|

Title: Down to zero it goes! Post by: bitcoin0918 on June 25, 2011, 04:00:30 PM Well, there it goes, down to zero. It had a good run while it lasted, but this was the obvious end result.

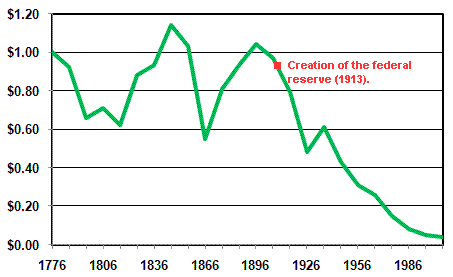

Here's the chart of its lifetime: http://static.seekingalpha.com/uploads/2009/3/9/saupload_dollar_value_chart.png Goodbye USD, hello BTC! Why, what did you think I was talking about? ;D Title: Re: Down to zero it goes! Post by: Gabi on June 25, 2011, 04:04:32 PM Lol nice graph

Title: Re: Down to zero it goes! Post by: onesalt on June 25, 2011, 04:42:38 PM Huh wierd because most banks offer intesterest at rates better than inflation and I can still use my money to buy things?

Title: Re: Down to zero it goes! Post by: hugolp on June 25, 2011, 04:48:57 PM Huh wierd because most banks offer intesterest at rates better than inflation and I can still use my money to buy things? Higher than the CPI, not the real price inflation. Title: Re: Down to zero it goes! Post by: bitcoin0918 on June 25, 2011, 04:58:54 PM Huh wierd because most banks offer intesterest at rates better than inflation and I can still use my money to buy things? Wow, bank rates higher than 10% (http://www.shadowstats.com/alternate_data/inflation-charts)?! Where do you live?Title: Re: Down to zero it goes! Post by: Justsomeforumuser on June 25, 2011, 04:59:30 PM I can get 4.2% interest for a 3 year guaranteed treasury/whatever it's called in english deposit.

Yay EUR land. Also what bollocks in the OP. The USDX is back over 75 and it's going to move higher again, just like Gold is going to lose that 1500$ mark. Nobody anywhere benefits from the USD "going to zero". Also lal @ shadowstats. I should just start selling tinfoil hats for BTC, would go like hotcakes. Next to the tulips and bridges, that is. Title: Re: Down to zero it goes! Post by: bitcoin0918 on June 25, 2011, 05:04:06 PM Also lal @ shadowstats. I should just start selling tinfoil hats How is it a conspiracy theory? It's a fact that CPI measurement techniques have changed multiple times over the last few decades, with the observed result of reporting a lower amount of inflation as compared to previous measurement techniques. Whether or not there were political motives behind these CPI changes is irrelevant when one's only goal is to accurately compare present inflation to past inflation.I'm not interested in conspiracies, only in preserving my wealth. And to do so requires that I am able to objectively measure long-term changes in the value of the dollar. If CPI measurement techniques change over time, they necessarily must be re-adjusted to correct for these changes. This is not an argument, not a conspiracy theory, but a fact. Title: Re: Down to zero it goes! Post by: Justsomeforumuser on June 25, 2011, 05:08:54 PM Oh I agree that a ton of stats are misreported or measured (NFP birth/death adjustment just as an example).

I just would also say that SS is a classic "zomgwtfbbq" site in tone and usually used by people who talk about "the amero" and other such sillyness. It's been a consistent phenomenon. And ever since seeing my first "zomg USD going to 0" post in 2006 on a forex related forum this has continuously been a recurring theme, month in, month out. Stuff like inflation talk, gold hyping and "one world currency" is usually not far behind. Sometimes the Rothschilds and masons get a go, too! Title: Re: Down to zero it goes! Post by: bitcoin0918 on June 25, 2011, 05:10:23 PM I just would also say that SS is a classic "zomgwtfbbq" site in tone and usually used by people who talk about "the amero" and other such sillyness. Yes, it has been. Another consistent phenomenon has been the rejection of alternative CPI measurements via guilt-by-association (http://en.wikipedia.org/wiki/Association_fallacy#Guilt_by_association) fallacies such as the one you present above.It's been a consistent phenomenon. Title: Re: Down to zero it goes! Post by: ribuck on June 25, 2011, 05:25:48 PM I can get 4.2% interest for a 3 year guaranteed treasury/whatever it's called in english deposit. Inflation in the UK is 4.2% if measured by the CPI, 5.1% if measured by the more realistic RPI, and a bit more still if measured by how much the cost of living is increasing for the average person.So an interest rate of 4.2% is, at best, not making any money. At worst, it's losing a few percent of real value each year. And that's before taking into account that most people will need to pay tax on any interest that they earn. And before taking into account that inflation will probably be a lot higher before this 3-year investment matures. When I was younger, you could generally count on making 3% from a savings account after tax and after inflation. That hasn't been possible for a few decades now. Title: Re: Down to zero it goes! Post by: kokojie on June 25, 2011, 05:58:29 PM nice graph

Title: Re: Down to zero it goes! Post by: JTaBitCoinKing on June 25, 2011, 06:46:10 PM I got some dehydrated food, some silver, and my first Bitcoin miner arrives on Monday. I'm ready for the Apocalypse. Let the p2p revolution begin! Send these greedy bankers packing!

REMEMBER THE ALAMO!!!!... Actually, I don't care about the Alamo. I'm in California! ;D Title: Re: Down to zero it goes! Post by: unk on June 26, 2011, 01:37:40 AM I can get 4.2% interest for a 3 year guaranteed treasury/whatever it's called in english deposit. Inflation in the UK is 4.2% if measured by the CPI, 5.1% if measured by the more realistic RPI, and a bit more still if measured by how much the cost of living is increasing for the average person.So an interest rate of 4.2% is, at best, not making any money. At worst, it's losing a few percent of real value each year. And that's before taking into account that most people will need to pay tax on any interest that they earn. And before taking into account that inflation will probably be a lot higher before this 3-year investment matures. When I was younger, you could generally count on making 3% from a savings account after tax and after inflation. That hasn't been possible for a few decades now. bitcoin doesn't change any of this. the inflation of fiat currencies, and its effects, are very poorly understood on these forums in general. the income from interest came from the participation of your savings accounts in the growth of the economy. the income from the hoped-for deflation of your bitcoins (based on bitcoin's future monetary policy, because of course bitcoins are right now substantially more inflationary than any fiat currencies, monetarily speaking, and they will remain so for some time) will come from exactly the same source. if the economy does not grow in real terms, there's no way that everyone can receive positive risk-free returns; there's nothing to do but shift the existing or dwindling wealth from person to person. i still bristle when i see people in these forums angry at the inflation of fiat currencies. the comparison to bitcoins is misleading. nobody received a dollar in 1913 and expected it to have the same purchasing power in 1999. and during the inflation that the original poster's chart shows, the united states was, with a handful of exceptions, both prospering and increasing its prosperity; the inflation of the money supply did not stop that. moreover, as i've tried to explain before, monetary policy does not force inflation's effects on people; anyone could purchase other assets (though not with infinite flexibility, given the outlawing of private holding of gold, which is a more serious regulatory intrusion than monetary inflation) with their cash if they wanted to avoid the effects of inflation. other regulations, including tax laws, have imposed limits on people's abilities to invest arbitrarily, but that is not the fault of monetary policy. the anger at the 'inflation' of 'fiat currencies' is, for these reasons, rather bizarre, and honestly the frequency with which it's repeated here increases the amateurish and fringe feel of the community. there are a lot of things to be angry at central banks for. that the dollar inflated throughout the 20th century is not one of them. Title: Re: Down to zero it goes! Post by: bitcoin0918 on June 26, 2011, 02:27:44 AM the income from interest came from the participation of your savings accounts in the growth of the economy. the income from the hoped-for deflation of your bitcoins (based on bitcoin's future monetary policy, because of course bitcoins are right now substantially more inflationary than any fiat currencies, monetarily speaking, and they will remain so for some time) will come from exactly the same source. Nobody but speculators are hoping to gain *income* from bitcoins. Bitcoins are not an investment, and are not supposed to pay a return.Quote if the economy does not grow in real terms, there's no way that everyone can receive positive risk-free returns; there's nothing to do but shift the existing or dwindling wealth from person to person. Economic growth requires capital, which comes from savings. It is not savings that depends on economic growth, but the other way around. So long as people save, there will be money for future economic growth. Only when monetary policy intervenes to discourage savings does the economy suffer.Quote nobody received a dollar in 1913 and expected it to have the same purchasing power in 1999. From where have you summoned such omniscience? Look up the concept of the "99-year loan" - which was much more common in the past, but is unheard of today.Quote during the inflation that the original poster's chart shows, the united states was, with a handful of exceptions, both prospering and increasing its prosperity Correlation is not causation. The US was prosperous despite its degrading purchasing power, and would have been even more prosperous had the currency been stable.Quote moreover, as