|

In reply to a comment upthread, the reason TPTB wanted a Hillary victory was that

if that had happened, the MSM would have "Brahms Lullaby" on a continuous loop.

With Trump, we get "The Ride of the Valkyrie", and the last thing TPTB want is a

population capable of critical thinking. That said, with only two candidates getting

95% of the vote, the situation is contained.

I believe the phrase is "This isn't their first rodeo".

|

|

|

|

|

Some notes on the Social Contract, and our present condition.

I'm going to begin with something of a workaround. I'll posit that,

to the extent that God exists, he created an economic system such that

the individual had only to work in his own informed best interests to

create the greatest common good. That allows the Invisible Hand, and

some basic concepts of the Social Contract to coincide.

Some would argue that in practice, this doesn't work, that the mass

of the population gives up the burden of becoming informed and even

thinking for themselves in return for protection and a structured

existence. Put simply, if the economy produces four percent per annum

surplus goods, and two percent goes to the elite and the peasants

share the rest, everybody is, if not happy, perhaps satisfied with

the contract.

Since in theory all citizens in an economy participate equally, it

could be said that the society tolerates theft by the elite up to a

level where it becomes unacceptable.

This limit of tolerance is somewhat narrower than might be supposed.

Historically, rates between zero and one percent real GDP growth are

much more common than the four percent or greater growth experienced

by most of the people alive today. The rising tide lifts all the boats.

It's reasonable to suppose that our present condition may not last

much longer, but before pursuing that, it's worth thing about where we

are now. We've had perhaps a generation, perhaps more, that has never

seen the need to challenge the established order, and the established

order, the Elite, TPTB, have never been called to account for their

privilege.

Such an arrangement encourages corruption. Such arrangements encourage

the exclusion of "squeaky clean" candidates for promotion. Corruption,

carried to extreme, and given time, may ultimately produce a kakistocracy.

Once established, such an arrangement may be impossible to remove absent

a revolution.

Accumulation of wealth gradually, over many years increases inequality

in the society. Strategies are devised to conceal or justify the theft,

but a city built on a hill cannot be hid. Those closest to it can be bought

off but the elite will find they cannot buy off enough sectors of society

without causing the fabric of that society to tear, or if they compromise

their income from monopolies of scale and captured legislatures, they fail.

It is tempting to dive into one of the many topics that should immediately

spring to mind. But I have a different question. What happens when the

play changes into a zero-sum game? Or put differently, when the elite

owns everything, who gets to decide what happens?

That's a rhetorical question, obviously. Asking it merely shows that we

find ourselves in unfamiliar territory. If you doubt this, would you

believe blatant theft from the poorest people on this planet by their

elected government?

|

|

|

|

|

Let me begin by a recap on a few things. The Clinton campaign initially targetted

Sanders and Trump. They wanted Trump as the Republican opponent as they expected

that he would be even more disliked than Hillary Clinton. Hence they pushed their

media contacts to give Trump airtime and encouragement. They sucked Sanders in

and ensured that the polling system was rigged to favour Hillary. Thanks to

some insiders and to Wikileaks much of that story is public knowledge.

You might wonder why they thought that selecting a candidate a majority of their

supporters wouldn't vote for was a good idea, but step back a bit from that idea.

Their customers are the people who give them money. And their customers wanted

Hillary. They thought they had enough control to pull it off. When Sanders

conceded and supported Hillary, and when Trump won the Republican nomination

while shredding that Party, confirmation bias kicked in. You know the rest of

that story.

Before I get to the next point, I'll mention that I don't have a dog in this fight.

People sometimes equate racism with fascism. While the two tend to go together,

Fascism is capitalism writ large, Mussolini defined Fascisim as Corporatism. It's

when the Corporate lobby decides who gets to govern and it doesn't care what laws

are passed so long as the profits keep increasing. If you're a neoliberal and want

to know what a fascist looks like, begin by taking a long hard look in the mirror.

That, however, misses my point. In a US election that fielded the two most disliked

contenders in its history, third party candidates were crushed. Further, nobody

seems to think this might be either an issue or indeed a problem. The US does

not hear policies or views on issues out of favour with the main stream media.

Hold that thought.

Currently, the Government of India is in the midst of a crisis brought about by

either malice or by mismanagement of their paper currency, perhaps both. In

India, possession of either gold or bitcoin is probably a good thing. From what

I've read, a subtle shift has taken place, and the Indian Government seems

to have shifted the burden of proof of ownership of assets onto the citizen.

If you can't prove it's yours, it's the Government's and you are a criminal.

It may be unintended, but that seems to be how it is being played.

So what is the systemic risk of owning gold elsewhere? Here I part company with

Jim Rickards. Mr Rickards suggests that the US executive order of 1933 making

gold contraband will not recur. The free market in gold prevents the accumulation

of seniorage, thus any attempt to seize private gold would result in the price of

gold rising rapidly, frustrating the intended goal.

But first, history suggests that TPTB will move their gold to a safe location, as

in 1933, hence that constraint on government action can be discounted. Secondly,

the preponderance of paper gold in the market suggests that the ratio of physical

gold to claims for gold could run close to three figures. That suggests that a

mechanism exists which could be used to suppress the price of physical gold in an

"emergency."I'm not saying that such action will happen, merely that Mr Rickards

is less cynical than I.

I'll mention that Mr Rickards and I agree on one thing. There is financial

asymmetry between western financial markets and Russia. If a cyberwar breaks out

the West has much more to lose than Russia. The same could be said regarding

the next financial crisis.

Much depends on confidence in fiat currencies, and that depends on perceptions.

Those, in turn, are influenced by the main stream media, and recent events have

shown that the press cannot be relied upon to provide fair unbiased reporting.

