Now that the first batch is going to sell out and it looks like Cryptx isn't going to have to buy any shares, we need to try and convince Cryptx to make the same deal again (with the second batch). Not only is that a huge boon to all investors, but it properly aligns Cryptx's incentives with the goals of all share holders.

Personally, I was much more comfortable thinking he was going to be buying shares, I'm sure others felt the same.

Cryptx, what say you?

Agreed, I think most investors would feel a lot more comfortable if cryptx owned a bunch of shares +1, +2 +3 +4 +5 +6 +7 C-C-C-COMBO BREAKERRRRRRRRRRRR  +9 |

|

|

|

|

tomorrow i will try to make functions for

$/BTC

Difficulty

cost$/Gh/s

w/Gh/s

on the spreadsheet

|

|

|

|

|

if new shareholders buy at 0.095 they might be inclined to buy more once trading opens at a lower share price

we will just have to wait and see how it all balances out

we might just manage to get through the current ipo block and up to the next share price

|

|

|

|

The reason dividends were going up was due to initial deployment not because reinvestment could keep up with difficulty rise. Leaving the reinvestment rate alone means investors lose less, and you still make a healthy profit.

Spot on! In the case of 65/35 dividend/reinvestment we cannot keep up with difficulty. This is why we are doing this IPO and changing our strategy, so we do keep up with difficulty and be able to grow large. But this new reinvestment plan can only keep up with difficulty until August 4, 2014, as seen in your forecast in the prospectus. After that date we are in the exact same situation with not being able to keep up with the difficulty using just reinvestment funds. The only way it can sustain is if there is a big price spike in BTC before that date to buy much more miners with reinvestment funds when the reinvestment is largest and network hashrate is lowest, but then a different problem arises. Are there any plans to to tackle this issue when it comes up again? thats only 1 view based on one projection you can generate thousands of multifactor exponential projections when considering everything i think they can keep up, because they have the ability to adapt, unlike your projection individuals miners have the same problems, yet we persist That is not an exponential projection, it is a linear network hashrate projection. This is also not my projection it is the projection done by CryptX in the prospectus. Individual miners have the same problem but they have the ability to reinvest 100% and not worry about splitting income with other people so it is more sustainable in the long run as a solo miner. The reason I bring CryptX's projection up is because his business plan is derived from how he thinks the project will do. And it can be seen in the forecast that his own plan will start to fall apart August 4, 2014 leading us back right to this issue. Also one issue with what you say is "..i think they can keep up.." You are putting faith into this mining operation because you are invested in it, not looking at what is laid out in front of you in the mine operators own forecast. If you are going to be posting silly projections that CryptX's business plan isn't based off of then there is no point in talking to you, lose all of your investment. There is also one fatal flaw in the chart you just posted it assumes a BTC price of $4,000 by the end of this month. again there is 0% certainty in the projection these factors are the one im talking about: $/BTC Difficulty cost$/Gh/s w/Gh/s can also influence the outcome $/kwh might aswell factor that in since it could change they can adapt, and their current strategy is the kind of strategy that is needed solo miners are not necessarily better off, they will have a harder time acquiring optimal reinvestment hashrate a large operation is more efficient at reinvestments |

|

|

|

The reason dividends were going up was due to initial deployment not because reinvestment could keep up with difficulty rise. Leaving the reinvestment rate alone means investors lose less, and you still make a healthy profit.

Spot on! In the case of 65/35 dividend/reinvestment we cannot keep up with difficulty. This is why we are doing this IPO and changing our strategy, so we do keep up with difficulty and be able to grow large. But this new reinvestment plan can only keep up with difficulty until August 4, 2014, as seen in your forecast in the prospectus. After that date we are in the exact same situation with not being able to keep up with the difficulty using just reinvestment funds. The only way it can sustain is if there is a big price spike in BTC before that date to buy much more miners with reinvestment funds when the reinvestment is largest and network hashrate is lowest, but then a different problem arises. Are there any plans to to tackle this issue when it comes up again? thats only 1 view based on one projection you can generate thousands of multifactor exponential projections when considering everything i think they can keep up, because they have the ability to adapt, unlike your projection individuals long-term miners have the same problems, yet we persist |

|

|

|

IMO Cryptx should have coincided the IPO with the addition of the new hash rate. I'm guessing the shares would be selling better if the extra 1000TH were online.

