poor and middle class end up paying for it. It's complete lunacy to think redistribution of wealth is anything but a power grab that will utterly kill all production long term.Or put another way, the top 10% are the ones doing all the hard work that the 90% don't want to do. You'll rise to your level of problem solving, so if your skill set is, "I know how to earn enough money so I can pay for my car and mortgage", that's what you'll get paid. If you can help solve the problems of a large corporation, that's what you'll get paid to do. And sitting around playing the blame game like the 95% are wont to do isn't going to help their situation. Instead, they should be reading quality books (e.g. The Slight Edge (http://www.amazon.com/gp/product/193594486X/ref=as_li_ss_tl?tag=dosk-20), Seven Habits of Highly Effective People (http://www.amazon.com/gp/product/0743269519/ref=as_li_ss_tl?&tag=dosk-20), etc.), seeking to improve their education, exercising, eating healthier foods, paying off debt, etc. -- but while those things are all possible for anyone to do, they're even easier not to do. Not doing them today won't hurt you, but long-term you'll end up in the pits. (Note: The general content of this post is inspired by reading The Slight Edge. I highly recommend the book; people need to stop looking for quick solutions and focus on improving Number One. Read 10 pages of such a book each dead -- e.g. instead of surfing Internet forums -- and by the end of the year you've read 3650 pages of quality self-improvement material. There's no way you could do that for a year and not come out a better person!) Title: Re: Housing Market Inventory At Extreme Lows [Dec 2012] Post by: SgtSpike on December 10, 2012, 11:12:00 PM Good post trogdor, I agree, at least to the extent of assuming an uncorrupted environment.

"I've never understood why it's greed to want to keep money you've earned but not greed to want to take somebody else's money. Certainly, many of the elite class have become quite adapt at stealing monies from other people, but that doesn't make the entire upper class greedy. Many of them are also very legitimate workers and key players in the companies or roles they occupy. Is anyone considering impending hyper-inflation as a potential cause for home prices increasing? They've been printing quite a lot of money lately... |

{kind=link}

{kind=link}