Which leaves bitcoin as perhaps the last currency standing.

|

|

|

|

An Economist tells a joke: Two economists are walking down a street. They walk past a pile of horse shit. The first economist says "I'll give you $1,000,000 to put a horse ball between two bits of orange peel and eat it." The second economist accepts and gets a cheque for $1,000,000. They walk on and see some dog poo. The second economist says "I'll give you $1,000,000 to put some dog poo between two bits of orange peel and eat it." The first economist accepts and gets a cheque for $1,000,000. The two economists laugh when they realize that their street cleaning has increased GDP by $2,000,000. Hillarious. But there's a deeper point here. What has value? Does prostitution really raise GDP? Drug-dealing? Are these different in the economy to other activities - hairdressing, for example? or pedicures? And if these are legitimate in the economic arena, what does that say about other forms of crime? for example, financial fraud? Where does the economy draw the line between the IMF's GDP forecasts? http://www.zerohedge.com/news/2015-06-21/greek-gdp-shocking-reality-vs-imf-forecasts-and-who-blame-greek-implosionor earnings forecasts? http://www.zerohedge.com/news/2016-10-26/earnings-magic-exposedand a ponzi bubble in swamp land prices in Florida? http://www.nytimes.com/1986/12/07/business/archives-of-business-a-rogues-gallery-charles-ponzi-a-pyramid-of-postage.htmlIs value nothing more than the net present value of some future event? Money, "It's all about the Benjamins", was at one time convertible into gold, ( https://www.youtube.com/watch?v=mnvrKdx5Mrs&feature=youtu.be - from corbett report episode292) though there were more claims to gold than gold in the bank vault. Earlier still, there was a 1:1 ratio at some time. And the origin of all this? in ancient Mesopotamia, when barley was money, silver was the unit of account. One shekel of silver was a claim on one gur of barley or a related measure. http://www.ishtartv.com/en/viewarticle,35322.htmlIt was coded into the law. Serious economics in those days. Here, today, there may be an equivalence between Value and Schrodinger's Cat. It's that moment when Investor->Bagholder, the moment when value may cease to exist. Until that moment Investor and Bagholder can coexist in someone's consciousness. But suppose "we" include financial fraud into our calculation of GDP. And, I'd argue that the banker's promotion of the idea that they are essential for our survival is the biggest fraud ever perpetrated on the public, hence there is huge potential there. What happens when that "value" drops out of existence? That moment when fraud gets "found out"? Hold off on that thought for a moment. More fraud Sir? What's not to like? It's GDP growth, that goal of formation kowtowing. And just the sort of thing that seems sensible when stock markets rise on bad news. It's the ultimate something for nothing, it's something for less than nothing. Still ...... "Too much of a good thing can be wonderful." - Mae West [The above is opinion, not advice, and the underlying mathematics lacks rigour, but probably good enough for economics work] |

|

|

|

While looking up legislation on internet freedom, I found the following somewhat broad overreach: PROTECT IP Act of 2011 https://www.congress.gov/bill/112th-congress/senate-bill/968/text"(ii) the Internet site - conducts business directed to residents of the United States; and harms holders of United States intellectual property rights." OK, the bill got squashed, which is a story in itself, but then there's this: http://www.salon.com/2011/12/09/hillary_clinton_and_internet_freedom/"There are many people who can credibly claim to defend Internet Freedom; Obama officials are not among them - Glenn Greenwald" "But when ideas are blocked, information deleted, conversations stifled, and people constrained in their choices, the internet is diminished for all of us. What we do today to preserve fundamental freedoms online will have a profound effect on the next generation of users." "Those are the acts of a government and a State Department seeking to block access to and discussion of evidence of their own wrongdoing and to punish as criminals those who reported it." The above suggests that absent major political change in the USA, there'll be more of this, which brings me to the prospects for the US leadership contest. A couple of days ago there was a news video link between an journalist and what appeared to be a girl in "Aleppo", pleading for the International Community to no longer idly stand by and do nothing. At that point, I was reminded of many other victims of recent conflicts, and of Benghazi. If I've recalled correctly, even a direct line to the second most powerful person on this planet failed to get any effective action in the midst of the Benghazi firefight. Everybody makes mistakes, everybody has regrets about things they did or didn't do. The difference is in recognising the mistake for what it is and in the character growth that happens. "What difference does it make?" suggests this learning process is not in place for HRC, and it suggests no understanding of the military mindset. If I'm reading the runes correctly, at least some faction of TPTB is rethinking its constituency, and advocating change, but they may have a problem. It is this : "You're going to Jail" For that political change to happen, TPTB have to be sure that they aren't going to jail, and there's no way to ensure that, without a deal. And if anybody gets a deal, everybody gets a deal. And if everybody gets a deal, then for the internet, it's the same old, same old ... BTW, More on the Syrian refugees and the totalitarian-lite profiteering here: http://www.boilingfrogspost.com/2016/10/14/the-generators-agent-provocateurs-opportunists-of-the-refugee-crisis/ |

|

|

|

"I will do such things, What they are, yet I know not; but they shall be The terrors of the Earth." - King Lear, Scene IV That's how the old regimes see the approach of the new .... As we approach the abyss, their loss of control appears in many guises, from the European Union's desire to punish the UK for Brexit, to the USA's machinations in the Middle East. This week, a US General, a character straight out of Dr Strangelove, pointed out that declaring war on Syria, and Russia, was above his pay grade. That approximates where we are now, and it doesn't get much more terrifying than that. In other news, from elsewhere on the Titanic, soap and towels are being stolen from the washrooms .... https://www.thetruthseeker.co.uk/?p=139989"Top Bank Fraud Expert: ALL of the Big Banks' Profits Come from FRAUD" https://www.youtube.com/watch?v=Y_E35bbFP1EPhysician, heal thyself .... https://www.intellihub.com/bis-warns-china-is-imploding/"A key gauge of credit vulnerability is now three times over the danger threshold and has continued to deteriorate, despite pledges by Chinese premier Li Keqiang to wean the economy off debt-driven growth before it is too late." "While the BIS is making noise about China's GDP, government bonds and debt, it is failing to look at the U.S. and European Union, both of which are in far worse condition than China." For something really scary, look at Ireland's national debt, and then Ireland's GDP. No problem? Now look at Ireland's N Debt/GNP .... hmmmmm It's going to be a while before "The Terrors of the Earth" are revealed, and I doubt I can add much more to this thread until they appear, maybe not even then. So, time to start a new thread? ;-) PS: The latest news out of China is on the use of entangled photons for radar. That may have some implications for quantum computing, and for bitcoin. |

