|

Title: Why do bitcoin futures contracts trade at a premium to the index/spot price? Post by: bitcoinmarkets on March 10, 2016, 01:14:02 PM A lot of people are now starting to trade Bitcoin futures at sites like OKCoin (http://www.okcoin.com), BitMEX (https://www.bitmex.com/register/RrmvSe), and CryptoFacilities (http://www.crypto-facilities.com) . One of the first questions people have when they start trading futures is: why are the prices higher than the spot? How does this work exactly? Here's a little explanation to help you understand the simple maths behind it.

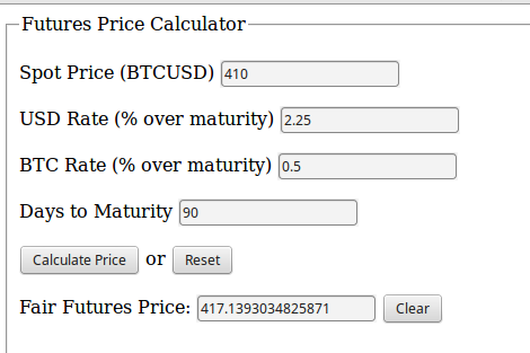

Some Finance 101 (or maybe 102) shows how you can calculate what the "fair value" of these contracts would be, given no arbitrage being possible. You can replicate the future value of a bitcoin in USD by borrowing USD and buying BTC, so the fair price is derived from the excess of USD borrowing rate vs BTC lending rate. The price of the Forward then should not deviate far from this level or arbitageurs close it. This material is inspired partially from Arthur at BitMEX's arbitrage trading YouTube presentation here. The efficient pricing of Futures contracts theoretically in finance is then governed by this formula: F = S * ( 1 + Rh * t ) / (1 + Rf * t) Where F = the price. S = spot price (Rh/Rf) Rh = home interest rate Rf = foreign interest rate t = days / 365 Just as an example, using Bitfinex swap markets as the baseline, at a spot rate right now of $410 , USD rate of 9% APY and BTC rate of 2% APY, and a quarterly maturity of 90 days. Home = USD, Foreign = BTC Its not exact, but we will use as a simple rate for quarter on USD at 2.25% and 0.5% on BTC. Here is a simple Bitcoin Futures Fair Price Calculator which you can plug these values into and you will get: http://www.bitcoinfuturesguide.com/fair-price-calculator.html http://www.bitcoinfuturesguide.com/uploads/6/4/6/5/64656757/4538079.png?532 Using this metric, the expected premium then on the OKCoin quarterly expiring in 90 days will be about $8, and if spot is still around $410 its price will be around $418. This is what we expect the OKCoin premium to be in then based on this model. You can read more detailed explanation here: http://www.bitcoinfuturesguide.com/bitcoin-blog/why-do-bitcoin-futures-prices-tend-to-have-a-premium-to-the-index-or-spot-value Title: Re: Why do bitcoin futures contracts trade at a premium to the index/spot price? Post by: tobacco123 on March 10, 2016, 01:45:42 PM Thanks for sharing this information. However, it seems very complex to a layman like me.

I guess this is a good way to invest but I will just stick to buying the bitcoin directly. Title: Re: Why do bitcoin futures contracts trade at a premium to the index/spot price? Post by: Jet Cash on March 10, 2016, 01:48:56 PM How will negative interest rates affect this?

Title: Re: Why do bitcoin futures contracts trade at a premium to the index/spot price? Post by: HowDoge on June 30, 2016, 07:19:47 PM In a negative interest rate environment you are effectively charged when using or holding your currency. In such a case the desirability of high mobility, low fee currency becomes far more attractive. I'd expect this to translate to higher premiums.

After all, why would you want to convert back to fiat if its going to cost you to hold it or when putting it to use ? |

{kind=link}