we will have additional hardware online before the IPO ends Just keep 0.0015 dividends and everything will go just fine.  only 2-3weeks of no dividend to endure we are on target for >50% yield even if we skip 4 weeks Way too optimistic. Unless there are some big whales buying ipo, or we are not going to see dividends until July/August. Even people follow this thread, not everyone knows this do good to investors. But if we continue 0.0015 dividends until debt is clear, many small investors would like to buy some shares. It's psychology. Because this move is good to the project, so we are able to pay the debt, dividends as usual is not a big deal. Then people are willing to buy in ipo, making this ipo more successful. Not like now, selling only 200 shares in 24 hours. And with a successful ipo, we should of course be able to pay dividends as usual. It's a positive cycle. you have been misinformed, cryptx has posted that it will take only 2 weeks to pay back the 1000btc loan with dividends + reinvestments and that means we will be at 84/16 on week 3, there is no need to try and manipulate psychology, people have been waiting for over 6 months from BFL for their cloud mining i have been waiting for 5 months now for my Monarch 600Gh/s |

|

|

|

IMO Cryptx should have coincided the IPO with the addition of the new hash rate. I'm guessing the shares would be selling better if the extra 1000TH were online.

we will have additional hardware online before the IPO ends Just keep 0.0015 dividends and everything will go just fine. only 2-3weeks of no dividend to endure we are on target for >50% yield even if we skip 4 weeks |

|

|

|

IMO Cryptx should have coincided the IPO with the addition of the new hash rate. I'm guessing the shares would be selling better if the extra 1000TH were online.

we will have additional hardware online before the IPO ends |

|

|

|

So if the IPO does not raise the needed funds , the old shareholders will pay with reduction in the dividend?

well its going to impact future size of reinvestment's which will have an impact on how efficiently we can maintain network share. IPO not raising all funds impacts all shareholders dividend will correspond to 15Gh/s no matter what, its only when considering long term impact we can see the negative impact, this will manifest in slower Gh/s per share increase |

|

|

|

so will PETA's cost/Gh/s go down as they increase the corresponding GH/s per share

look at butterflylabs, $10.83/Gh/s cloud hosting

They should, theoretically. Right now, PETA is at about $5.64 per GH/s (~7.55 GH/s per share @ BTC0.095). Assuming full deployment of 1.5PH/s, current share value ( BTC0.095) puts it at ~$1.88 per GH/s (at 66,371 outstanding shares)...but the more shares there are, the higher the 'price per GH/s' will be. Until full deployment happens, though, CoinTerra's new hosting plans range from $4.99 down to $2.75. And I'm not sure what KnC's plans are for hosting... we are currently guaranteed the 15Gh/s++ per share the current increase in shares will not have any diluting affect You are guaranteed >15GH/s, for now anyway, but an increase in the outstanding shares does have a diluting effect: 1,500,000 GH/s spread over 66,375 shares is ~22.6GH/s per share. 1,500,000 GH/s spread over 76,206 shares (selling out the current IPO) is ~19.68GH/s per share. Which would you rather have? no we are only getting a total hashrate according to how many ipo shares are sold, but it comes out as 15Gh/s per share they are putting up their own money, as a loan, to guarantee that regardless if any ipo shares are sold |

|

|

|

Hi guys, redditor here. Saw a post in there and I've been doing my research as I have some BTC to invest.

Most of it looks legit apart from well, apart from a few things.

1) is it true that the team that runs this project makes money from the electricity fees?

Does that not seem completely counter productive considering its completely against investor interests?

2) why is the reinvestment strategy set so poorly? It makes no sense at all to reinvest like that unless your trying to build up electricity no?

3) Also, my numbers are pretty poor, but is it actually 3$/GHs? Last time I checked you could buy hardware directly from the manufacturer for 1.5$/GH and they would even host it for you including costs for an extra 0.2$/GHs. How come the price difference is so huge, if your buying the best machines, where is all the extra funds going?

1) their solar project only provides 1-6% of the power used by the operation its not counter productive ,its beneficial if they can reduce their power costs 2) its not set poorly, their strategy will guarantee better ods of successful long term operation and larger dividends 3) if you want to manage hardware, electricity, bandwidth, reinvestments, deals, board assembly and other things required to maintain a large scale operation, you could, but i prefer leaving that to a company that has more experience and purchasing power the ipo is going towards funding the 1Ph purchase |

|

|

|

This was a bit painful to read, but it does highlight some glaring issues with how some people view mining. $3 per GH/s was a fair deal 4 months ago when BTC/USD was $700-800 a coin and network difficulty was under 2.5B.

As Jimmothy started to touch on, current hardware has fallen well below that mark. A BitMain AntMiner S2 (1TH/s) is being sold for BTC5.065, the equivalent of ~$2.27 per GH/s at today's exchange rate. It's predecessor, the AntMiner S1, is being sold for BTC0.439, the equivalent of ~$1.09 per GH/s at today's exchange rate, though not as energy efficient. As newer hardware is introduced and competition increases, it's expected that the price per GH/s will continue to fall.

so will PETA's cost/Gh/s go down as they increase the corresponding GH/s per share look at butterflylabs, $10.83/Gh/s cloud hosting They should, theoretically. Right now, PETA is at about $5.64 per GH/s (~7.55 GH/s per share @ BTC0.095). Assuming full deployment of 1.5PH/s, current share value ( BTC0.095) puts it at ~$1.88 per GH/s (at 66,371 outstanding shares)...but the more shares there are, the higher the 'price per GH/s' will be. Until full deployment happens, though, CoinTerra's new hosting plans range from $4.99 down to $2.75. And I'm not sure what KnC's plans are for hosting... we are currently guaranteed the 15Gh/s++ per share the current increase in shares will not have any diluting affect |

|

|

|

[...]

3$ per Gh/s is a bargain, especially with all that PETA is doing for us

This was a bit painful to read, but it does highlight some glaring issues with how some people view mining. $3 per GH/s was a fair deal 4 months ago when BTC/USD was $700-800 a coin and network difficulty was under 2.5B. As Jimmothy started to touch on, current hardware has fallen well below that mark. A BitMain AntMiner S2 (1TH/s) is being sold for BTC5.065, the equivalent of ~$2.27 per GH/s at today's exchange rate. It's predecessor, the AntMiner S1, is being sold for BTC0.439, the equivalent of ~$1.09 per GH/s at today's exchange rate, though not as energy efficient. As newer hardware is introduced and competition increases, it's expected that the price per GH/s will continue to fall. so will PETA's cost/Gh/s go down as they increase the corresponding GH/s per share look at butterflylabs, 10.83$/Gh/s cloud hosting cloudhashing best plan is 8$/Gh/s mikemikemike the two were unrelated, i dont consider someone buying contracts or shares a miner |

|

|

|

3$ per Gh/s is a bargain, especially with all that PETA is doing for us

I lol'd If you are interested in buying hardware for twice what its worth I may have a deal for you. Selling bitmain s1s for 0.9btc each. High price is only because I care about you. (Still actually cheaper than peta at double the msrp price ($2/gh)) sure you can get cheaper, thats not the point, you are getting more then just Gh/s i cant execute reinvestment's as efficiently as PETA can its actually 2.875$/Gh/s |

|

|

|

|

we have 12 days to clear the ipo, lets get going on a media campaign

im buying more shares later today once i get my BTC from cavirtex

2.875$ per Gh/s is a bargain, especially with all that PETA is doing for us

|

|

|

|

...

assume your choice is between buying hardware, a cloud contract or PETA shares

... You're overlooking a rather obvious alternative -- keeping your coin and not "investing" it at all. *But sure, all mining operations offered to the public have either lost money for the "investors," or simply stole it. See your exchange-mate, COG. you overlooked the rest of my post mikemikemike? No, simply pointed out the logical fail on which your entire post pivots. Thus far, I've been accused of being Eduardo de Castro, Mircea Popescu, crumbs, Icebreaker, and various others. Adding mikemikemike to the list. *My name is Legion: for we are many. you say no yet you still missed the body of my post mikemikemike keeping your coins leaves you with a predictable fixed return, such would not work for a stock, buy B.MINE if you truly believe in that strategy. mikemikemike, this your second slipup, your forgot to go talk to yourself in your thread with your sock-puppet accounts. |

|

|

|

...

assume your choice is between buying hardware, a cloud contract or PETA shares

... You're overlooking a rather obvious alternative -- keeping your coin and not "investing" it at all. *But sure, all mining operations offered to the public have either lost money for the "investors," or simply stole it. See your exchange-mate, COG. you overlooked the rest of my post mikemikemike? |

|

|

|

mikemikemike has allot of sock-puppet accounts

lets look at PETA from an objective point of view

their profit margin is competitive, no point arguing about what they do with it

assume your choice is between buying hardware, a cloud contract or PETA shares

since PETA does everything for you we will only discuss management of revenue from other options

the intelligent strategy with either the hardware or the cloud contract is to maximize reinvestment's of initial revenue

otherwise you are holding something that is diminishing in value and in returns

with the exponential increase in difficulty, a cloud contract or mining hardware is destined to make a fixed return, you will never make more then double what you made in the first span of difficulty doubling,

aka if you made 6BTC in 2 months, assuming diff doubling rate of 2 months, you will never make more then 12BTC in the lifetime of the hardware or mining contract

so if you instead focus on reinvesting, you can grow to a point where the asymptotic curve of returns is a significant amount in $ for a long period.

I see you posting a lot but you never have anything of substance. "...otherwise you are holding something that is diminishing in value and in returns..." After August 4, 2014 that is exactly what you are holding with Petamine. This is easily seen in CryptX's forecast in the "BTC mined 10 days" column. Numbers speak more than words, so let's see some and add some substance to your words. not in this case, numbers are pure speculation think for second, and look at what i posted, take the point of view of someone wanting to invest in mining BTC PETA is the best strategy forward |

|

|

|

|

mikemikemike has allot of sock-puppet accounts

lets look at PETA from an objective point of view

their profit margin is competitive, no point arguing about what they do with it

assume your choice is between buying hardware, a cloud contract or PETA shares

since PETA does everything for you we will only discuss management of revenue from other options

the intelligent strategy with either the hardware or the cloud contract is to maximize reinvestment's of initial revenue

otherwise you are holding something that is diminishing in value and in returns

with the exponential increase in difficulty, a cloud contract or mining hardware is destined to make a fixed return, you will never make more then double what you made in the first span of difficulty doubling,

aka if you made 6BTC in 2 months, assuming diff doubling rate of 2 months, you will never make more then 12BTC in the lifetime of the hardware or mining contract

so if you instead focus on reinvesting, you can grow to a point where the asymptotic curve of returns is a significant amount in $ for a long period. The larger your operation, the more you can take advantage of reinvestment's to secure your network share more efficiently then others.

there is nothing wrong with PETA's reinvestment plan, the loan will be paid back in 2 weeks, so dividends will not be suspended for long