|

|

|

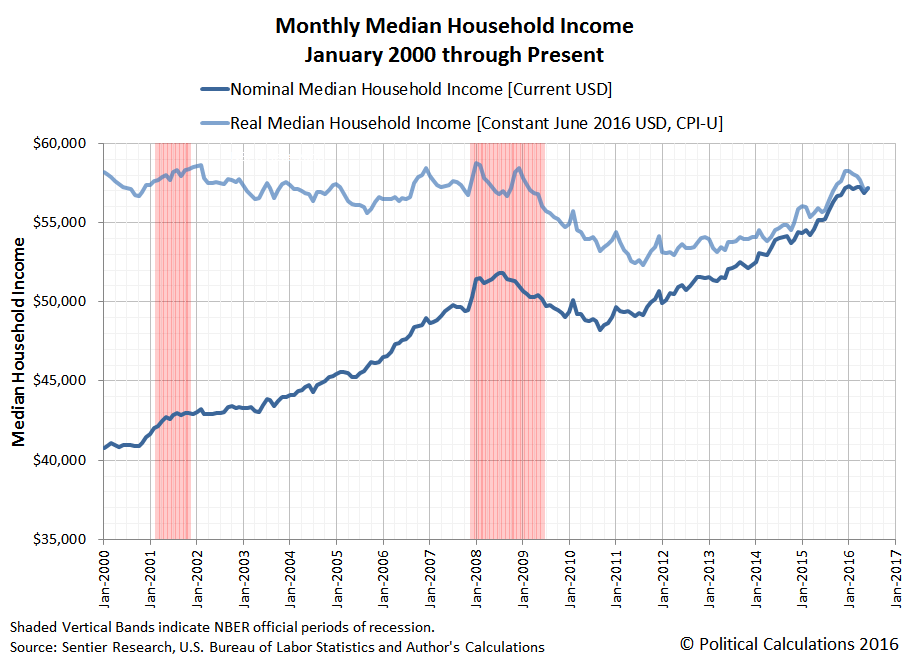

'The rule is, jam to-morrow and jam yesterday - but never jam to-day.' The Red Queen - Alice through the Looking Glass. Have you notice a dearth of year-on-year figures of late? Where almost always a month-on-month figure is multiplied by 12 in its place? That's because the facade is proving difficult to keep in place. So, when the US Census Bureau announced a 5.2% increase in real (inflation-adjusted) median household income, over the 2015 year, the absence of jam today got noticed. It may be, by a couple of lucky concidences, that what the Census Bureau said is actually true, but that's not the real story. Have a look at the graph here: http://politicalcalculations.blogspot.co.uk/2016/07/household-median-income-growth-stalling.html#.V9qh-SgrLARhttps://1.bp.blogspot.com/-DNWQIkH-h34/V5UANuO1WbI/AAAAAAAANyo/2AEDsV7_veM8tnAuSBr4Sme9pLltYR3WQCLcB/s1600/monthly-median-household-income-2000-01-thru-2016-06.pngNominal Median Household Income (Current US$) rose from $54,000 in mid 2014 to $57,000 in 2016, or about 5.5% over two years before allowing for inflation. Also here : http://www.declineoftheempire.com/2016/09/deconstructing-median-income-bullshit.htmlThere are many things that could be said about this and other attempts at perception management. Put simply, it's beginning to fail. If you gleefully thought that US inflation was going to take off next year amid rate rises by the FED, well, you just got punk'd by the US Census Bureau. I'll still hold to my forecast of five percent inflation at some time in 2017, though, just later in the 2017 year. All of which neatly ties up a loose end from a few weeks ago. Some other stuff that caught my eye this last week. "Chinese growth 'all but disappeared' amid economic restructuring, heavy flooding, factory closures ahead of G20 Complete absence¡ of y/y oil demand growth in 3Q16 China" And this: http://econimica.blogspot.co.uk/2016/06/global-peak-oil-demand-dead-ahead-but.html"To begin, I'll focus on the present consumers of 70% of the worlds crude, the OECD+China+Russia+Brazil. And if we check the annual change to their combined 0-64yr/old population (blue line in the chart below), 0-64yr/old population growth has decelerated 90% since the '88 peak and cumulatively turns to outright annual declines by 2019. The annual declines accelerate indefinitely from there. I also show total 0-64yr/old annual global growth (black columns) and 0-64 growth among the RoW or Rest of the World (red line)." I keep hoping I'm wrong, but the news just keeps coming. |

|

|

|

M-T "Everything falling into place?" OK maybe I need to work through this some more. This isn't a great example, but it is recent. http://www.zerohedge.com/news/2016-09-07/gdp-less-meets-eye"As one easily notices GDP on a per capita basis is more worrisome than when viewed on a total basis as in the first two graphs. The economic growth rate per person is currently below one half of one percent. More concerning, it is below levels seen during the great financial crisis in 2008 and it is still trending lower. This graph confirms our macroeconomic concerns and helps explain, in part, why so many U.S. citizens feel like they are being left behind. Factor in that many of the economic spoils are not evenly distributed, as assumed in this analysis, but are largely accruing to the wealthy, and the problem only worsens. As such, the growing social anxiety and trend towards populism, be it conservative or liberal leaning, will not likely dissipate if the aforementioned economic trends continue." Begin by rethinking what the author says, and look at what happened post 2002 when Greenspan inflated the US housing bubble. Then note that graph of ten year GDP growth rate per capita, and then note that today the figures are almost certainly lower, and note that the graph is a crude approximation for productivity. Except that productivity needs to be measured as productivity per employee not per capita. Thus as unemployment falls, employment numbers increase, and productivity falls if GDP stays constant, so the graphed figures should be a bit optimistic. As stated in my earlier post, as this trend continues, the US economy moves into instability. There's a lot of noise in these figures, so deciding when things like a phase change has happened can only be precisely defined in hindsight. Maybe Armstrong's 2015.75 applies here, maybe not, the exact date is unimportant. There are no precedents for this, and I sincerely hope that I have completely misread the way things seem to be moving. Japan and some parts of Europe are ahead of the USA. Emergent nations with growing populations still have well-behaved economies. Think of all this as an enormous hall with rows and rows of dominoes all falling into place. The emergent nations' dominoes haven't started falling - yet. So, when you read "It ain't working", or similar thoughts, know that it also ain't fixable. But beware - economists are like medieval doctors, if one bunch of leeches hasn't worked, moar leeches will be applied. Is that any clearer? Maybe re-reading my last 3-4 posts will help? |