i've tried to explain before, monetary policy does not force inflation's effects on people Given that the US dollar has a government-backed monopoly on legal tender, forcing people who want to trade with others to accept US dollars, I will vehemently disagree with this claim. You are basically saying, "if you don't like it - leave!" That is not an argument.Quote the anger at the 'inflation' of 'fiat currencies' is, for these reasons, rather bizarre, and honestly the frequency with which it's repeated here increases the amateurish and fringe feel of the community. Fortunately, feelings are no substitute for rationale. Your feelings will be disregarded.Title: Re: Down to zero it goes! Post by: unk on June 26, 2011, 02:37:04 AM the income from interest came from the participation of your savings accounts in the growth of the economy. the income from the hoped-for deflation of your bitcoins (based on bitcoin's future monetary policy, because of course bitcoins are right now substantially more inflationary than any fiat currencies, monetarily speaking, and they will remain so for some time) will come from exactly the same source. Nobody but speculators are hoping to gain *income* from bitcoins. Bitcoins are not an investment, and are not supposed to pay a return. If there were bitcoin banks that paid interest for bitcoin savings, then the situation would be identical to current savings banks.you misunderstand my point, or perhaps you haven't fully thought through the economic landscape. right now, bitcoins are used almost entirely as a speculative vehicle, but if they took on the form of an operational currency, there could indeed be 'income' through simple monetary deflation against the economy that bitcoin represented. Quote Economic growth requires capital, which comes from savings. It is not savings that depends on economic growth, but the other way around. So long as people save, there will be money for future economic growth. Only when monetary policy intervenes to discourage savings does the economy suffer. again, you misunderstand or are applying insufficient analysis. a statement like 'it is not savings that depends on economic growth, but the other way around' is not analytically coherent because we're not describing a mutually exclusive causal process. economic growth in a capitalistic system both requires and rewards investment; 'requires' does not eliminate or oppose 'rewards' in that sentence. Quote Quote nobody received a dollar in 1913 and expected it to have the same purchasing power in 1999. You have summoned this omniscience from where, exactly? Look up the concept of the "99-year loan" - which was much more common in the past, but is unheard of today.again, this is a misunderstanding. a long-term loan is not inconsistent with anything i've said. Quote Given that the US dollar has a government-backed monopoly on legal tender, forcing people who want to trade with others to trade in US dollars, I will vehemently disagree with this claim. You are basically saying, "if you don't like it - leave!" That is not an argument. i've shown at least two or three times, in other discussions, exactly why this is wrong. i said that in my last message, and you could have looked it up before responding in ignorance. the 'legal tender' laws do not force anyone to hold fiat currencies long-term and thus experience their long-term inflationary effects. the transaction costs of moving out of fiat currency are minimal in most contexts. moving back in occasionally incurs capital-gains taxes, but that is then a feature of the taxing laws, not the legal-tender laws, that may discourage particular types of investments; the taxing laws are not neutral as to the choice of investments, but that is not an indictment of monetary policy. and in any event, it is easy to avoid capital-gains taxes, in these contexts, in nations like the united states and the united kingdom using a variety of practical mechanisms. if you think that you are forced to experience the inflation of fiat currencies, you're simply mistaken. i have significant holdings, and about 5% of them are in fiat currencies and thus subject to any sort of inflation. few people with significant wealth choose a portfolio more weighted toward cash in the long term, for obvious reasons. Quote Fortunately, feelings are no substitute for rationale. Your feelings will be disregarded. yet my scholarship is often cited, my businesses prosper, and my teaching is influential. your dismissive arrogance in response to me is startling given that you don't appear to have understood anything i've said. Title: Re: Down to zero it goes! Post by: tavi on June 26, 2011, 02:47:02 AM I got some dehydrated food, some silver, and my first Bitcoin miner arrives on Monday. I'm ready for the Apocalypse. Let the p2p revolution begin! Send these greedy bankers packing! Actually, no.REMEMBER THE ALAMO!!!!... Actually, I don't care about the Alamo. I'm in California! ;D Remember A.Lamo (http://en.wikipedia.org/wiki/Adrian_Lamo#WikiLeaks_and_Bradley_Manning) >:( Title: Re: Down to zero it goes! Post by: Oldminer on June 26, 2011, 03:03:18 AM http://theeconomiccollapseblog.com/wp-content/uploads/2010/12/Ben-Bernanke-250x250.jpg What's wrong with that chart? It's a masterpiece! - Ben the Junkie Title: Re: Down to zero it goes! Post by: bitcoin0918 on June 26, 2011, 03:06:11 AM few people with significant wealth choose a portfolio more weighted toward cash in the long term, for obvious reasons. Exactly, and because these reasons discourage savings, and savings is a necessity for economic growth, the economy suffers. It may still prosper overall, but it will not prosper as much as it could have.No matter how you try to paint it, the loss of real purchasing power does not benefit anyone but those who use it to their advantage (which in this case are politicians who use deficit spending to fund short-term projects to gain votes, and then encourage an inflationary policy to pay off past debt with devalued currency) Quote yet my scholarship is often cited, my businesses prosper, and my teaching is influential. Your appeal to authority, on the other hand, is not influential.Title: Re: Down to zero it goes! Post by: CurbsideProphet on June 26, 2011, 03:06:42 AM Where are you getting rates better than inflation? I think inflation has been about 4% lately (at least that is what the government says), but banks around here are only offering like 2% if you are lucky. Where are you getting 4% inflation? TIPS just sold for a record low last week. If the market (read: not the gov't) was pricing for inflation, TIPS would not be at the yield they are. I'm curious where you're getting your information. Title: Re: Down to zero it goes! Post by: westkybitcoins on June 26, 2011, 03:08:03 AM i still bristle when i see people in these forums angry at the inflation of fiat currencies. the comparison to bitcoins is misleading. nobody received a dollar in 1913 and expected it to have the same purchasing power in 1999 To the contrary, I imagine plenty of the people who received silver dollars in 1913 expected those dollars to have the same purchasing power... or even greater... by the end of their children's lifetimes. And, hey, they pretty much were right! It's those who held paper dollars that got screwed. :( Oh, but that's their own fault though, right? These largely rural, pre-WWI folks should have known not to trust the government, and to save and conduct business in precious metals only... that's what their government schools taught them to do, after all. (Not.) Quote there's a lot to be angry at central banks for. that the dollar inflated throughout the 20th century is not one of them. Yes, it absolutely is the fault of the central bank. Inflation is an increase in the money supply. The central bank is the primary entity which increases the money supply. Ergo, the central bank is responsible for inflation throughout the 20th century. Title: Re: Down to zero it goes! Post by: Anduril on June 26, 2011, 03:18:01 AM bitcoin doesn't change any of this. the inflation of fiat currencies, and its effects, are very poorly understood on these forums in general. the income from interest came from the participation of your savings accounts in the growth of the economy. the income from the hoped-for deflation of your bitcoins (based on bitcoin's future monetary policy, because of course bitcoins are right now substantially more inflationary than any fiat currencies, monetarily speaking, and they will remain so for some time) will come from exactly the same source. if the economy does not grow in real terms, there's no way that everyone can receive positive risk-free returns; there's nothing to do but shift the existing or dwindling wealth from person to person. i still bristle when i see people in these forums angry at the inflation of fiat currencies. the comparison to bitcoins is misleading. nobody received a dollar in 1913 and expected it to have the same purchasing power in 1999. and during the inflation that the original poster's chart shows, the united states was, with a handful of exceptions, both prospering and increasing its prosperity; the inflation of the money supply did not stop that. moreover, as i've tried to explain before, monetary policy does not force inflation's effects on people; anyone could purchase other assets (though not with infinite flexibility, given the outlawing of private holding of gold, which is a more serious regulatory intrusion than monetary inflation) with their cash if they wanted to avoid the effects of inflation. other regulations, including tax laws, have imposed limits on people's abilities to invest arbitrarily, but that is not the fault of monetary policy. the anger at the 'inflation' of 'fiat currencies' is, for these reasons, rather bizarre, and honestly the frequency with which it's repeated