The FED published a few weeks ago an update of their annual report:

Economic Well-Being of U.S. Households in 2022 May 2023The report is a very interesting roundup analysis of the financial well-being of US Households.

The results are not great.

Results from the 2022 Survey of Household Economics and Decisionmaking (SHED) indicate a decline in peoples financial well-being over the previous year.1 The survey, which was fielded in October 2022, found that self-reported financial well-being fell sharply and was among the lowest observed since 2016. Similarly, the share of adults who said that they spent less than their income in the month before the survey fell in 2022 from the prior year, while the share who said that their credit card debt increased rose. Among adults who were not retired, the survey also showed a decline in the share who felt that their retirement savings plan was on track, suggesting that individuals had concerns about their future financial security. The declines in financial well-being across these measures provide an indication of how families were affected by broader eco- nomic conditions in 2022, such as inflation and stock market declines.

For those of you that like the video recap, you might like the following:

There is an interesting paragraph about Cryptocurrency usage that helps us assess how much widespread the use of such instruments is in the US and a few demographic data.

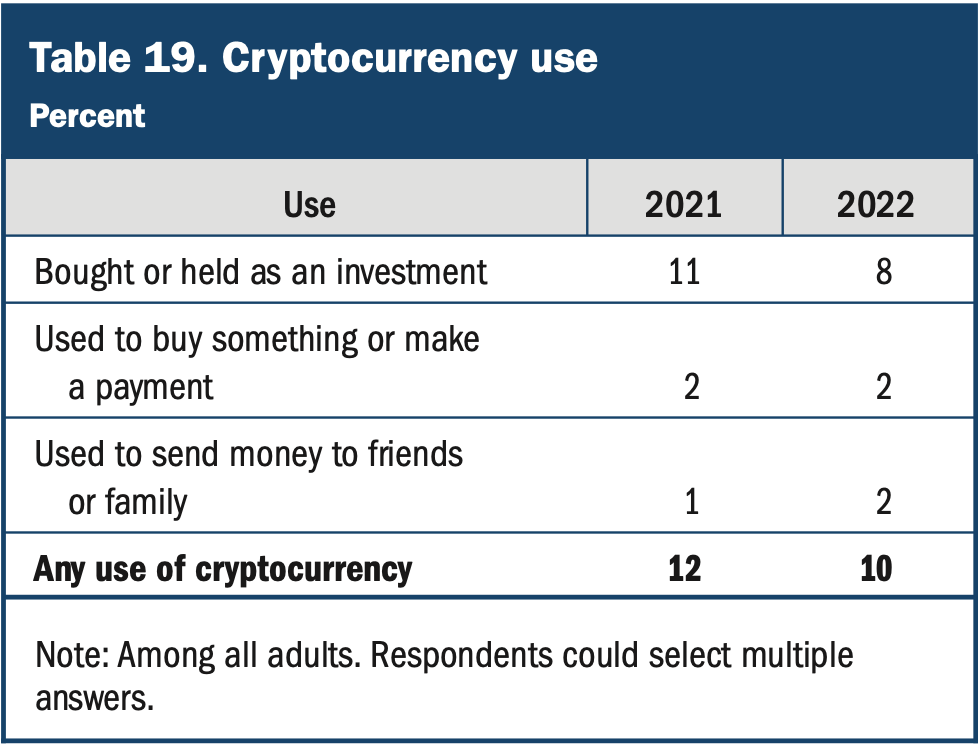

Cryptocurrency

Cryptocurrencies are relatively new digital assets that may be held as an investment or used for conducting financial transactions.31 One in ten adults held or used cryptocurrency in 2022, down 2 percentage points from 2021. This overall decline reflects a drop in the share of adults who bought or held crypto-currencies as an investment, which fell from 11 percent in 2021 to 8 percent in 2022 (table 19), potentially reflecting a response to declines in cryptocurrency asset values prior to the survey.

The share of adults using cryptocurrency for financial transactions was unchanged from 2021. It also remained less common than holding cryptocurrency as an investment.

Overall, 3 percent of adults said they used cryptocurrency to make a financial transaction in the prior 12 months: 2 percent used cryptocurrency to buy something or make a payment, and 2 percent used it to send money to friends or family (table 19).