|

|

|

"Be not afraid of greatness. Some are born great, some achieve greatness, and some have greatness thrust upon them" - Shakespeare A day or two back, I'm told that we are now in a "post-heroic Age". This in the context that we are more likely to die in a household accident, such as falling off a chair, than in a terrorist attack. Add to this threats such as organised crime, drug trafficking, sex slavery, paedophilia, as headlined by the main stream media, and one would assume that the mass of the population is traumatised into fear of its own shadow. Ever wondered why they carry out polls to find out what scares you most? It's time to raise your eyes from this dark path and stare into the abyss nearby. Does that frighten you? Those of you still with me are probably asking. which abyss? there are so many? This one: "Stability" ... OK, dive in. For most of recorded history, 0 < beta + alpha. The population increased, and they found better ways to make stuff. The economy grew. The times when that didn't happen were dark times: the fall of the Roman Empire; the Black Death, ... you get the picture. Hence the willingness of politicians to talk about "growth" and "stability". Their audience translated this as more jobs, and more money, and that's what they voted for: Infinite Growth. But, Central Banks cannot create babies, nor even an increase in the economically active population. They might have contributed to an increase in innovation and productivity by ensuring that the most inefficient abusers of capital got pushed into creative destruction, but signally failed to do that. They cannot directly improve productivity or innovation. Which begs the question: Absent some magical event, what are the chances of both productivity and population growth turning down in the none-too-distant future? Quite high, perhaps, see here: http://sustainable.unimelb.edu.au/sites/default/files/docs/MSSI-ResearchPaper-4_Turner_2014.pdfThe paper follows up work carried out 1972-1974 "Limits to Growth", finds that the "Business as Usual" scenario is followed reasonably closely up to the date of publication (2014) and expects a decline in world industrial production to begin soon. And if growth continues, the collapse will be steeper and deeper. I'm inclined to believe that the outcome will not be as dire as some forecast. However, the point is made that we cannot expect 0 < beta + alpha to prevail much longer. What happens as we transit this trajectory? The world's economies move into instability, with unpredictable interactions. If the central banks were well prepared with low debt and plenty of munitions, they might be of some help. Frankly, they look like a liability. I'm thinking that this is hard to take in, that economics as we know it, free market capitalism, could just stop working. Maybe one word will explain : RATIONING. Got it? Everything falling into place? Good. Any Questions? Confirmations? I do expect one or more financial "events" before we get to that point. Whether we get a repeat of 2008, maybe better, maybe worse, remains to be seen. The last event saw a transfer of wealth to the one percent. Next time there will be many more people with little to lose. "Be not afraid of greatness", as this New Age of Heroes gets thrust upon our newest generation. The New Heroic Age. |

|

|

|

Milosevic finally exonerated. https://consortiumnews.com/2016/08/24/the-bogus-humanitarian-war-on-serbia/"It was blatantly ideological; at a notorious "peace conference" in Rambouillet in France, Milosevic was confronted by Madeleine Albright, the U.S. Secretary of State, who was to achieve infamy with her remark that the deaths of half a million Iraqi children were "worth it." Albright delivered an "offer" to Milosevic that no national leader could accept. Unless he agreed to the foreign military occupation of his country, with the occupying forces "outside the legal process," and to the imposition of a neo-liberal "free market," Serbia would be bombed. This was contained in an "Appendix B," which the media failed to read or suppressed. The aim was to crush Europe's last independent "socialist" state." "The final count of the dead in Kosovo was 2,788. This included combatants on both sides and Serbs and Roma murdered by the pro-NATO Kosovo Liberation Front. There was no genocide. The NATO attack was both a fraud and a war crime." "At the height of the bombing, the BBC's Kirsty Wark interviewed General Wesley Clark, the NATO commander. The Serbian city of Nis had just been sprayed with American cluster bombs, killing women, old people and children in an open market and a hospital. Wark asked not a single question about this, or about any other civilian deaths." "Milosevic died of a heart attack in 2006, alone in his cell in The Hague, during what amounted to a bogus trial by an American-invented "international tribunal." Denied heart surgery that might have saved his life, his condition worsened and was monitored and kept secret by U.S. officials, as WikiLeaks has since revealed." "The exoneration of a man accused of the worst of crimes, genocide, made no headlines. Neither the BBC nor CNN covered it. The Guardian allowed a brief commentary. Such a rare official admission was buried or suppressed, understandably. It would explain too much about how the rulers of the world rule." Just to seek a second opinion: http://www-personal.umich.edu/~lormand/agenda/9905/16.pdf"The Rambouillet Accord : A Declaration of War Disguised as a Peace Agreement" "A 28,000 strong NATO occupation army, known as KFOR, would be authorised to "use necessary force to ensure compliance with the Accords". "Kosovo has vast mineral resources, including he richest mines for lead, molybendum, mercury and other metals, in all of Europe." With this kind of ruthlessness, when they are hunting for cash under your sofa, or down the back of your cushions, even the cash in your child's piggy-bank will be a target. |