here increases the amateurish and fringe feel of the community. there are a lot of things to be angry at central banks for. that the dollar inflated throughout the 20th century is not one of them. Just wanted to congratulate you on a very sound analysis. It is good to see someone who understands monetary policy beyond Tea Party soundbites. Title: Re: Down to zero it goes! Post by: unk on June 26, 2011, 03:21:15 AM few people with significant wealth choose a portfolio more weighted toward cash in the long term, for obvious reasons. Exactly, and because these reasons discourage savings, and savings is a necessity for economic growth, the economy suffers.please try to explain the precise mechanism by which you think that happens. certainly taxes and transaction costs serve to slow various kinds of economic 'growth', though of course most people (perhaps not in this forum) think taxes have countervailing benefits. but you have not explained how you think monetary policy will 'discourage savings'; generally it does not, for the reasons i've already outlined. it simply makes one available 'savings' instrument less attractive, which eliminates nobody's choices. (other things, of course, might limit their choices.) if it helps, you might think of the dollar as a service provided by the united states government. you might not like the service, but nobody forces you to engage in it as a long-term holder subject to the sorts of inflationary pressures in your chart. you have to pay taxes in it if you owe income taxes, but that only helps you if it inflates and you need to convert to it on a certain date in the future. you have to accept it for payment of debts, though you can convert out of it immediately in that case. what's left are, again, various taxing issues that are not as significant, in practice, as people here think they are. note that i'm not relying on economic dogma here; i've explained the analysis i'm providing, both in this discussion and, in more detail, in others. i'm as critical of economic dogmas as anyone. i'm writing here just to try to correct an often-repeated misunderstanding in this forum. it's fairly unique to this forum and other fringe online communities; at least, i've never seen it elsewhere. my goal is actually to help people think more clearly about bitcoins, as i've been doing since i started posting. it is not in any way anti-bitcoin, in case that alleviates a concern that is possibly motivating your strident response to me. Quote No matter how you try to paint it, the loss of real purchasing power does not benefit anyone but those who use it to their advantage (which in this case are politicians who use deficit spending to fund short-term projects to gain votes, and then encourage an inflationary policy to pay off past debt with devalued currency) that's not quite true, but regardless, the point is that purchasing power is lost only by those who choose to continue to hold dollars long-term in the face of many alternatives. think of it this way: if you couldn't avoid deflation by holding commodities, securities, or other instruments instead, how could bitcoin help you avoid inflation? bitcoin doesn't add anything new if your goal is simply to avoid inflation; what it adds is, in principle, a convenient payments system, and it reduces the transaction costs (again, in theory) of moving funds into and out of that payments system. the rest of bitcoin is either (1) ill-founded marketing, though that's quite common in this forum or (2) speculation, which is as good or as bad as anyone ordinarily thinks speculation is. Quote Quote yet my scholarship is often cited, my businesses prosper, and my teaching is influential. Your appeal to authority, on the other hand, is not influential.you seem to have neglected the flow of the conversation here. you suggested my 'feelings' were irrelevant; i claimed they aren't. nothing else i've said depends on my 'authority', my stature, or indeed on anything else about me. westkybitcoins: you're missing my point, i'm afraid. i'm not saying that central banks aren't responsible for inflation. i'm saying that nobody is forced to experience that inflation long-term, contrary to the sentiments that i so commonly see in this forum. let me ask you: do you hold us dollars in your long-term investment accounts? if so, why? what's preventing you from avoiding them if you are so concerned about inflation? the answer is nothing, except again, in the marginal case, perhaps capital-gains taxes that you could likely avoid if you put your mind to it. Title: Re: Down to zero it goes! Post by: foggyb on June 26, 2011, 03:46:26 AM nobody received a dollar in 1913 and expected it to have the same purchasing power in 1999. The expectation of the day was CERTAINLY NOT that the dollars they were accepting in 1913 would be lose more than 90% of their value in less than 90 years. Title: Re: Down to zero it goes! Post by: bitcoin0918 on June 26, 2011, 03:47:57 AM few people with significant wealth choose a portfolio more weighted toward cash in the long term, for obvious reasons. Exactly, and because these reasons discourage savings, and savings is a necessity for economic growth, the economy suffers.please try to explain the precise mechanism by which you think that happens. Quote but you have not explained how you think monetary policy will 'discourage savings'; Besides what I have said above, I am curious how you conclude that the Fed's monetary policy of keeping interest rates artificially low, thus reducing the interest rate paid toward savings, does not discourage savings.Quote the point is that purchasing power is lost only by those who choose to continue to hold dollars long-term in the face of many alternatives I am forced to pay into social security - money which I will supposedly get back at retirement in a highly diluted state. Are you saying I have a choice not to give up that purchasing power?Quote nothing else i've said depends on my 'authority', my stature, or indeed on anything else about me. Then why the necessity to reference your credentials? What did you hope to gain by citing them?Title: Re: Down to zero it goes! Post by: westkybitcoins on June 26, 2011, 03:49:14 AM westkybitcoins: you're missing my point, i'm afraid. i'm not saying that central banks aren't responsible for inflation. i'm saying that nobody is forced to experience that inflation long-term, contrary to the sentiments that i so commonly see on that board. let me ask you: do you hold us dollars in your long-term investment accounts? if so, why? what's preventing you from avoiding them if you are so concerned about inflation? the answer is nothing, except again, in the marginal case, perhaps capital-gains taxes that you could likely avoid if you put your mind to it. I understand you're trying to suggest that inflation shouldn't be a problem, because it's avoidable. But I believe you've missed my point. Do you think the average person throughout the 20th century managed their finances with an eye toward inflation? If you do, may I suggest you have a rather generous view of "the average person throughout the 20th century?" Think of the people who were present during the transition in 1913. They were used to a monetary system that was totally fixed to precious metals. Do you think most of them knew, and really understood, that first their paper dollars were going to be devalued in 1933, and then continually devalued from then on, all due to the deliberate actions of men, rather than natural market forces? Think of poorer people who didn't have access to a lot of wealth, and hence much of the wisdom regarding it's proper handling. Think of grandpa stuffing money under the mattress because he didn't trust banks. Think of the poor family who diligently saved their coins (and even the occasional bill!) in a large jar as an emergency fund for when times got bad, trying to improve their condition. Think of people NOW who may not have a 401k or a stock broker, but have a money market savings account, and think that they're doing well because of it. These people all got--and are getting--screwed. If your attitude is that they're just not educated, then you're forgetting that education isn't free ("free" public education is the worst) and that even then there's much pressure to miseducate. Many people of modest means know they need to save to get ahead. But the Keynesian crap pushed in the classroom doesn't give them the tools to realize just saving dollars isn't enough, and that one of the best ways to save and avoid inflation is through that "relic" called gold. If your attitude is that, well, some folks are just less intelligent, and can't be helped, then we have a problem. Fifty percent of any given society is going to be of less than average intelligence. What sort of man-made system requires us to take 50% of the population and just accept they're going to get robbed annually by their central bank? Especially considering this 50% is frequently the less-well-off? That's my main beef with an centralized, inflationary monetary system. It's bad enough that it steals, moreso from the poorer and less educated. It's that at its core it's a fundamentally dishonest system, and one that to some extent (thanks to legal tender laws) is forced onto the society. It's just plain wrong, regardless of whether I can personally figure out how to beat it. Title: Re: Down to zero it goes! Post by: bitcoin0918 on June 26, 2011, 03:55:05 AM nobody received a dollar in 1913 and expected it to have the same purchasing power in 1999. That's extraordinarily disingenuous of you. The expectation of the day was CERTAINLY NOT that the dollars they were accepting in 1913 would be lose more than 90% of their value in less than 90 years. Title: Re: Down to zero it goes! Post by: bitcoin0918 on June 26, 2011, 04:07:46 AM westkybitcoins: excellent post!

Title: Re: Down to zero it goes! Post by: unk on June 26, 2011, 04:14:21 AM Quote from: foggyb That's extraordinarily disingenuous of you. The expectation of the day was CERTAINLY NOT that the dollars they were accepting in 1913 would be lose more than 90% of their value in less than 90 years. they could have simply asked their grandparents, as a similar phenomenon described the previous ninety years. inflation in the united states is generally recognised to have been greater from 1913 to 1999, but not by as much as the often-disputed '90%' figure would have you believe. (probably it was about twice as great in the 20th century as the 19th century, though i'm saying that offhand without looking at the best data.) more to the point, very few people held dollars outside of interest-bearing accounts, particularly after the federal deposit guarantees that followed the great depression in the united states. as ribuck pointed out, most people matched or beat inflation in practice, with those interest-bearing accounts. my point is that to focus on the inflation of the currency, out of context, is itself 'extraordinarily disingenuous'. i want to avoid the inline quoting in the rest of the responses, so i'll just address your points in freeform. first, social security has nothing to do with what we're talking about. if you want to say that social security isn't sufficiently adjusted for inflation, that's fine, but again, that is not an indictment of monetary policy. if social security were properly adjusted for inflation, your concern here would fall away. (please, though, let's not have a general debate about social security. i recognise the american tea party calls it a 'ponzi scheme' and that those views are common in this forum. it's a profoundly and tragically misguided understanding of the system, but i don't want to debate that in detail here.) second, i referenced my 'credentials' (not really; i just made a claim that i knew what i was talking about) only because you suggested that i ought to be ignored, incorrectly terming my analysis 'feelings' that ought to be easily dismissed. i'd never have brought anything personal about myself up if you'd responded to my analysis instead of dismissing it as coming from someone inappropriately emotional, which is of course far from the truth. third, and probably most importantly, interest rates do affect riskfree savings, but their effect is largely to shift riskfree savings to 'investments'. in practice, empirically, they do not substantially decrease 'savings' as opposed to 'spending'. if all they do is shift around what 'saved' money does, then we're back to the point i've been making all along: nobody is forced to experience the inflation of the dollar, and their choice of other instruments (such as commodities) does not significantly distort the economy. note also that you're criticising low interest rates, which ordinarily do not coincide with inflation. you may be upset at a particular feature of the monetary landscape over the last few years, and other actions of the central banks of major industrialised countries, that have little to do with inflation. as i have said from the start, i'm not telling you that you should not oppose all central banks' decision. i'm just telling you that you're opposing the wrong ones. westkybitcoins: for much of the period you're describing, the group of 'middle class' americans to which you're referring held extremely little cash, and they held essentially none outside interest-bearing accounts with which they matched or even beat inflation. furthermore, many such families 'saved' in non-cash assets, such as a family house. to be clear, however, i'm not disputing that inflation takes from some people and gives from others. that's true of anything, however; it's true, of deflation too, for example. who benefits and who suffers is a detailed empirical question that requires nuanced analysis to answer, just like questions about the true incidence of a new tax. for instance, if we all used bitcoins, the eventual presumed deflation would affect salaried laborers versus investors in very complicated ways that are hard to predict based merely on the notion of 'deflation', for they would depend on many other macroeconomic and psychological factors. (for example, how sticky are wages? how are pensions computed?) to answer these questions with ideological generalities will almost always lead to wrong answers and bad decisions. Title: Re: Down to zero it goes! Post by: bitcoin0918 on June 26, 2011, 04:39:22 AM Unk: There is no free lunch. You cannot inflate a currency without consequence. Even if every citizen was capable of minimizing the loss of purchasing power, that purchasing power would still be seized from the rest of the world through treasury bills. As the rest of the world realizes that the US is increasingly printing money and issuing new debt just to pay the interest on past debt, the US will lose its reserve currency status, and nobody will want our debt. Then all of the government programs we have come to rely on will fail, and we (the private sector) will have to create and fund those programs ourselves, reducing our standard of living.

You can say that the specific inflationary policy alone does not cause all of this grief, but that policy was not enacted in a vacuum, and is what allows all of these problems to become possible. Quote you suggested that i ought to be ignored, incorrectly terming my analysis 'feelings' that ought to be easily dismissed. I only suggested that your claim that the community is feeling more "amateurish" and "fringe" be ignored.Title: Re: Down to zero it goes! Post by: iya on June 26, 2011, 05:04:40 AM http://static.seekingalpha.com/uploads/2009/3/9/saupload_dollar_value_chart.png

What is the chart actually showing? Dollar in $ makes no sense to me. @unk I agree with you theoretically, and I always recommend holding only as much currency as needed for monthly expenses. If most people would do that, the central bank had less influence. But I don't think it's as easy as you make it out to be. We get bubble after bubble in things that seem to be good assets, but actually aren't. Gold is the only "hands-off" store of wealth, and in many countries it's legally impossible or expensive to acquire. In case of emergency it will likely get confiscated. The main problem with central banks, fiat money and government debt is the illusion of wealth they create. When the economic distortions can no longer be hidden/ignored, people always blame scapegoats. For example the Greeks are angry at the prospect of becoming poorer, while, in fact, they were never as rich as they believed to be. Would you argue that there is no "debt supercycle", and that for example the US deficit is no big deal? Title: Re: Down to zero it goes! Post by: marcus_of_augustus on June 26, 2011, 05:13:39 AM Quote i still bristle when i see people in these forums angry at the inflation of fiat currencies. the comparison to bitcoins is misleading. nobody received a dollar in 1913 and expected it to have the same purchasing power in 1999. and during the inflation that the original poster's chart shows, the united states was, with a handful of exceptions, both prospering and increasing its prosperity; the inflation of the money supply did not stop that. moreover, as i've tried to explain before, monetary policy does not force inflation's effects on people; anyone could purchase other assets (though not with infinite flexibility, given the outlawing of private holding of gold, which is a more serious regulatory intrusion than monetary inflation) with their cash if they wanted to avoid the effects of inflation. other regulations, including tax laws, have imposed limits on people's abilities to invest arbitrarily, but that is not the fault of monetary policy. the anger at the 'inflation' of 'fiat currencies' is, for these reasons, rather bizarre, and honestly the frequency with which it's repeated here increases the amateurish and fringe feel of the community. there are a lot of things to be angry at central banks for. that the dollar inflated throughout the 20th century is not one of them. yet again unk proves he wrong, wrong, more wrong and full of wind ... bristling or otherwise ... tax laws and monetary policy are bound at the hip by the same people creaming it off the top ... supporting a failed system must leave one feeling dirty and guilty at some point ... surely? Title: Re: Down to zero it goes! Post by: airdata on June 26, 2011, 05:32:26 AM ROFL.

Well played sir :) 5 star thread !!! Title: Re: Down to zero it goes! Post by: westkybitcoins on June 26, 2011, 05:41:50 AM westkybitcoins: for much of the period you're describing, the group of 'middle class' americans to which you're referring held extremely little cash, and they held essentially none outside interest-bearing accounts with which they matched or even beat inflation. furthermore, many such families 'saved' in non-cash assets, such as a family house. to be clear, however, i'm not disputing that inflation takes from some people and gives from others. OK. Fair enough that you don't dispute it. Let's just focus on that then. Quote that's true of anything, however; it's true, of deflation too, for example. who benefits and who suffers is a detailed empirical question that requires nuanced analysis to answer, just like questions about the true incidence of a new tax. for instance, if we all used bitcoins, the eventual presumed deflation would affect salaried laborers versus investors in very complicated ways that are hard to predict based merely on the notion of 'deflation', for they would depend on many other macroeconomic and psychological factors. (for example, how sticky are wages? how are pensions computed?) to answer these questions with ideological generalities will almost always lead to wrong answers and bad decisions. Three points. First, let's look at "who benefits and who suffers." In a centralized, inflationary monetary system, this is pretty clear. The primary beneficiary is the one who gets to create more money (or I suppose more accurately, those immediately able to use the new money in exchange for goods and services at full value. This could be the central bank itself. This could be the entities bailed out via newly minted cash.) The primary suffering are those forced to hold the money, those holding it out of ignorance, and those holding it out of necessity--the system as it is requires us all to use dollars for our everyday needs. There will always be some of these people. In fact, for the monetary system to actually function, the money MUST be in someone's hands. And those someones get screwed. What about with bitcoins? Well, remember that the bitcoin network doesn't go and periodically destroy bitcoins. There's simply a cap on the number of them that will ever exist. So the primary beneficiaries of any deflation are ALL the voluntary holders of bitcoins. So far, no problem there, is there? And the primary suffering in this case? Those who lose their bitcoins. Please take a second and think about how ingenious that is. Some people will irretrievably lose their money in ALL monetary systems. Under inflation, these people lose 100% of their lost money, and will also lose some % of their remaining money due to their central bank. Under a non-inflationary money, these people still lose 100% of their lost money, but they gain some % of that value back in their remaining money. Even if they have no remaining money, then they've just broken even with the inflationary system... they certainly didn't fare any worse for it. This reduces the group of sufferers to the ideal, most fair group... those who would have lost purchasing power anyway. They are demonstrably never worse off than they would be under an inflationary system, and periodically are better off. This arrangement seems far, far superior to one where the politically connected profit at the expense of the poor, the uneducated and the coerced. Second, there's a big difference in how any transfer of wealth occurs under an inflationary and a non-inflationary system. In a non-inflationary system, any wealth transfer can only be initiated by the person who would lose their purchasing power... for example, those who lose their bitcoins. Call such a situation what you will, but at best, their loss of purchasing power is an accident, at worst, it's just their own fault. Under an inflationary system, the wealth transfer can be initiated pretty much at will by those who would gain the purchasing power. Which is so ripe for abuse it stinks. Moreover, that purchasing power comes AT THE EXPENSE of the suffering. And remember: for the monetary system to even work, SOMEONE has to be holding the money, so there is NECESSARILY a patsy. Before we started redefining terms in western society, we used to call that sort of a wealth transfer theft. And considering it's a system forced onto some segment of the society or another, I prefer to just call it getting screwed. Third, there's something far more fundamental we're overlooking. Our opinions on the issue don't matter. The fact is: people choose non-inflationary systems. You can call that stupidity, ignorance, cowardice, whatever. People do. They do it over and over, every time. They choose non-inflation over inflation. This is proved by the fact that governments have to resort to legal tender laws and having tax payments required to be in their own currency. Gresham's law ceases to exist in the absence of coercion. Thought experiment: go to a nation, any nation. Give them a choice: they can transact in a non-inflationary fiat money, or some other inflationary fiat money, or even both, with all contracts and debts honored equally. They can pay taxes in either form of money they wish. Of course, they still can have access to all the other means of asset protection; just ensure there will be no penalties or punishments given to them for choosing one fiat money over the other in regular use. Oh, and don't bar anyone from informing others about the true natures and consequences of each. Which of the fiat monies do you think people will choose? Seriously, is there even any question? So say what we will, people have spoken. They don't want inflationary monies. THE MASSES DISAGREE WITH YOUR ASSESSMENT OF THE ILLS OF A NON-INFLATING CURRENCY. They only deal with it because it's forced down their throat by people who feel the need to save them from themselves. But considering that (a) they're the ones who have to use it, and (b) the whole issue is supposedly about what's in their best interests... I'd say the people themselves are best suited to determining what is best for them. Title: Re: Down to zero it goes! Post by: unk on June 26, 2011, 05:47:28 AM yet again unk proves he wrong, wrong, more wrong and full of wind ... bristling or otherwise ... tax laws and monetary policy are bound at the hip by the same people creaming it off the top ... supporting a failed system must leave one feeling dirty and guilty at some point ... surely? i don't understand the point of comments like this; surely this is what people call a 'troll'? if not, it's just ignorant nonsense, almost glorying in its intentional, anti-intellectual ignorance. there are many ways to read up on the substantive and procedural differences between tax laws and monetary policy, in the united states and elsewhere. to criticise someone for separating them analytically reflects exactly the kind of tragically simpleminded worldview i'm faulting. iya: the chart compares the changing functional value of a dollar against its calculated value in 1776. i didn't previously take issue with the details of how inflation is calculated because the details are complex and contentious ('inflation' is not a singular phenomenon but a distributed one that can be measured in a variety of ways), but it may be worth pointing out that the particular chart is far from universally accepted. that said, nobody disputes that there has been dollar-inflation in the last 235 years. bitcoin0918: it's hard to disentangle the various points you're making; they don't relate to each other analytically. as far as i can tell, you're making a series of very specific but unsupported empirical predictions, and the only place i've seen those particular predictions is on various websites populated by amateur, self-styled economists. if you would be willing to specify the claims into concrete, testable predictions, i likely would be willing to bet substantial money against you, as would anyone who has studied the matter in more substantive detail than the various websites that foam at the mouth about the united states's impending doom after its currency fails to maintain its status as the functional global 'reserve'. if you think you can predict the specific actions of most national governments over the next twenty years in response to economic conditions that have not yet manifested themselves, you're probably wrong, or else you're a better economist than everyone who's worked in detail on related matters. in case the perspective helps, very few people (or perhaps no one) with a deeper understanding of global trade make the same strong predictions as the foam-at-the-mouth amateurs that you can find on various blogs. the only consistent response i've seen in this forum is that all those analysts must be 'brainwashed' because they 'suckle the teat of the state'. if that is a convincing argument to you, then we probably have nothing further to discuss. Title: Re: Down to zero it goes! Post by: unk on June 26, 2011, 06:05:01 AM First, let's look at "who benefits and who suffers." In a centralized, inflationary monetary system, this is pretty clear. The primary beneficiary is the one who gets to create more money (or I suppose more accurately, those immediately able to use the new money in exchange for goods and services at full value. This could be the central bank itself. This could be the entities bailed out via newly minted cash.) just as an example, bailouts of banks are an extremely recent phenomenon and have little to do with historical inflation. i've never criticised anyone who opposed bailing out the banks. i simply insist that people who criticise the very existence of central banks at least try to learn, in detail, how newly created funds enter the monetary system. almost nobody here seems to manifest that understanding, but that doesn't stop them from criticising the system they don't understand. Quote What about with bitcoins? Well, remember that the bitcoin network doesn't go and periodically destroy bitcoins. There's simply a cap on the number of them that will ever exist. So the primary beneficiaries of any deflation are ALL the voluntary holders of bitcoins. So far, no problem there, is there? And the primary suffering in this case? Those who lose their bitcoins. Please take a second and think about how ingenious that is. ah, the near-religious faith in the 'ingenious' design of bitcoin. as i've demonstrated many times before, i've studied the code in detail and have commented on its strengths and weaknesses; i don't need to sit and reflect on its ingenuity. nothing about bitcoin depends on a shift of wealth from those who lose funds to those who keep them. indeed, bitcoin would probably be stronger, rather than weaker, if there were a convenient way to recover funds that were lost, as some developers have proposed via a 'keepalive'-like system or a variety of other mechanisms. (strictly speaking, 'deflation' is a bit imprecise when applied to a system where the money supply stays constant, and 'non-inflation' would be a more precise term, but i'm using 'deflation' the way most people do in this forum - that is, in a way, that does not at all depend on funds being lost by people who corrupt their wallets.) the wealth transfers i was talking about are more complex than what i think you have in mind. for example, in a non-inflationary system, wages will need to fall as prices fall, and wealth will be transferred based on the relative rates at which they fall. note that the relative rates cannot be derived theoretically, because in the real world they depend on complex macroeconomic and psychological factors. if you propose a world with no transaction costs and perfectly competitive markets, you propose an ideal world that doesn't exist, and the economic conclusions you reach won't be particularly useful in our world. Quote Third, there's something far more fundamental we're overlooking. Our opinions on the issue don't matter. The fact is: people choose non-inflationary systems. You can call that stupidity, ignorance, cowardice, whatever. People do. They do it over and over, every time. They choose non-inflation over inflation. This is proved by the fact that governments have to resort to legal tender laws and having tax payments required to be in their own currency. it's absolutely not proved by that; many other things explain legal-tender laws, both historically and conceptually. if you adopt this sort of reasoning, you just assume your conclusion. the point i've made many times in this forum, in much greater detail, is that the inflation or deflation of a monetary instrument doesn't matter at all for investment decisions unless you take into account contextual factors, because if you're occupying an ideal theoretical realm, the inflation or deflation of competing instruments can be priced into the instruments. in the 'real world', of course, that pricing is imperfect, but that doesn't mean that inflation or deflation magically 'wins', and there's absolutely no historical evidence to bear out the kind of phenomenon you're describing (the systematic preference by large populations for deflationary currency instruments). Quote Gresham's law ceases to exist in the absence of coercion. Thought experiment: go to a nation, any nation. Give them a choice: they can transact in a non-inflationary fiat money, or some other inflationary fiat money, or even both, with all contracts and debts honored equally. They can pay taxes in either form of money they wish. Of course, they still can have access to all the other means of asset protection; just ensure there will be no penalties or punishments given to them for choosing one fiat money over the other in regular use. Oh, and don't bar anyone from informing others about the true natures and consequences of each. Which of the fiat monies do you think people will choose? Seriously, is there even any question? you're forgetting that the exchange rate between the two will matter, as well as the relatively riskfree interest available in both. you can't compute the merits of the competing instruments without considering those factors. Quote So say what we will, people have spoken. They don't want inflationary monies. THE MASSES DISAGREE WITH YOUR ASSESSMENT OF THE ILLS OF A NON-INFLATING CURRENCY. They only deal with it because it's forced down their throat by people who feel the need to save them from themselves. i think you're just repeating this point over and over, but which masses? where? if your economic understanding of the foreign-currency markets is coming from the wikipedia page on gresham's law, note that at present it's simply an unjustified tirade against legal-tender laws, as many people in the 'talk' page of the article have pointed out. Title: Re: Down to zero it goes! Post by: MoonShadow on June 26, 2011, 06:07:26 AM Quote from: foggyb That's extraordinarily disingenuous of you. The expectation of the day was CERTAINLY NOT that the dollars they were accepting in 1913 would be lose more than 90% of their value in less than 90 years. they could have simply asked their grandparents, as a similar phenomenon described the previous ninety years. inflation in the united states is generally recognised to have been greater from 1913 to 1999, but not by as much as the often-disputed '90%' figure would have you believe. (probably it was about twice as great in the 20th century as the 19th century, though i'm saying that offhand without looking at the best data.) You're saying this without access to any factual data. It's simply not true. The US Dollar prior to 1913 did have it's ups and downs, but the general trend over the prior century was deflationary, if only very mildly. It would be tricky to have an inflating currency that wasn't just on a bi-metal standard, the currency was actually the metal. Try and imagine the world before 1913, for the most part paper money didn't really exist. All those old Westerns showing thieves robbing banks and getting away with paper money were wrong. A dollar was (and legally still is, look it up) a defined weight in gold, while coins were made of the silver itself. Paper money was rare. Title: Re: Down to zero it goes! Post by: MoonShadow on June 26, 2011, 06:10:43 AM First, let's look at "who benefits and who suffers." In a centralized, inflationary monetary system, this is pretty clear. The primary beneficiary is the one who gets to create more money (or I suppose more accurately, those immediately able to use the new money in exchange for goods and services at full value. This could be the central bank itself. This could be the entities bailed out via newly minted cash.) just as an example, bailouts of banks are an extremely recent phenomenon and have little to do with historical inflation. i've never criticised anyone who opposed bailing out the banks. i simply insist that people who criticise the very existence of central banks at least try to learn, in detail, how newly created funds enter the monetary system. almost nobody here seems to manifest that understanding, but that doesn't stop them from criticising the system they don't understand. That's quite an assumption to make about your detractors. I consider it more likely that you don't understand a system that you advocate. You might know bitcoin inside and out, but you still don't understand that which you speak. Title: Re: Down to zero it goes! Post by: unk on June 26, 2011, 06:21:00 AM That's quite an assumption to make about your detractors. I consider it more likely that you don't understand a system that you advocate. You might know bitcoin inside and out, but you still don't understand that which you speak. it's not an assumption; as i said, it's an observation based on what's manifested. perhaps people here are just poor at communicating their understanding, but i see no indications of a detailed understanding of the operation of central banks. you may be right about the particulars of deflation in 1800s america; the united states is not my home or my speciality. if so, i retract that particular point, but very little depends on it. my larger point is still that very few actually suffered substantially from inflation from 1913 onward, because most people who had a bank account were able to match or outpace inflation. the more general point is that the amateur economists in this forum seem implicitly to be comparing (1) bitcoins with (2) dollars held under a mattress. the more accurate comparison, however, is with (3) dollars held in a bank account, earning interest. the chart for most 'savers', even those who never opened a brokerage account, would not be close to the original poster's once interest were taken into account. it is only recently that it was hard to match inflation in a bank account, and the reason for that has more to do with the unique failures of central banks over the last few years than the generalised problems that people here want to assign to all central banks everywhere, throughout time. of course, that's a classic mistake that many anti-government extremists make ('i can point to a bad thing that a government did, therefore governments should not exist'). perhaps i shouldn't draw myself into another debate with a horde of anti-governmental extremists, however. i realise that i am in the minority in this forum by not belonging to that group. Title: Re: Down to zero it goes! Post by: foggyb on June 26, 2011, 06:22:25 AM they could have simply asked their grandparents, as a similar phenomenon described the previous ninety years. inflation in the united states is generally recognised to have been greater from 1913 to 1999, but not by as much as the often-disputed '90%' figure would have you believe. (probably it was about twice as great in the 20th century as the 19th century, though i'm saying that offhand without looking at the best data. Thanks for helping my case. ;) more to the point, very few people held dollars outside of interest-bearing accounts. Nearly everyone's good fortunes rest on the stability of the US dollar, today.That's the point. Title: Re: Down to zero it goes! Post by: MoonShadow on June 26, 2011, 06:33:40 AM it is only recently that it was hard to match inflation in a bank account, and the reason for that has more to do with the unique failures of central banks over the last few years than the generalised problems that people here want to assign to all central banks everywhere, throughout time. Well, that's just it. The recent failures of central banking over the last few years were not only not unique, they were entirely predictable from the moment the central banks shed the discipline of the gold standard and thus gained the power to inflate. That is what happens to all fiat currencies. It always has. Just because we are finally starting to see the fatal imbalances in the system accumulate to a visible level, doesn't mean that those imbalances were not there from the start. They were, and I believe that you are smart enough to understand that. The cognative dissonance that you are experiencing within this forum is not a unique affliction. Most people very much desire to believe that the society that they live within is a predominately honest one, and that the image that it presents to us is not fraudulent. I'm sorry to be the one to tell you this, but what you have been told since you were a child, what your parents believed, and what you believe about the best intentions of those who command these vast monetary systems is a lie. Title: Re: Down to zero it goes! Post by: unk on June 26, 2011, 06:47:36 AM it is only recently that it was hard to match inflation in a bank account, and the reason for that has more to do with the unique failures of central banks over the last few years than the generalised problems that people here want to assign to all central banks everywhere, throughout time. Well, that's just it. The recent failures of central banking over the last few years were not only not unique, they were entirely predictable from the moment the central banks shed the discipline of the gold standard and thus gained the power to inflate. That is what happens to all fiat currencies. It always has. Just because we are finally starting to see the fatal imbalances in the system accumulate to a visible level, doesn't mean that those imbalances were not there from the start. They were, and I believe that you are smart enough to understand that. The cognative dissonance that you are experiencing within this forum is not a unique affliction. Most people very much desire to believe that the society that they live within is a predominately honest one, and that the image that it presents to us is not fraudulent. I'm sorry to be the one to tell you this, but what you have been told since you were a child, what your parents believed, and what you believe about the best intentions of those who command these vast monetary systems is a lie. but do you honestly think that kind of general, simplistic statement is convincing? merely because you claim something and present it as revolutionary doesn't make it correct. you're asserting things seemingly in response to very particular analysis i've offered showing that both inflation and deflation can be priced into alternative currencies, which can then be chosen freely as competing investments, at least in the absence of transaction costs. that cold analysis is what i 'believe', not what my 'parents' told me about central banks. note that i'm not one of the people whose knee-jerk reaction was 'bitcoin can't work because it's deflationary'. my response was instead 'they're all mistaken to think it matters; it doesn't, on either side'. in any event, one of the most frustrating things about anti-government extremists is their perception of themselves as visionaries who see truths that nobody else sees. the reality is that most of us flirted with similar ideas in our teenage years and then outgrew them, faced with the complex realities of the world and the recognition that not everything has simple answers. i hate to sound condescending, but outside internet message boards like this one, adjectives like 'juvenile' and 'sixth-form' come up much more often than 'idealist' or 'visionary' to describe that kind of extremism. and that is not because anyone feels threatened or surprised, and it is not because everyone outside this message board is corrupt or otherwise undermined. Title: Re: Down to zero it goes! Post by: westkybitcoins on June 26, 2011, 07:12:56 AM First, let's look at "who benefits and who suffers." In a centralized, inflationary monetary system, this is pretty clear. The primary beneficiary is the one who gets to create more money (or I suppose more accurately, those immediately able to use the new money in exchange for goods and services at full value. This could be the central bank itself. This could be the entities bailed out via newly minted cash.) just as an example, bailouts of banks are an extremely recent phenomenon and have little to do with historical inflation. i've never criticised anyone who opposed bailing out the banks. i simply insist that people who criticise the very existence of central banks at least try to learn, in detail, how newly created funds enter the monetary system. almost nobody here seems to manifest that understanding, but that doesn't stop them from criticising the system they don't understand. OK. Do you agree that the primary beneficiary in a centralized, inflationary monetary system is the one who gets to create more money? If not, who is the primary beneficiary? Quote Quote What about with bitcoins? Well, remember that the bitcoin network doesn't go and periodically destroy bitcoins. There's simply a cap on the number of them that will ever exist. So the primary beneficiaries of any deflation are ALL the voluntary holders of bitcoins. So far, no problem there, is there? And the primary suffering in this case? Those who lose their bitcoins. Please take a second and think about how ingenious that is. ah, the near-religious faith in the 'ingenious' design of bitcoin. as i've demonstrated many times before, i've studied the code in detail and have commented on its strengths and weaknesses; i don't need to sit and reflect on its ingenuity. nothing about bitcoin depends on a shift of wealth from those who lose funds to those who keep them. indeed, bitcoin would probably be stronger, rather than weaker, if there were a convenient way to recover funds that were lost, as some developers have proposed via a 'keepalive'-like system or a variety of other mechanisms. (strictly speaking, 'deflation' is a bit imprecise when applied to a system where the money supply stays constant, and 'non-inflation' would be a more precise term, but i'm using 'deflation' the way most people do in this forum - that is, in a way, that does not at all depend on funds being lost by people who corrupt their wallets.) the wealth transfers i was talking about are more complex than what i think you have in mind. for example, in a non-inflationary system, wages will need to fall as prices fall, and wealth will be transferred based on the relative rates at which they fall. note that the relative rates cannot be derived theoretically, because in the real world they depend on complex macroeconomic and psychological factors. if you propose a world with no transaction costs and perfectly competitive markets, you propose an ideal world that doesn't exist, and the economic conclusions you reach won't be particularly useful in our world. OK. (1) Who initiates these wealth transfers in a non-inflationary system? (2) Who SHOULD be the initiator of these wealth transfers in a monetary system? Quote Quote Third, there's something far more fundamental we're overlooking. Our opinions on the issue don't matter. The fact is: people choose non-inflationary systems. You can call that stupidity, ignorance, cowardice, whatever. People do. They do it over and over, every time. They choose non-inflation over inflation. This is proved by the fact that governments have to resort to legal tender laws and having tax payments required to be in their own currency. it's absolutely not proved by that; many other things explain legal-tender laws, both historically and conceptually. if you adopt this sort of reasoning, you just assume your conclusion. the point i've made many times in this forum, in much greater detail, is that the inflation or deflation of a monetary instrument doesn't matter at all for investment decisions unless you take into account contextual factors, because if you're occupying an ideal theoretical realm, the inflation or deflation of competing instruments can be priced into the instruments. in the 'real world', of course, that pricing is imperfect, but that doesn't mean that inflation or deflation magically 'wins', and there's absolutely no historical evidence to bear out the kind of phenomenon you're describing (the systematic preference by large populations for deflationary currency instruments). Quote Gresham's law ceases to exist in the absence of coercion. Thought experiment: go to a nation, any nation. Give them a choice: they can transact in a non-inflationary fiat money, or some other inflationary fiat money, or even both, with all contracts and debts honored equally. They can pay taxes in either form of money they wish. Of course, they still can have access to all the other means of asset protection; just ensure there will be no penalties or punishments given to them for choosing one fiat money over the other in regular use. Oh, and don't bar anyone from informing others about the true natures and consequences of each. Which of the fiat monies do you think people will choose? Seriously, is there even any question? you're forgetting that the exchange rate between the two will matter, as well as the relatively riskfree interest available in both. you can't compute the merits of the competing instruments without considering those factors. Quote So say what we will, people have spoken. They don't want inflationary monies. THE MASSES DISAGREE WITH YOUR ASSESSMENT OF THE ILLS OF A NON-INFLATING CURRENCY. They only deal with it because it's forced down their throat by people who feel the need to save them from themselves. i think you're just repeating this point over and over, but which masses? where? if your economic understanding of the foreign-currency markets is coming from the wikipedia page on gresham's law, note that at present it's simply an unjustified tirade against legal-tender laws, as many people in the 'talk' page of the article have pointed out. I really didn't think you would even dispute this. I actually thought "no one would publicly try to defend the idea that the majority of people would voluntarily choose an inflationary currency over a non-inflationary one." Once I saw that you did, I even got ready to ask you what sort of evidence you were going to accept to the contrary, and to spend time accumulating it for this post. But I have a better idea.... Let's presume for the moment that you might be right. That people, in general, naturally gravitate toward an inflationary currency as opposed to a non-inflationary one. If so, would you advocate for the abolition of legal tender laws and of the mandatory payment of taxes in a government-created medium of exchange? That would seem to be the most important point here. If yes, then good, I agree with you. Let's just see for ourselves the result. If no, then why not, if doing such wouldn't result in an exodus of people from inflationary currencies anyway? (EDIT: Slight tonal adjustment) Title: Re: Down to zero it goes! Post by: bitcoin0918 on June 26, 2011, 12:29:37 PM Unk: you have repeatedly stated that inflation is not a problem. Please answer the following:

1. Why is the Federal Reserve inflating the currency? I am not asking you to regurgitate their mandate, because they are far exceeding the 2% price inflation target. So why are they doing it? 2. When the Fed creates money to buy bonds - whether from the treasury or financial institutions holding subprime mortgages - is the Fed overpaying for those bonds? If not, then why must the Fed even step in to buy anything? Certainly there is a buyer at the right price, no? 3. What do the entities that receive this money do with it? Whether in the case of the government, or on-the-brink financial institutions, is the money put to the most productive value, given the scarce resources toward which that capital will be directed? Side note: please stop with all of the snide remarks about "juvenile", "foaming at the mouth", "simplistic", etc. If you are unable to effectively state your case, leave it at that. Do not try to win people over by fallacious reasoning. Title: Re: Down to zero it goes! Post by: MoonShadow on June 26, 2011, 02:00:28 PM it is only recently that it was hard to match inflation in a bank account, and the reason for that has more to do with the unique failures of central banks over the last few years than the generalised problems that people here want to assign to all central banks everywhere, throughout time. Well, that's just it. The recent failures of central banking over the last few years were not only not unique, they were entirely predictable from the moment the central banks shed the discipline of the gold standard and thus gained the power to inflate. That is what happens to all fiat currencies. It always has. Just because we are finally starting to see the fatal imbalances in the system accumulate to a visible level, doesn't mean that those imbalances were not there from the start. They were, and I believe that you are smart enough to understand that. The cognative dissonance that you are experiencing within this forum is not a unique affliction. Most people very much desire to believe that the society that they live within is a predominately honest one, and that the image that it presents to us is not fraudulent. I'm sorry to be the one to tell you this, but what you have been told since you were a child, what your parents believed, and what you believe about the best intentions of those who command these vast monetary systems is a lie. but do you honestly think that kind of general, simplistic statement is convincing? Of course not. I don't think that you could be convinced of anything. You have a strong belief system, and are unlikely to accept any evidence to the contrary of that belief system. It's like trying to convince a muslim from afganistan that a Catholic is correct. It doesn't really happen. Very few people who grow up surrounded by such a particular belief are going to be able to break free from it, Title: Re: Down to zero it goes! Post by: unk on June 26, 2011, 03:56:48 PM Of course not. I don't think that you could be convinced of anything. You have a strong belief system, and are unlikely to accept any evidence to the contrary of that belief system. It's like trying to convince a muslim from afganistan that a Catholic is correct. It doesn't really happen. Very few people who grow up surrounded by such a particular belief are going to be able to break free from it, oh, the irony, since you just accused me of making strong assumptions about my interlocutors (which i indeed wasn't even doing). as i just finished saying in my last message, my beliefs have evolved substantially since i was a teenager. have yours? do you actually read, in the present day, sophisticated positions that disagree sharply with yours and consider their merits? again, i do, and indeed that's roughly my half-time job. are you anti-intellectual enough to think that my intellectual focus on the subject necessarily corrupts my reasoning so that i cannot see the faults of governments and must merely accept them as the 'slave' that libertarians must imagine i am? you appear to be stuck in tragically simple generalities. there's apparently almost no content to your position, other than an anger at largely unspecified governmental forces. are you a member of the american tea party? it would be consistent with the many guns you've claimed you keep in the event of governmental collapse. the tea party is not known for its intelligence or sensitivity, to put it mildly. almost all smart people who care about political economy (1) consider extreme libertarianism in their youth and then (2) reject it on its merits in favour of something more nuanced. if all nuance is necessarily your enemy, it's hard to take your position seriously. westkybitcoins: my point, which i've spelled out many times now, is that the legal tender laws aren't as significant as you're making them out to be. they simply don't matter much, because they don't force long-term holding of any currency, and they don't prevent any significant trade. i couldn't care less whether they're repealed, and my prediction is that it would make very little difference empirically if they were. suppose that the laws said that in addition to any other agreed-upon forms of payment, large merchants needed to accept online bill payments in the customer's choice of major currencies to satisfy debts. that is a 'legal-tender' law, and nonetheless it would be a minor procedural rule and wouldn't make much of a difference beyond the payments industry. legal-tender laws are quite similar in scope and effect. if your concern is human liberty, you're simply picking the wrong regulatory targets to critique. if i wanted to be a demagogue for effect, i could make the same sort of conspiracy-theory-laden points as people commonly do in this forum: wouldn't the 'state' much prefer that you be complacent about the real, more significant threats to your liberty and have you spend all your time focusing on a mostly irrelevant procedural law about how payments have to be made before they're converted voluntarily into other instruments by anyone who cares? surely you want to pick the right thing to criticise; i'm trying to suggest that you be more careful about the ones you choose. bitcoin0918: i'm not sure what the point of your questions is. i can't read the mind of the central bankers in a foreign country. what relevance would my answers have to the larger analytical points i've made? note that i've never said that central banks are perfect, that they can't be corrupted, etc. perhaps you assume that that's what i think, because i'm not willing to suggest abolishing them entirely? if so, that would be an incorrect assumption. i'm just trying to explain that a system should be criticised for the problems it has, rather than made-up ones. the critique of a system should go no further than the problems it has; the proper response to an imperfect system isn't always to try to destroy it. Title: Re: Down to zero it goes! Post by: HappyFunnyFoo on June 26, 2011, 04:18:57 PM For fun's sake, let's compare dollars to gold