|

|

|

|

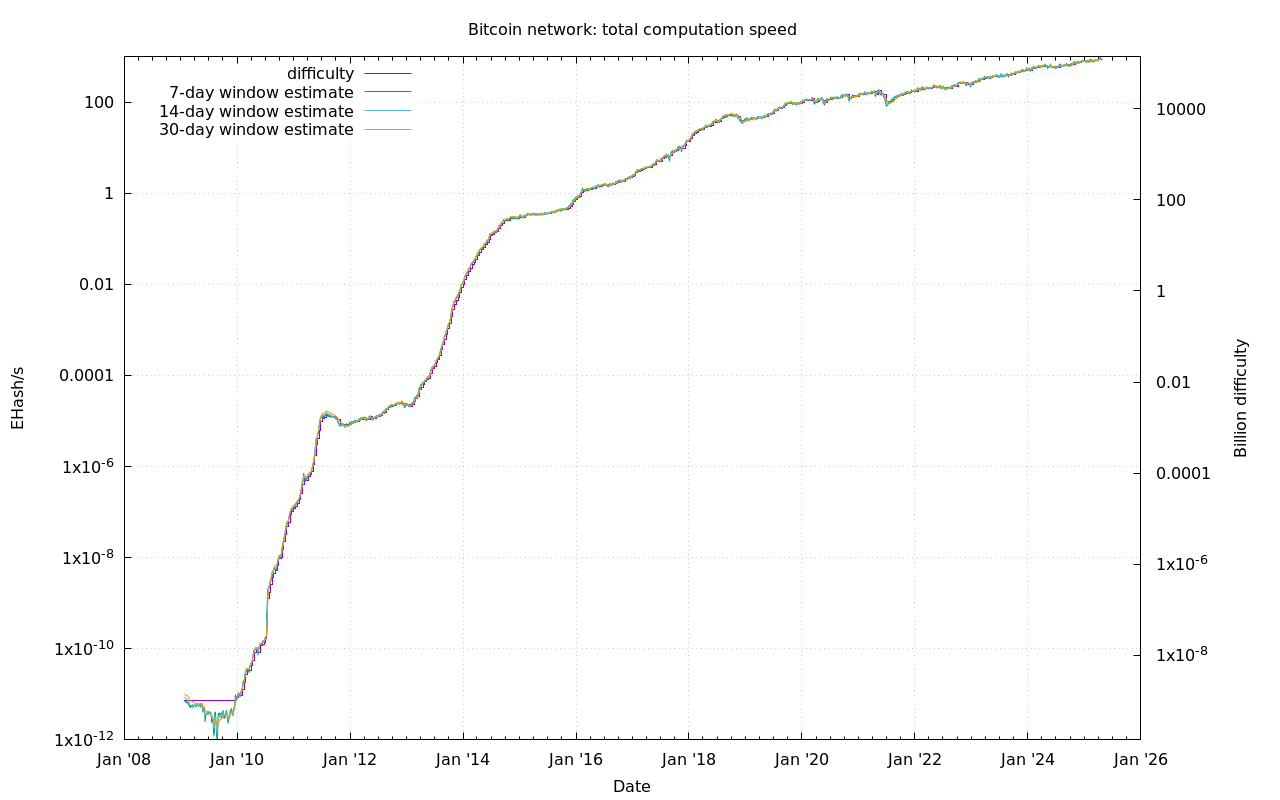

cost$/Gh/s is on an inverse trend to Difficulty there is currently not enough asic manufacturing capacity in the world to maintain the current doubling rate of the difficulty, as indicated by http://bitcoin.sipa.be/speed-ever.png$/BTC has historically kept going up, this impacts how much Gh/s each BTC buys combining these factors, PETA is setting itself up to become the most profitable investment option available with PETA current strategy, each share will continue to grow in corresponding Gh/s, giving you the most secure mining investment PETA's current profit margin is 20% of mined revenue, they have shown that they are willing to adjust their hosting fee as their operations grow, altho some who only seek short term profits may think they have acted in self-interest when they decided to grow the operation by releasing more ipo and halting dividends the case is that their action will actually benefit all investors with greater returns and better odds of successfully operating indefinitely. It was a poor decision to give petas profits through hosting fees that they determine.

I think it would have been better if they held a portion of petamine shares so at least their interests would align with their investors.

interests do align, they need to maintain and grow the hashrate network share to continue being profitable this will always benefit investors in the long run |

|

|

|

|

{kind=link}