|

|

|

I'll summarize some of the points of these recent posts, because mainstream and most alt-media reporting seems to skip over important background details. Bucket shops were banned in 1929 because they were fraudsters. It was too easy to suck clients in on a momentum trade, and at an appropriate moment, to short the stock, causing a crash and wiping out clients trading on margin. The Savings and Loan Crisis (1986-1995) sent many bankers to jail. There were two other outcomes: the US government seized toxic loans, and as a consequence of attempting to sell these at a profit, forced unsafe practices onto the financial sector, and forced the Ratings Agencies to underestimate risk. the financial sector moved to protect itself from prosecution, seeking "deregulation" and "light touch regulation". Besides the removal of Glass-Stegall, the prohibition on "bucket shops" was removed. Fraud was now legal (again!). While the deregulation issue was broadly internationally understood, the repricing of risk and its effects was hidden. Financial instruments rated 'AAA' are expected to default once in 10,000 years. That number suggests that it is pointless to insure against default because your counterparty is more likely to fail than the bond. Initially, there was no market for that insurance (CDO's) because the risk was correctly priced. That changed, in part because of US government pressure, beginning with sub-prime.[1] In 2004 the FBI was warning that mortgage fraud in America was endemic. In 2005, Washington Mutual was reducing its mortgage lending, and in doing so, its profits suffered, weakening the bank. "More backers piled in with time, and by May 2005, Mr. Burry closed the first deal on subprime credit default swaps with Deutsche Bank." http://dealbook.nytimes.com/2010/03/01/michael-burry-the-man-who-shorted-subprime/In 2006 John Paulson took an artisan industry and industrialised it. Goldman Sachs, satisfied itself with its cut of the trade between the buyers and the sellers of CDO's. The lack of risk of going to jail, and the mispricing of risk mandated by US government pressure and practice meant that the more toxic the debt, the greater the likely profits all down the food chain. http://www.nakedcapitalism.com/2015/12/debunking-the-big-short-how-michael-lewis-turned-the-real-villains-of-the-crisis-into-heros.html"So it wasntt just that these speculators were harmful, and Lewis gave them a free pass. He failed to clue in his readers that the actions of his chosen heroes drove the demand for the worst sort of mortgages and turned what would otherwise have been a "contained" problem into a systemic crisis." "Both market participant estimates and repeated, conservative analyses indicate that Magnetar's CDO program drove the demand for between 35% and 60% of toxic subprime bond demand." "For the most part, the dealers themselves. Without going into mind-numbing detail, the apparent risklessness of an AAA instrument hedged by an AAA counterparty (in this case, a monoline) substantially reduced the capital a dealer needed to support a position. As a result, holding AAA CDOs hedged by AAA guarantors was treated, on a profit and loss basis on the relevant dealing desks, as vastly more attractive than finding investors to take the other side of the trade. In other words, this was massive gaming of the banks' own bonus systems." Think of it like this: If the government mandated fitting faulty brakes to cars, and then repealed all the laws relating to speeding and traffic violations, would you be surprised when a few accidents occur in good weather? followed by massive pileups on motorways when winter sets in? (It's not just the US Government BTW, they had help). [1] The Ratings Agencies agreed to change their models in 1997. Within ten years, problems began to appear: http://www.bankofengland.co.uk/publications/speeches/2009/speech374.pdfThe sort of problem that, according to statistics, as Haldane comments "To provide some context, assuming a normal distribution, a 7.26-sigma daily loss would be expected to occur once every 13.7 billion or so years. That is roughly the estimated age of the Universe." In good times failure rates can be fitted to a normal, gaussian distribution. That model would seem to be optimistic by a factor of four when the hard times reappear - the "fat tail" or power law distribution. |

|

|

|

Just a thought on the Economic Confidence model. When comedy gets to the mainstream, how long before it's all over? Bird and Fortune - the Subprime Crisis - The South Bank Show - The last Laugh - 14 October 2007 http://www.youtube.com/watch?v=mzJmTCYmo9g |

|

|

|

I hate lies. Lies get good people killed. That's lies, dammed lies and government statistics. So, when some government statistics "got revised", something just didn't smell right. I haven't, yet, worked out what is going on, but along the way I came across this: http://www.marketskeptics.com/2011/04/government-financial-innovation-caused-2008-financial-crisis.html"Below are two videos showing how the federal government (not wall street) caused 2008 Financial Crisis." https://www.youtube.com/watch?v=cNXyBIPAJqQ"1) Bundled toxic (subprime) loans into securities 2) Used financial alchemy to make risk "disappear" 3) Designed complex financial structures to hide the fraud 4) Developed insanely optimistic evaluation models to inflate ratings on toxic securities 5) Marketing these toxic securities to an unsuspecting public" https://www.youtube.com/watch?v=i4PE1gZn7s4"1) Created the entire infrastructure necessary for the subprime market to function 2) Decimated state authority to regulate the financial sector 3) Shielded subprime lenders from prosecution 4) Encouraged banks to buy toxic CDOs and to get rid of safer assets" I'll compress this into a few lines. Bucket shops began in the late 1800's, expanded in the 1920's and were outright banned in the USA in 1929. "In other words, they were fraudsters." - jmalmberg March 5, 2009 Then, after the USA's Savings and Loans crisis (1986-1995), parts of the US government found toxic debt on their books - similar to the subprime stuff of 2008 that had 40% delinquency rates, and to the 30% delinquency rates of the 1930's. When you have a load of fish sitting in the sun, and nowhere to put them, what do you do? In the case of this debt, the government cooked the books, then twisted the arms of the Ratings Agencies to change their models, and, as if by magic, toxic debt took on the appearance of investment grade government paper. Cue scene from "The Wolf of Wall Street", and a modern day bucket shop was born. Contrary to the current "What Everybody Knows" the Government had to twist Wall Street's arms pretty hard to get them to do their bidding. Even the US Justice Department began to throw up when they found out about this. In 2000, as part of the race to the bottom, this: "This act shall supersede and preempt the application of any state or local law that prohibits gaming or the operation of bucket shops" http://www.washingtonpost.com/wp-dyn/content/article/2008/02/13/AR2008021302783.html"Predatory lending was widely understood to present a looming national crisis. This threat was so clear that as New York attorney general, I joined with colleagues in the other 49 states in attempting to fill the void left by the federal government. Individually, and together, state attorneys general of both parties brought litigation or entered into settlements with many subprime lenders that were engaged in predatory lending practices. Several state legislatures, including New York's, enacted laws aimed at curbing such practices. What did the Bush administration do in response? Did it reverse course and decide to take action to halt this burgeoning scourge? As Americans are now painfully aware, with hundreds of thousands of homeowners facing foreclosure and our markets reeling, the answer is a resounding no." "... it used the power of the federal government in an unprecedented assault on state legislatures, as well as on state attorneys general and anyone else on the side of consumers." The above narrative fits the description of "Control Fraud" to a "T". That's maybe not the best move when your economy depends on a fiat based currency. Eliot Spitzer Governor of New York resigned on March 17 2008 amid threats of impeachment. Just. Another. Coincidence. And my original query? It's still in play. And a couple of other things: After you read up on the above, you may want to compare with this: http://ftalphaville.ft.com/files/2013/01/Perfect-Storm-LR.pdf"the real causes of the economic crash"  Also, an earlier post mentioned that the FED was a "monopoly purchaser of lemons". Sounds like the hole RTC found itself in all those years ago. |

|

|

|

I'm struggling to keep up with the flow of news. This is some weeks old, it's on the IMF and the Greek economy - some background - I don't have transcripts for some of this, so feel free to jump in: Around 2009-2010 everyone knew that Greece was going to default on its debts. Then, it got a bailout. And another, and another... In the midst of all this, Yanis Varoufakis became the Greek Finance Minister, and began to put together an economic plan. We were spared the details of his proposals, as he quickly found that the Troika, - the ECB, IMF and European Commission, none of whom were elected to any position of power, (and in effect the council of Finance Ministers) - were diametrically opposed to his proposals. The Troika wanted austerity, while at the same time imposing conditions that almost certainly ensured that the objective would not be met, despite, or perhaps because of, the likely collateral damage to the Greek economy and the need for further bailouts. Mr Varoufakis pressed the dozen or so key EU Finance Ministers and found that, in private, the Ministers were quite knowledgeable, and acknowledged the strength of his arguments. Singly, in private, they assured him of their support for his case, but as soon as these Ministers appeared in public, their understanding disappeared, and they were back onto the Troika's message. More curiously, Mr Varoufakis had appealed for help in tacking corruption, a widely publicised barrier to improving the Greek economy, and pursuing tax payments, essential for achieving the Troika's stated objectives. No help was forthcoming, despite dubious financial transactions with other EU member state's banks. Thus Greece could use only its own resources to fix its problems, despite a clear implication that other nations were benefiting from misdeeds. I'll briefly mention that my recent earlier post highlighted the relationship between government deficit spending and the profits of private companies. That logic would suggest that a sudden drive for government budget surplus would result in private, and public, companies running at a loss, and possibly into bankruptcy. The Troika's policies made the Greek situation worse. All the above suggests that, at best, the Troika's decisions were driven by politics rather than economics. Other interpretation placed on the Torika's motives could be much more concerning for the future of the Eurozone. Recently, support for Greece and for Mr Varoufakis, now the exFinance Minister, has appeared from an unexpected source - the IMF. "What the IEO report makes very clear is that the IMF should never have agreed, as part of the Troika, to assist the EU in forcing austerity upon Greece without insisting on significant debt relief, in the shape of a haircut, or (a) debt writedown(s).... The IMF's long established policy is that both MUST happen together." "And Europe's grip on the IMF is exactly what the report is about, in that it accuses Lagarde et al of bowing to EU pressure, to the extent that it abandons its own guiding 'laws'. It acted like it was the European Monetary Fund, not the international one." "That would seem to leave the IMF just one option: to apologize profoundly to Greece, to demand from the EU that all unjust measures be reversed and annulled, and to set up a very large fund (how about $1 trillion) specifically to support the Greek people, including retribution of lost funds, repair of the health care system, reinstatement of a pension system that can actually keep people alive and so on and so forth." http://www.zerohedge.com/news/2016-08-02/end-imf-credibility-or-why-christine-lagarde-should-be-fired-wont-behttps://www.theautomaticearth.com/2016/08/why-should-the-imf-care-about-its-credibility/http://www.ieo-imf.org/ieo/pages/CompletedEvaluation267.aspxSo, what to take away from all this? That the IMF, the ECB, and the European Commission are subservient to an unknown unelected body seemingly unconcerned by inter-national corruption to the extent of hundreds of billions of Euros? If it were not for prior art in the form of Operation Gladio, such a conspiracy theory would sound ridiculous. If, after researching Operation Gladio, you can afford a further three hours, see 'After Dark British Intelligence' - though it is off topic for this thread. http://www.youtube.com/watch?v=caUG4L-3S30I'm mentioning this only as background material on the relationship between an elected representative government and the notional Deep State. |

|

|

|

An inhabitant of the Bank for International Settlements claims bankers are "Magic People" Kuroda-San insists that if the Japanese people would only believe : "I trust that many of you are familiar with the story of Peter Pan, in which it says, 'the moment you doubt whether you can fly, you cease forever to be able to do it,'" all would be well with the Japanese economy. What next? "attempts to kill goats by staring at them."? (and more) "The Men Who Stare at Goats (2004) is a book by Jon Ronson concerning the U.S. Army's exploration of New Age concepts and the potential military applications of the paranormal." https://en.wikipedia.org/wiki/The_Men_Who_Stare_at_GoatsMaybe even "Helicopter Money"? - Seriously? - How might this work in practice? Soooo, you have thought this through, and maybe created "Streetwalkers Inc", (for the tax advantage.) While walking down main street, your corporation finds a newly issued $1 bill. What do you do? You enter it into your P&L account: Profit from walking down street : $1 Wonderful. Profits, unfortunately, do not just appear out of thin air. How to even know that this is a profit? Let's simplify Levy's total profits equation: TNP = TVI + t4b + t5b + t6b + cCr + aL - cCrl -cs + TpCNP + BT + BI - Tdp - ex -dep + ETC -vOt7 + vOt8 Yuck. But all we need from the equation is this : TNP = TVI TNP = Total Net Profits (all corporations) TVI = change in the value of money over the time in examination. Since the quantity of goods that can be bought is unchanged, the profit is created by an increase - $1 - in the quantity of money. And, since the quantity of goods is unchanged, there must be a loss somewhere. In this case, the bank that printed and issued the money - it now has a loss to account for. Thus, "Helicopter Money", in current parlance, will be paid out of the pockets of the owners of the banks, most probably the owners of the Central Bank - TPTB. About as likely as (1+1 ne 2) IMHO.[1] So, if governments (ie, you, dear taxpayer) are not going to fund "Helicopter Money" what is really going on? (Taxpayer funding makes as much sense as some of the projects referred to earlier) - A non-mathematical, non-economic, conspiracy-theory explanation should have the fewest assumptions. "Occam's Razor : Among competing hypotheses, the one with the fewest assumptions should be selected." The TPTB are involved, soooo, maybe this? The World is being conditioned to drop its trousers and grab its ankles anytime the phrase "Helicopter Money" is broadcast. Oh! One other thing: Don't forget to say "Thank You Ben Bernanke!" [2][3] If, by now, you are curious as the the competence and motivation of these monetary gods, the concluding remarks of a report on the Lehman debacle may crystallize those doubts: "Their explanations for their actions rest on flawed economic and legal reasoning and dubious factual claims." http://www.econ2.jhu.edu/People/Ball/Lehman.pdf[1] for example see "Exploring Complex Dynamic Systems" Cheng, Zhang J System Simulation 2002 14(11): 1147-1149 [2] Feel free to substitute your choice of Central Banker. [3] Your guess at what happens next? |

|

|

|

"The tragedy of investment is that it causes crisis because it is useful. Doubtless many people will consider this paradoxical. But it is not the theory which is paradoxical, but its subject - the capitalist economy." Kalecki As an example, see US net government lending, $Bn starting in 2007: -354.9 -781.8 -1476.7 -1509.5 -1400.1 -1214.8 -698.3 -681.4 -602.3 So, from 2008 to 2012, some $2.7Tn of excess deficit went into the US economy. "One of the more enlightening things you learn from a sound understanding of macro is the Kalecki profits equation which shows that corporate profits are the result of the following equation:" Profits = Investment - Household Savings - Government Savings - Foreign Savings + Dividends http://www.pragcap.com/why-hasnt-the-budget-deficit-decline-hurt-corporate-profits-more/That suggests that the $5.6Tn that the US government borrowed between 2008-2012, if all other things were unchanged, became profit somewhere in the economy. And the Stock Market soared. Since then, from 2013-2016, the Stock market has some $2Tn less in government funded profits, and is presumably buoyed up only because the Federal Reserve Bank is cornering the market for Lemons. http://www.nytimes.com/2010/11/24/business/economy/24econ.html"American businesses earned profits at an annual rate of $1.659 trillion in the third quarter" http://www.nytimes.com/2010/11/24/business/economy/24econ.html"Corporate profits have been doing extremely well for a while. Since their cyclical low in the fourth quarter of 2008, profits have grown for seven consecutive quarters, at some of the fastest rates in history. As a share of gross domestic product, corporate profits also have been increasing, and they now represent 11.2 percent of total output. That is the highest share since the fourth quarter of 2006, when they accounted for 11.7 percent of output. This breakneck pace can be partly attributed to strong productivity growth - which means companies have been able to make more with less - as well as the fact that some of the profits of American companies come from abroad. Economic conditions in the United States may still be sluggish, but many emerging markets like India and China are expanding rapidly." "This breakneck pace can be partly attributed to people getting fired" - FIFY. Before moving on, note the borrowing requirement in 2007, $354.9Bn, the difference between spending and taxation, in broad terms, and contrast the values for later years. You may be curious as to how borrowing got reduced 2013 - 2015? Here are the tax revenues: 2660.8 2505.7 2230.1 2391.7 2516.7 2663 3141.3 3265.2 3434.9 (US$Bn) The change is accounted for neatly by an increase in taxation in one form or another, rather than any reduction in government spending. This seems to be a widespread paradox - "capitalist" economies whose profits are often entirely funded by governments. Those 2010 accounts are entirely coincidental :-) Any thoughts on "Helicopter Money" yet? We're getting to the endgame, and the equation above provides a hint of things that just aren't gonna happen. |

|

|

|

Just to point the discussion on fraud in the right direction ... http://edition.cnn.com/2004/LAW/09/17/mortgage.fraud/index.html?_s=PM:LAW"From Terry Frieden CNN Washington Bureau Friday, September 17, 2004 Posted: 2144 GMT (0544 HKT) Assistant FBI Director Chris Swecker said the booming mortgage market, fueled by low interest rates and soaring home values, has attracted unscrupulous professionals and criminal groups whose fraudulent activities could cause multibillion-dollar losses to financial institutions. "It has the potential to be an epidemic," said Swecker, who heads the Criminal Division at FBI headquarters in Washington. "We think we can prevent a problem that could have as much impact as the S&L crisis," he said." https://ourfuture.org/20150911/now-the-justice-department-admits-they-got-it-wrong"By issuing its new memorandum Thursday, the Justice Department is tacitly admitting that its experiment in refusing to prosecute the senior bankers that led the fraud epidemics that caused our economic crisis failed. The result was the death of accountability, of justice, and of deterrence. The result was a wave of recidivism in which elite bankers continued to defraud the public after promising to cease their crimes." I'm shocked, shocked, to find that gambling is going on in these places. But you knew all this already (I hope) and could have found these references in a few seconds with a simple search. I'm coming to the view that the biggest deception practiced by the banks is that we need the banks, the bankers, and the financial sector. There's a simple equation that suggests that TPTB will never allow helicopter money. I'll post something later, but If you have any thoughts on that feel free to post.here. |

|

|

|

|

Maybe the time has come for ZIRP (Zero Interest Rate Policy). No, really, ZIRP!

As in nobody gets to charge interest. During the Middle Ages, that was they way

things worked. In those days, money was for trade, paying armies, and not much else.

Debasing the currency was a Capital offence, and without interest, banking and

moneylending were niche industries.

So, suppose the artificial divide between those who can and those who can't borrow

at zero interest rates disappears. Well, the first impact would be to credit card

companies and payday lenders. Their business model is trashed. Do dry your eyes

dear reader. There's more.

Banks would have a problem. Eighty percent of their business is mortgage lending,

that would be just before they package the toxic stuff with a wrapper of AA and

flog it to some "sophisticated" pension fund desperate for yield. Did I mention

Ratings Agencies might actually have to work for a living? House prices would fall,

and banks would be out of the mortgage business because they just could not afford

the risks they are currently financing. Banks would be one fifth their present

size, perhaps less, because business would have to replace large chunks of their

debts with equity. If, as a private lender, you get no return on a loan to a

business the loan will not be made, so business will be forced towards retained

earnings and equity.

All this may seem strange when compared with the world today. Companies are using

cheap debt to buy back their shares to boost P/E ratios to push up share prices

to increase the value of management's stock options irrespective of the long

term implications for shareholders. Similarly for other asset price inflation

such as real estate. That, dear reader, is the point. Central Banks are buying

up assets and putting it on your tab. If not onto your tax bill, certainly

out of your pension fund and savings account. They are moving from AAA rated

paper into toxic waste and into monkey dung. Best of all, if ZIRP wasn't just

for the rich and well-connected, there would be no need for a Central Bank.

OK, maybe just a tiny unrecognisable barbaric relic of a Central Bank. Maybe.

One final point: Interest on loans is, in most cases, a business expense. The

business does not pay tax on the interest. Unlike Dividends. So if you invest

in equity you get taxed twice, first by corporation tax, then by income tax.

And guess what, if you have an offshore account, a loan is the way to go.

BTW, I suspect US price inflation will be ~5% by mid 2017

I'm thinking I might go long popcorn, deckchairs, and bicycle clips.

|

|

|

|

Paradox is awsome. The downside is that you to have to live with the knowledge that 1+1 doesn't always equal 2, luckily, that probability is infinitely small. Other, real-life paradox does matter, and finance and law are full of it. Think about Central Banks this way: Would you like to have an imaginary friend who gives you money? The USA did that in 1913, and the Brits did it waaay earlier. Of course, logically, most banking is fraud, so the governments have to create the legal fiction that Central Bank actions are fair and just, and also that if ayone else attempts this they go straight to Jail. So if you and I decide that we have an imaginary friend who gives us money, we not only go to Jail, we probably get assessed for tax, KYC, AML, structuring, as well. Got that? Cool. Pass enough laws, and eventually you get two mutually exclusive things that must be true. This is meat and drink to the legal profession, and since the Central Banking and financial systems are founded on legal fictions, it's sorta a permanent open season - don't try this at home, to mix metaphors. Which brings me to this: http://www.zerohedge.com/news/2016-07-13/spoofing-trader-who-outsmarted-citadel-and-hfts-gets-3-year-jail-sentence"And the biggest irony: Steven Peikin, one of Coscia's lawyers, argued that high-frequency traders routinely canceled orders. He told the jury that Coscia's trading strategy was unique but not illegal. Wrong: it is illegal, but he is absolutely right that everyone does it, especially the HFTs. But doesn't matter - next year Coscia will be back in court to hear just how many years he will spend in prison." Fast forward to today when Coscia's story gets its conclusion. As Bloomberg reports, Michael Coscia, the first person convicted of spoofing after it was made a crime under the Dodd-Frank Act, was sentenced to three years in prison by a federal judge in Chicago, less than half the time sought by prosecutors." "His real crime? Taking on the HFTs, and Citadel, and winning. Now he gets to spend 3 years in prison thinking about it. And let that be a lesson to anyone else out there who dares to do the same." There are many facets to this story, one is this: TPTB realised that this was just another version of the "imaginary friend" and that if it was allowed to continue, the entire Banking scam would fall apart. So, everybody knows what's going on, they even complain to the regulators - but when they do as others do, and are profitable, they get arrested. You might conclude that trading is only allowed after the protection tax is paid, but I couldn't possibly comment on that. I'll admit I'm surprised that a jury would convict. After all, if they don't understand what's going on, they have to acquit, don't they? And if they thought bitcoin was a threat, we would all be in Jail. |

|

|

|

'Let the jury consider their verdict,' the King said, for about the twentieth time that day. 'No, no!' said the Queen. 'Sentence first - verdict afterwards.' From "Alice in Wonderland" 'Brexit' is seen as the cause of so much these days that it may be timely to point out that: a) it hasn't yet happened; and b) not much may actually change on the economics once things get underway. So, what are we witness to? A ripple on the surface of things still to come? Payback for 2008 when banks should have been allowed to exit via bankruptcy and clear the bad debts built up from years of fraud and greed? What was mortgaged into the future may now become due, and, in my opinion, the UK sensed that if it was to manage its share in any collapse, it was best done outside the control of the European Commission. And financial troubles, being man-made, are manageable, however painful they might be, but you have to have full freedom, at minimum, to act via your Central Bank. Which in a way, brings me to the curious decision of the Bank of England to suggest a cut in interest rates, some say from 0.5% to 0.25%. But before getting down to the price of Bitcoin, lets think about the wider implications. The announcement seemed to be a response to the market's clamour that something, anything, must be done, which in itself was probably a self-fulfilling result of Project Fear, and over-hyped falls in the value of Sterling. The BoE's mandate is for the operation of UK banks, and a cut in rates would harm the profitability of that sector, hence the delay in taking action. So who might profit from a cut in rates, apart fro the usual suspects who profit from turmoil in the markets? In the long run, UK manufacturing, but not enough to make a difference now. Property, including housing and commercial real estate (CRE)? Since Financialisation the banks have been bunged to the gills with this stuff. Well, thanks to government policy, and the worldwide race toward NIRP, the rentier sector has reached altitudes where oxygen starvation is a distinct possibility - witness the panic in the UK property fund sector, with redemptions gated, and prices cutting back several year's gains. http://www.zerohedge.com/news/2016-07-06/dramatic-twist-uk-property-fund-cuts-value-its-assets-17 Hmmmm ... will it work? If debt increases, certainly yes. More debt boosts GDP immediately, but has to be paid for later. But where will the money come from? Usually interest rates are raised to bring money into the UK, and it is a signal toward to instabilities in the present arrangements that it can be suggested that cutting rates might boost sterling. Where might money go if it wants out of the UK? Not Europe, probably not Japan, though anything seems possible these days, Switzerland's negative rates? Hmmmm ... The broader picture of worldwide declining interest rates has Central Banks acting like beaters on a grouse moor, driving investors toward US corporate debt to the benefit of global corporations such as Amazon. That has implications best left for another day, and perhaps to another forum. http://www.zerohedge.com/news/2016-07-07/reason-relentless-scramble-us-corporate-debt-one-chartAnd the implications for Bitcoin? That may depend on where you live, and your view of your currency. For the UK, it remains to be seen whether Mr Carney follows through with a cut to interest rates. He seems to have played better than his counterparts thus far, though as they say, past performance is no indication of future returns. Given the turmoil of UK's politics, bitcoin may seem attractive right now. |

|

|

|

|

{kind=link}