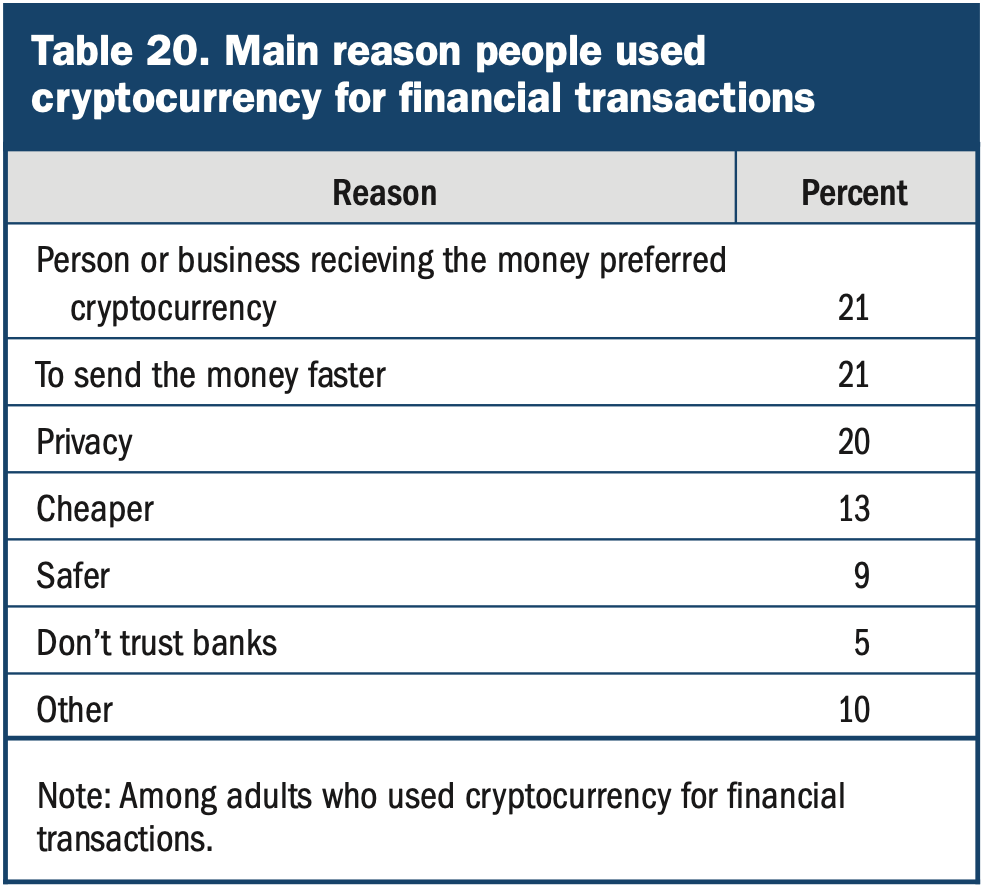

The survey asked those who used cryptocurrency to make financial transactions for the main reason they did so (table 20). The three most cited reasons for using cryptocurrencies for transactions were that the person or business receiving the money preferred cryptocurrency, to send the money faster, and privacy.

Each of these reasons was cited by about one-fifth of transactional cryptocurrency users.

|  |  |

| Cryptocurrency usage is on the dcline compared to 2021. Crypto winter is taking his toll. | There is no second best. Bitcoin is by far better money. |

Use of cryptocurrency varied by peoples willingness to take financial risks. Adults who said they were very willing to take financial risks were more likely to use cryptocurrency, either as an investment or for transactions. Just above one-fourth of those very willing to take financial risks used cryptocurrency in the prior year, compared with only 4 percent among those not at all willing to take financial risks.

Use of cryptocurrency also differed across demographic and socioeconomic characteristics (table 21). Use was more common among younger adults and men, both for investment and transactions. This was the case even after controlling for peoples self-reported willingness to take financial risks.

In contrast with age and gender, patterns by income, race, and ethnicity differed by whether the cryptocurrency was used for investment purposes or to conduct financial transactions. Adults with income of $100,000 or more were more likely than adults with lower incomes to hold cryptocurrency as an investment, whereas those with income less than $25,000 were more likely than those with higher incomes to use cryptocurrency for financial transactions. Looking across race and ethnicity shows that holding cryptocurrency as an investment was most likely among Asian adults. In contrast, use of cryptocurrency for financial transactions was more common among Black and Hispanic adults than White or Asian adults.

One in ten adults held or used cryptocurrency in 2022, down 2 percentage points from 2021.

Use of cryptocurrency for financial transactions was more common among the unbanked, as well as those who used nonbank check cashing and money orders. Five percent of unbanked adults used cryptocurrency for financial transactions, compared with 3 percent among banked adults. Regardless of bank account ownership, those who used nonbank check cashing or money orders had a greater propensity to use cryptocurrency for transactions8 percent among those who used nonbank check cashing or money orders compared with 2 percent among those who did not. That said, use of cryptocurrency for financial transactions remained very low, even among groups who were more likely to use cryptocurrency in this way.

|  | |

| Cryptocurrency grows with the Family Income as a investment only asset class, the opposite happens with transaction use. | |

Previous years SHED reports can be found

here: