fillippone (OP)

Legendary

Offline Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 02, 2020, 09:59:37 PM

Last edit: May 16, 2023, 06:52:37 AM by fillippone Merited by Micio (30), LoyceV (15), babo (13), arulbero (10), Paolo.Demidov (7), hugeblack (6), duesoldi (5), LUCKMCFLY (5), exstasie (5), DdmrDdmr (4), vapourminer (3), The Sceptical Chymist (3), Heisenberg_Hunter (3), pugman (2), zasad@ (2), VB1001 (2), d5000 (1), JayJuanGee (1), Gyrsur (1), seleme (1), mk4 (1), Saint-loup (1), hosseinimr93 (1), TheBeardedBaby (1), 1Referee (1), bitserve (1), Rikafip (1), famososMuertos (1), Last of the V8s (1), psycodad (1), Poker Player (1), HBKMusiK (1), Krastavac (1) |

|

Options on bitcoin have been accessible only to whales and on very specific exchanges as Deribit, but when Bakkt and CME, the two main traditional bitcoin exchanges will open the products to their clients option trading in bitcoin will become more widely accessible. Actually, options trading has been available on Bakkt since December 9th, while CME will launch a similar product later this month, starting trading from January 13th. Options are a difficult instrument to trade. This is true in traditional markets, but this is even more true in a wild market like bitcoin. With this thread, I will try to give a few theoretical and practical hints on how to understand, price and use options. I will start detailing what an option is, explaining all the characteristics of the options and what they mean for the investor. Then I will briefly explain how to price them. I won’t explain the details of the mathematical model used to price those, because it would imply some advanced differential calculus nobody wants to hear about. What I will try to do is to convey what factors have an impact on option price and how to interpret those. I will also try to clear the field from some common misconceptions about options. Last I will explain a few common strategies for options trading. Nothing too complicated, just a few examples on how to use them according to investment purpose: be it speculation or hedging.

INDEX

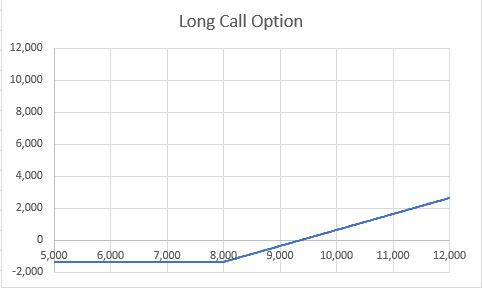

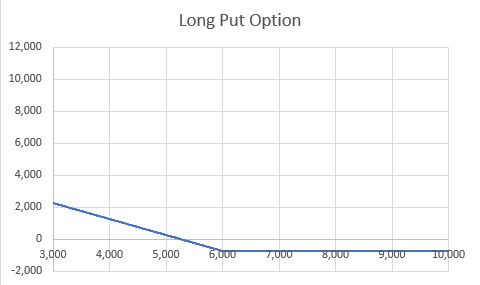

What is an optionAn option is a contract that gives the holder the faculty, but not the obligation, to trade an asset, called the underlying asset, before the expiry, the termination date of such contract. The option that gives the holder the faculty to buy the underlying asset is called call option. The option that gives the holder the faculty to sell the underlying asset is is called a put option. The price at the trade will happen is called the strike price. When an option generates a trade then we say it is "exercised", otherwise it simply ends without any trade put in place we say it is "abandoned". If an option can be exercised only at the termination is called European Option, while if it can be exercised anytime before the termination is called American Option. The price the buyer of the option pays to the seller, or the writer of the option, is called the premium. If the market price is above the strike price, the call option is called "in-the-money", because in the case of American exercise it could be exercised with profit. Otherwise, the call option is called "out-of the-money". If the market price is below the strike of the put option, the put option is called "in-the-money", because in the case of American exercise it could be exercised with profit. Otherwise, the put option is called "out-of-the-money". If we look at a certain strike then, only call options or put option can be in-the-money, not both of them. For example, if we look at 10,000 strike options, the calls are now out-of-the-money, while puts are in-the-money. At expiry, if the option can generate the underlying asset what has been priced is called “physical delivery”. Many commodity or financial options are physically settled. Alternatively, an option can regulate only the cash equivalent of the profit exercising the option itself: that expiry then an in-the-money option would deliver the buyer a cash amount equal to the difference between the asset price and the strike (in case of a call option) or the difference between the strike price and the asset (in case of a put option). In this case, the option is called cash-settled. In the case of Bitcoin options, namely the Bakkt options on BTC futures, the option is physically settled: at the expiry of the option the in-the-money option generates an appropriate position in the underlying future. There’s only a peculiarity: as it is common on many commodity options, the option itself expires a few days before the future, so the holder of the in-the-money options has the possibility to close the future position before the actual delivery of the underlying of the future (the option has the future as underlying, the future has the bitcoin as underlying). This is why you probably heard some marketing nonsense where “Bakkt options allow you to choose the type of delivery: physical or cash)". Before analysing mathematically how to price an option, let’s see that impact the pricing with the intuition. STRIKE: The first element is the strike. Of course, the difference between the market price and the strike is the first hint at the value of an option. Intuitively the more an option is in-the-money, then the more such an option must have value. When an option is in-the-money, such an option has intrinsic value. For both call and put options, the intrinsic value is equal to the difference between the underlying price and the strike price: intrinsic value only measures the profit as determined by the difference between the option's strike price and market price. When an option is out-of-the money instead, the intrinsic value is zero. The intrinsic value is the minimum value of an option: if the value of an option would be less than the intrinsic value, could be arbitraged, buying that option and exercising it to profit. So when BTC is trading at 7,000, a call with strike K = 5,000 is in-the-money and has an intrinsic value of 2,000, so the price must be greater than that. At the same time, a call with a strike K =10,000 has no intrinsic value, so the intrinsic value is zero. Of course, intrinsic value is only a part of the pricing of an option: other variables impact the option pricing each one of them adding value to the intrinsic value getting the final value of the options: TIME TO EXPIRY: the second most important element when pricing an option is the time to expiry: the longer the time to expiry, the dearer the option. If we price two options with all characteristics being equal, but the exercise date, the one with the exercise date the furthest away, will have the greater price. VOLATILITY: the greater the volatility of the underlying asset, the greater the value of the option. Here the explanation gets a little bit tricky. Let’s say that the main reason it is not the greater the volatility of the underlying, the greater the possibility of the underlying going in-the-money. We will see later why this is important, just take in mind that is not obvious. The option buyer doesn’t profit from the option going in-the-money. Rather don’t profit only if the option goes in-the-money. The buyer of the option benefits just because the underlying asset moves (i.e. it is volatile) under a risk-neutral approach, i.e. without taking the “risk” of profiting because the option goes in-the-money. Let's see an example: We buy a call option on BTCUSD, with a strike price of 8,000 USD, expiring in June 2020. The strategy is named Long call because buying something is called being " long" in finance jargon. The premium for this option is 1,350 USD, we have to pay immediately (" upfront", again in finance jargon). Fast forward to option expiry. The outcomes of our option differ according to the final price of bitcoin: If BTCUSD is below 8,000 USD the option is abandoned, it expires worthless. If BTCUSD is above 8,000 USD the option is exercised, and generate a payoff equal to the difference (positive) between BTCUSD and the strike price. In more formal terms the call option payoff is the following: Call=max(0;Spot-Strike) The final payoff of the strategy will be the following:  Note that this graph considers we paid a premium of 1,350 USD upfront, the premium must be paid in every scenario: if the option expires worthless the P&L (Profit&Loss) of the strategy is negative and equal to the premium paid, otherwise is equal to the option payoff netted with the premium paid. Note that the P&L starts increasing at the strike price level, 8,000 USD in this case, but breaks even at a higher level equal to the strike + the premium plaid, or 9,350 USD in this example. Let's see the same thing for a put option. We buy a put option on BTCUSD, with a strike price of 6,000 USD, expiring in June 2020. The strategy is named long put. The premium for this option is 732 USD, we have to pay " upfront". Fast forward to option expiry. The outcomes of our option differ according to the final price of bitcoin: If BTCUSD is above 6,000 USD the option is abandoned, it expires worthless. If BTCUSD is below 6,000 USD the option is exercised, and generate a payoff equal to the difference (positive) between the strike price and the BTCUSD. In more formal terms the put option payoff is the following: Put=max(0;Strike-Spot) The final payoff of the strategy will be the following:  The graph looks familiar, as it is the symmetrical payoff than the call. Note that this graph considers we paid a premium of 732 USD upfront, the premium must be paid in every scenario: if the option expires worthless the P&L of the strategy is negative and equal to the premium paid, otherwise is equal to the option payoff netted with the premium paid. Note that the P&L starts increasing at the strike price level, 6,000 USD in this case, but breaks even at a lower-level equal to the strike - the premium plaid, or 5,267 USD in this example.

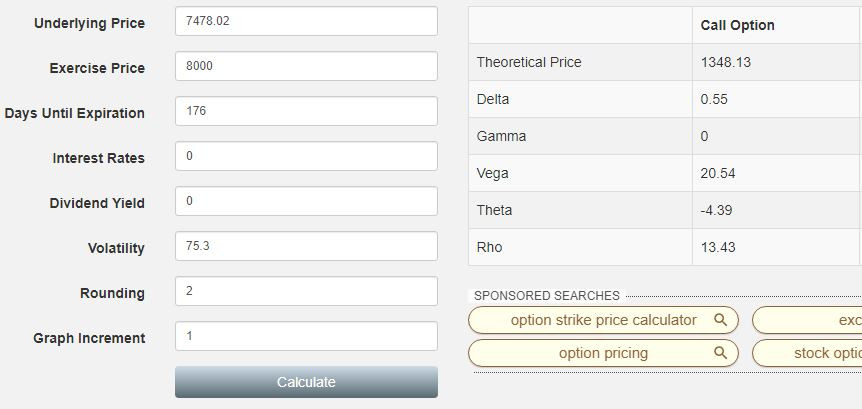

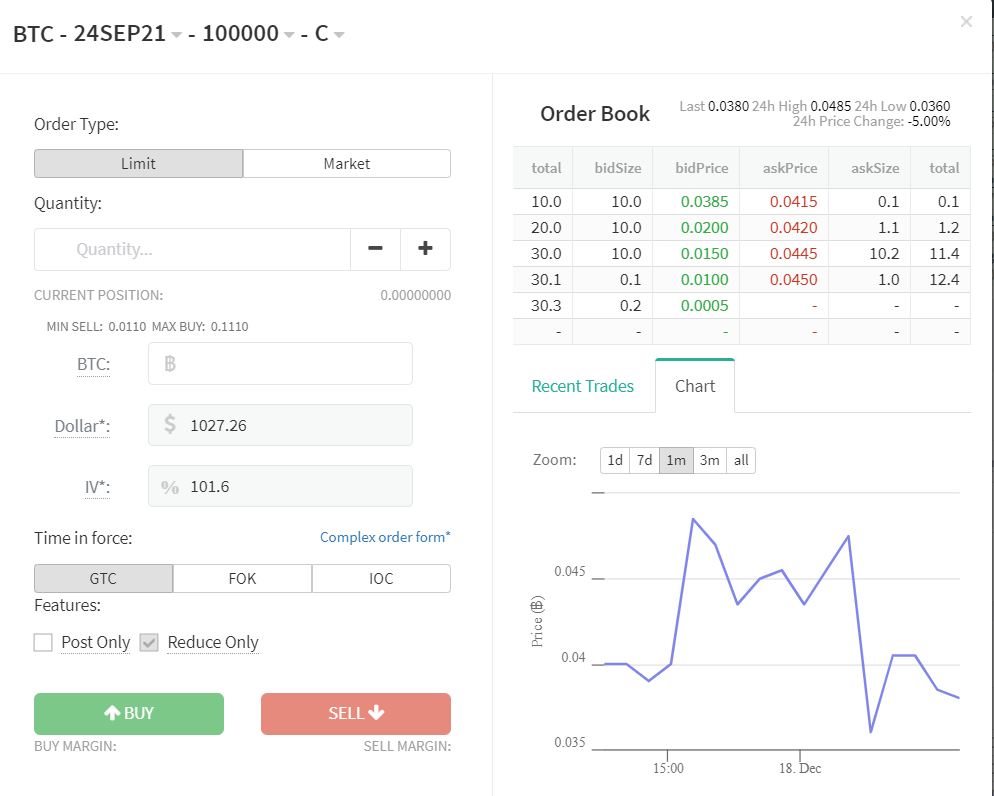

Let’s have a look at an options exchange looking for confirmations. All the examples are from Deribit, who is the only widely available source for option prices: creating an account is easy and don’t require KYC. If you are interested to do it for educational purposes. Of course standard disclaimers apply and I am not by any mean linked to that exchange. If we select BTC options, and then 26 Jun 2020 we will find a screen like the following:  (click on the image to enlarge it) (click on the image to enlarge it)This particular page considers the options maturing on 26 Jun 2020. The centre grey column represents the strike levels. The options on the same row share the same strike price. On the left of that column, we have the call options for each strike, while the puts are on the right-hand side. The bid price is the price where other participants want to buy the options, i.e. the price you have to sell at if you want to sell it. The ask price is the price where other participants want to sell the options, i.e. the price you have to pay for if you want to buy it. Each bid and ask price has a corresponding Implied Volatility level, that is the volatility level that, if inputted in the model, gives back the aforementioned price. This is why speaking of options, volatility and price are exchangeable concepts. As we saw earlier, we see that the calls have a diminishing price when the strike goes up: the 6,000 call has a mid-price (the average between the bid and the ask) of 0.29725 BTC, while the 10,000 call has a mid-price of 0.11275 BTC. The opposite is true for the puts. The puts with lower strike have lower premiums. The put stuck at 10,000 has a price of 0.46075 BTC, while the 6,000 put has a mid-price of 0.09725 BTC. Also, we can see that examining options with greater time to expiry each option has a greater value: the 10,000 USD strike call maturing in September has a value of 0.16775 BTC versus the value of 0.11275 of the same option maturing in June. The 6,000 strike put has a value of 0.13175 BTC versus the value of 0.09725 of the same option maturing in June. If we plug the data we find on that page in an options calculator we can reprice the option itself. If we try to reprice the 8,000 USD call, inputting 0% as the interest rate (BTC is a non-dividend paying asset) and the correct information about strike, underlying and implied volatility, we get the (almost) exact valuation we have on Deribit:  The numbers below the option price are the "greeks" or the sensitivities of the option price to their various component: DELTA: it's the sensitivity of the option price to the underlying: if the underlying goes up 1 USD, the option price goes up 0.55 USD. GAMMA: it's the second-order sensitivity of the option price to the underlying: if the underlying goes up 1 USD, the option delta goes up 0% (I guess there's a rounding factor here to consider in this calculator) VEGA: it's the sensitivity of the option price to the volatility level: if the volatility goes up 1%, the option price goes up 20.54 USD. THETA: it's the sensitivity of the option price to the time: if 1 day passes, the option price goes down 4.39 USD. RHO: it's the sensitivity of the option price to the interest rates: if interest rates go to 1%, the option price goes up 13.49 USD. The greeks of an option are linked to each other in a pretty complicated way, there are many ways to interpret them and they all varies continuously given the level of the market, the volatility and the time to maturity. Books have been written on how to tame them and use them in your favour. I think this very brief explanation is enough for this thread.

How to price an optionUnderstanding the details of how options are priced, would mean understanding very advanced mathematics, including stochastic calculus, differential calculus, statistics, etc. Here I want only to give you a few important concepts, you have to keep in mind when thinking of options and their value. Black&Scholes won the Nobel prize for their option pricing model. Their biggest achievement was to demonstrate it is possible to price an option using non-arbitrage conditions. Arbitrage is a trade where a profit is gained involving no risk and no capital. Of course, those trades do not exist, so markets will adapt themselves to avoid these situations. Reasoning under the “non-arbitrage” conditions, means also that no risks are involved, hence the individual appetite for risk of each different trader in the market can be taken out of the equation. This means that every trader in the market will reason using the same “language” of a world without risk (if we reason with no-arbitrage conditions, we can ignore the associated risk, then we can ignore the willingness of every trader to take that risk). This means the price of such a derivative is unique, irrespective of the risk appetite for each trader. This has the important consequence the price of an option is INDEPENDENT of the probability given by each trader about the possibility of the underlying ending in-the-money. This is something we have to keep in mind: the price of an option doesn’t mean automatically that the scenario where it ends in-the-money is more “plausible”. Historical Volatility vs Implied Volatility As we can see the only “difficult” input to price an option is the volatility to be used. The correct number to be plugged into the pricer is the expected future realised volatility until the expiration of the option. Quoting this number means quoting the price of the option (being the other option pricing numbers deterministic, i.e. known without uncertainty). The volatility level used to price an option is called implied volatility because it’s the level of volatility “implied” by the quoted price. How do you quote the future volatility? Here’s the trick of options trading. The first idea is to look at the realised volatility: looking at the past can give first guidance of the future volatility. Of course, this is not always true as there can be many factors that can change the volatility in the future. One easy example, specific to bitcoin options could be the halving. This event, according to many models, could have a great impact on the bitcoin price. So we can guess that coming into the halving the volatility will be low: bitcoin might move, but without great variations, but once the halving happens, the price will possibly start swinging more, due to the very different valuation the S2F model implies. In this case realised volatility won’t be good guidance for the future volatility: namely the realised volatility will be much lower than the future volatility used to price options with expiries after the halving. Many websites calculate the realised volatility of bitcoin: on Deribit you can get one. Calculating historical volatility with different horizons yield very different results:  In the above graph, we see the bitcoin price (black line, left axis), with the superimposition of different historical volatility calculations using different terms (yellow, red and blue lines, right axis). Volatility in the short term can be more “volatile” itself (yes, there is the volatility of volatility, but this is for advanced options trading). The yellow line represents the annualised historical volatility calculated using the previous 10 trading days, and as we see in the above graph is swinging more violently, from 180% to below 20%. Volatility calculated over more extended periods of time, like the blue line (calculated over the last 30 days of data) or the red line (calculated over the last 180 days of data) is instead more and more stable as we extend the calculation interval. Of course, we are more interested in matching, with the caveat earlier explained, the historical volatility computation with the time to expiry of the option we want to price. The implied volatility can instead be observed on options markets. If we look at the options screen above we see some IV columns: that is the implied volatility corresponding to each quote. If we use the model in the opposite way, we can use the price as an input and find the volatility implied into that price: that is the implied volatility.

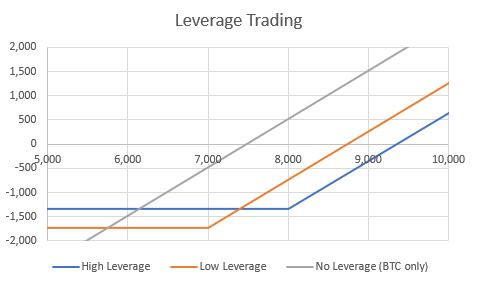

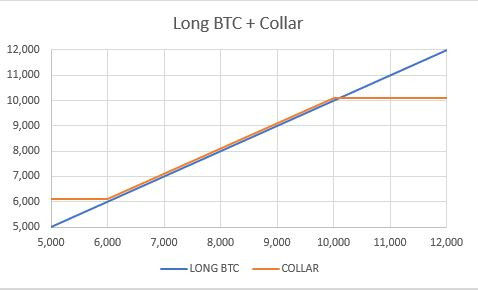

Option strategies - How to use an optionOptions are very complicated instruments, here I want to highlight only a few uses of them. These are the most simple ones, and all have in common to be “static” strategies. This means those are meant to be put in place and not touched until maturity. There are different strategies meant to be adjusted during the life of the option. These are totally different animals and they are called dynamic strategies. Leverage TradingScenario: You want to gain as much possible exposure to bitcoin. You have a very clear trading view. You are not interested in losing your capital if this view doesn’t materialise. Strategy: Use your funding to pay the premium for an out-of-the-money option, choosing the strike to maximise the expected final payout. Example: - Buy 1 call option strike 7,000 USD, Jun Expiry at 0.233 BTC. alternatively - Buy 1 call option strike 8,000 USD, Jun Expiry for a total of 0.1805 BTC.  Analysis: In this scenario, you have gained exposure to the appreciation of bitcoin above the strike level using only a fraction of the capital required to buy the underlying (i.e. 1 bitcoin). In the case of bitcoin being at a price of 10,000 at expiry, in the case of a bitcoin investment, you would have a return equal to (10,000-8,000)/8,000=25%. This is the base case scenario of no leverage. Buying an in-the-money call option the return would be instead (10,000-7,000-1,742)/1,742=72%. Note that if the option gets further in-the-money the return goes up even further as the option paid is constant, while the gain increase linearly. In the second example, we bought an out-of-the-money option, using even less capital. In the case of bitcoin being at a price of 10,000 at expiry, the yield would be in this case (10,000-8,000-1,350)/1,350=48%. Of course in the scenario of an opposite movement, your loss is limited to the premium paid, which would be lost entirely. This implies that you have to choose wisely not only the strike level, to gain the correct level of exposure, but also the expiry, as the movement has to materialise Before the expiry of the option. Covered call writingScenario: You are a whale you want to sell part of your bitcoin holding to finance your daily expenses. You are bullish on bitcoin as an investment. Strategy: Sell out-of-the-money calls, cash in the premium to finance your expenses, actually sell bitcoin only if the price goes up (possibly on a spike). Example: - long 1 bitcoin, - sell 1 option strike 10,000 USD, Jun Expiry at 0.11 bitcoin.  Analysis: The payoff of the structure gives you a benefit over the simple holding of bitcoin equal to the premium if the price is below the strike price at maturity. If at expiry the price is above the strike, the option goes in-the-money and you sell the bitcoin. The strategy has a break-even, compared to being long the BTC only, at a level equal to strike + premium received (in this example at 10,000+0.11*7,478=10,826 roughly). If the BTC goes further up, you basically sold a bitcoin at 10,826, hence the strategy has a lower value against holding the bitcoin. CollarScenario: You are a whale. You want to sell part of your bitcoin holding to finance your daily expenses. You are bullish on bitcoin as an investment. You get pissed off in case of a violent drawdown in bitcoin prices. Strategy: Sell out-of-the-money calls, cash in the premium to finance your expenses, actually sell bitcoin only if the price goes up (possibly on a spike). Use the cashed-in premium to buy protection on the downside, i.e. buying a put option. Buying an out-of-the-money call and selling an out-of-the-money put is a strategy known as "Collar". Example: - long 1 bitcoin, - sell 1 call option, strike 10,000 USD, Jun Expiry at 0.11 BTC, - buy 1 put option, strike 6,000 USD, Jun Expiry for 0.098 BTC.  Analysis: The final payoff is similar to the one of the covered call writing. The payoff of the structure gives you a benefit over the simple holding of bitcoin equal to the difference between the premiums paid to buy the put and the premium cashed in to sell the call. In this particular case, I chose two strike levels to have the smallest positive difference between the twos. If the price is below the strike price at maturity. If at expiry the price is above the strike, the option goes in-the-money and you sell the bitcoin. The strategy has a break-even, compared to being long underlying, at a level equal to strike+premium received (in this example at 10,000+(0.11-0.098)*7478=10,093 roughly). If the BTC goes further up, you basically sold a bitcoin at 10,093. On the contrary, if BTC goes down, you also bought protection at 6,000, as you are long a 6,000 put. More precisely, as you cashed in a premium of 93 dollars, you are protected at a 6,093 USD. In case bitcoin goes down more, you are not affected, as the payoff of the put protects you on the downside.

Word of caution. Options are a very complicated topic. I tried my best effort to explain this topic in the most simple and intuitive way. I can expand the thread in the direction you prefer. Just ask me to explain what you are interested in most, or just ask me to clarify the point you want me to dig more precisely.

If you think this thread or any other of my threads is worth being translated in your own local board, please do! I will be happy to provide assistance!

Useful resources: Online Calculators: Option CalculatorExchanges product information: Option on Bakkt ™ Bitcoin (USD) Monthly FuturesOptions on Bitcoin FuturesOnline courses: Basic: CME Option CourseAdvanced: Options Theory for Professional Trading

This post is eligible for my project: I am a strong believer in the utility of local boards.

I am lucky enough to be able to express myself in at least a couple of languages, but I know this is not the case for everyone.

A lot of users post only on the local boards because of a variety of reasons either language or cultural barriers, lack of interest or whatever other reason.

I personally know a lot of very good users (from the Italian sections mainly, for obvious reason) who doesn't post in the international sections.

I think all those users are missing a lot of good contents posted on the international (English) section or on other boards. If you think you can help here, just visit the thread! |

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

|

|

|

Even if you use Bitcoin through Tor, the way transactions are handled by the network makes anonymity difficult to achieve. Do not expect your transactions to be anonymous unless you really know what you're doing.

|

|

|

Advertised sites are not endorsed by the Bitcoin Forum. They may be unsafe, untrustworthy, or illegal in your jurisdiction.

|

|

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 03, 2020, 01:58:14 PM

Last edit: May 16, 2023, 06:52:17 AM by fillippone |

|

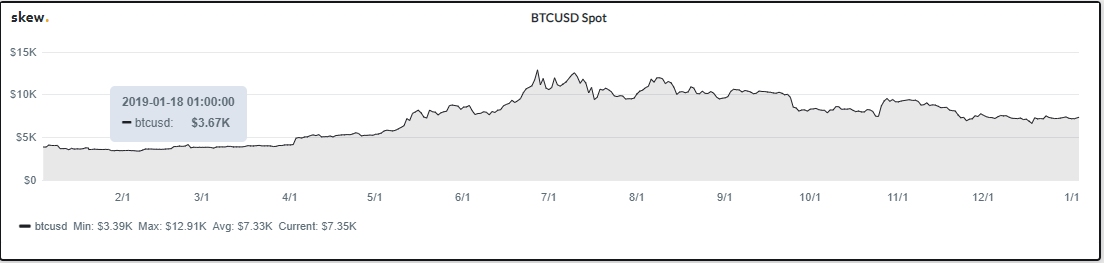

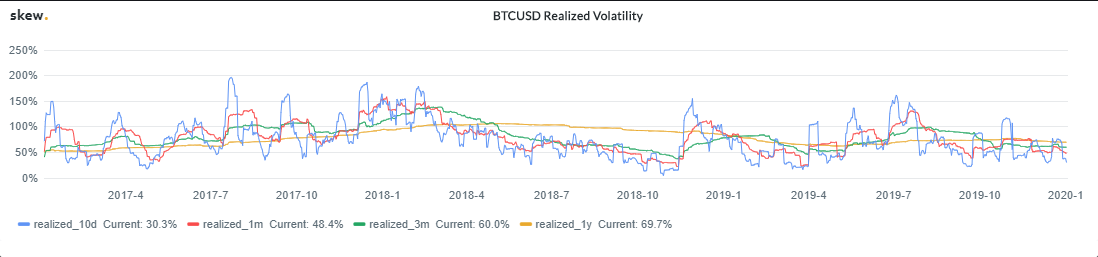

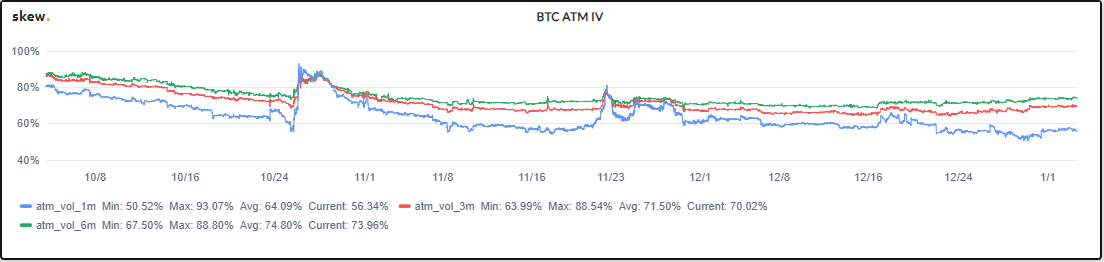

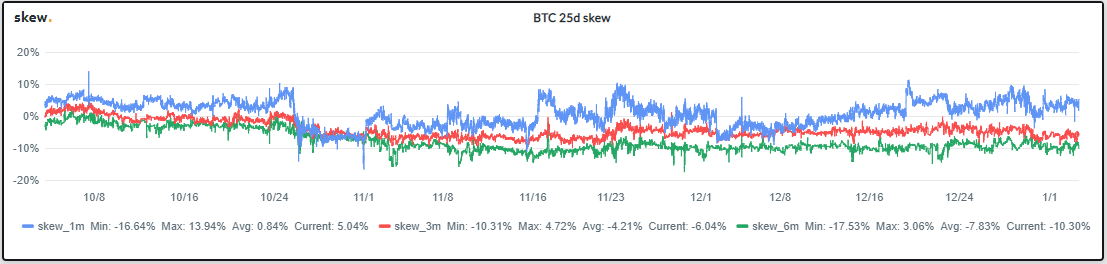

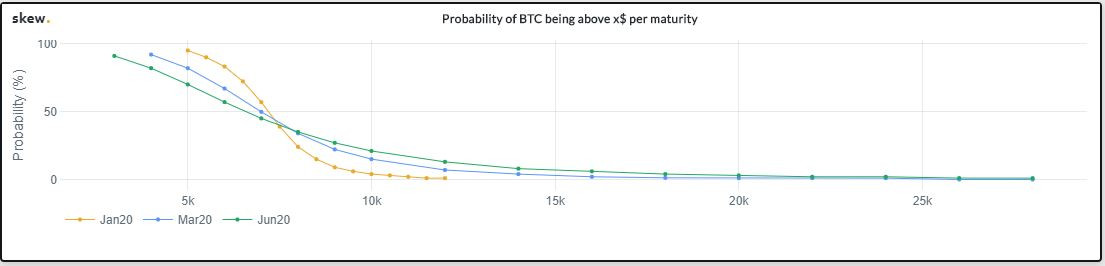

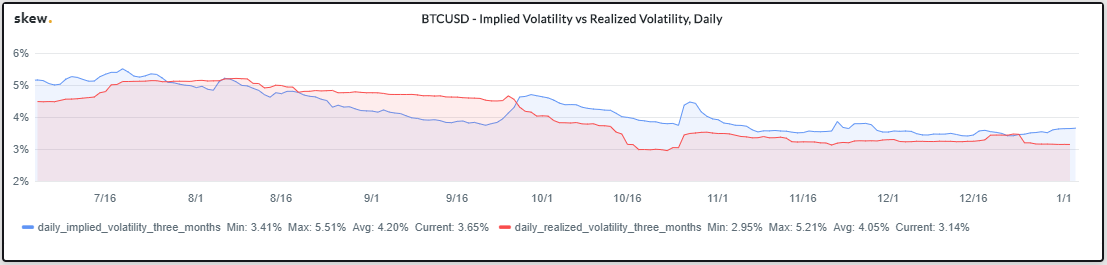

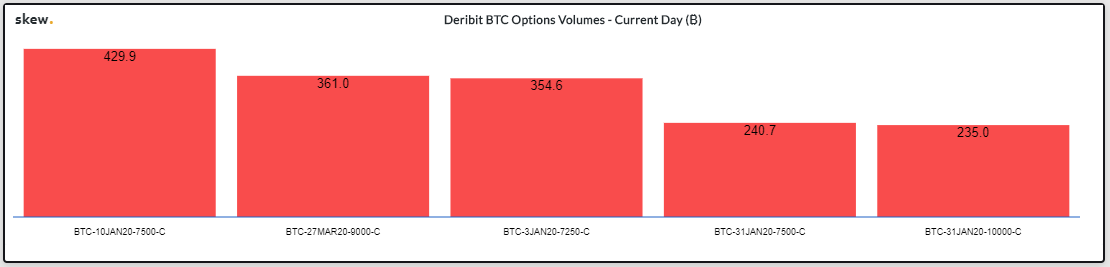

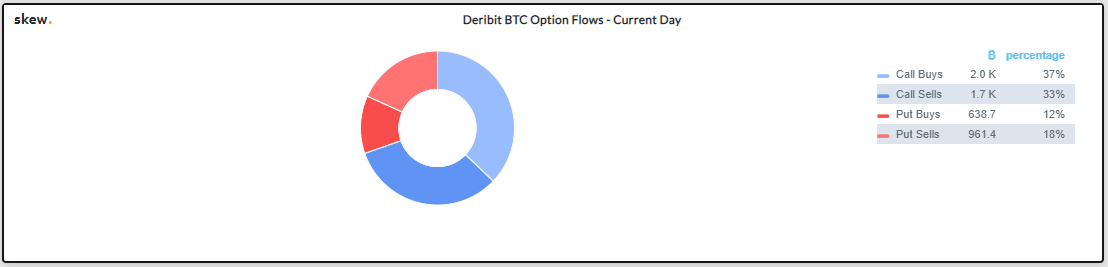

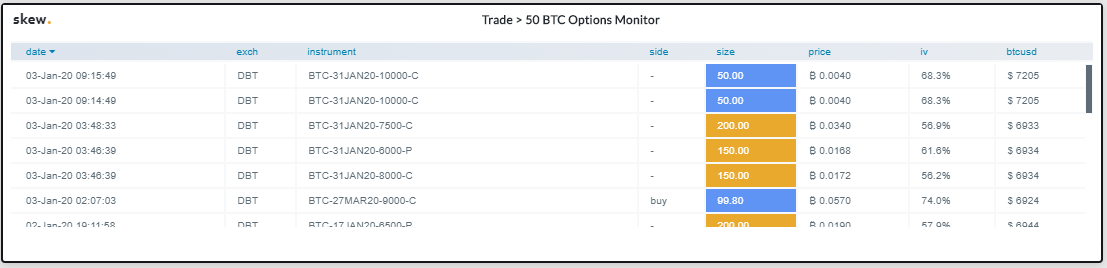

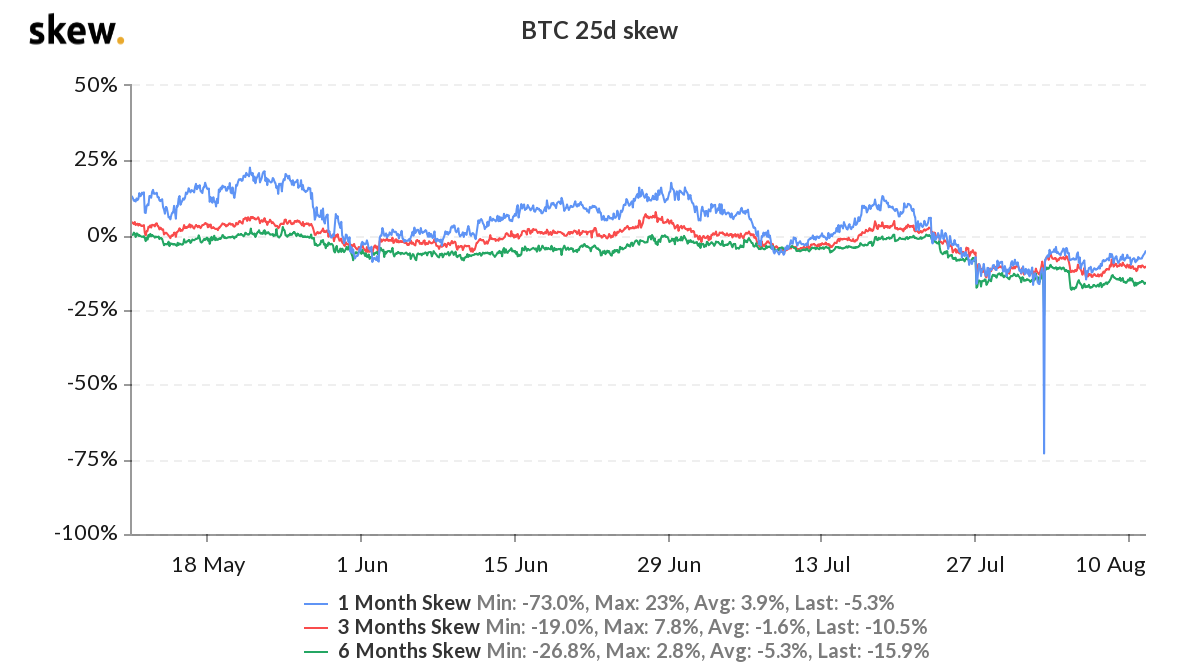

A nice tool to monitor the options market is the dashboard provided by skew.com: Bitcoin Options Dashboard by SkewI will try to explain how to interpret the various graphs. BTCUSD Spot Nothing to see here, a simple graph on a linear scale. Pretty Standard, just to orient ourself checking the other graphs. BTCUSD Realised Volatility We already saw this graph in the OP: this is the historical bitcoin volatility, computed using different time horison. We already noticed the realised volatility observed over longer periods tends to be more stable. BTC Options Volumes In this graphs we see the trading volumes of all options on the different exchanges. We see the vast majority of options has traded on Deribit. I think this is going to change with the launch of the two biggest exchanges BAKKT and CME. Bakkt has actually already launched, but it is barely noticeable. We already noticed Bakkt is a slow starter, but when he got his product rolling, they were slowly grinding volumes. BTC ATM IV This graphs is similar to the historical volatility one, but instead focus on the Implied Volatility. They compute the implied volatility of an at-the-money option (strike price euqalt to forward price of bitcoin) expiring at various tenors: 1m, 3m and 6 months in the future. So this represent the future expected volatility of bitcoin over such horizons. We notice that implied volatility is moving more for shorter term options, and its more stable for longer tenor options. BTC 25d Skew This charts start giving out very technical infromations. This measures the difference in implied volatility terms between two options maturing on the same date. The lines measure the difference in implied volatilites between an out of the money call and an out of the money puts. Both options are chosen with a strike having 25% delta (hence the 25d in the chart title). So the strikes are not fixed in dollar terms, but in "moneyness" or "distance" from the current market levels, so the measure is consinstent over the various market phases. A positive number means call Implied volatility is higher than the put volatility, this means volatility is expected to rise in an upward movement (probably more people wants to buy upside options because want to leverage the price of bitcoin. BTC ATM Volatility Structure This is the level of implied volatility of the options expiring at the various dates expressed below. This gives a similar information as the BTC ATM IV graphs (and informations are actually consistent), losing the historical part , but giving more informations on the expiries, axpressed as fixed dates r(probably expiries dates at the various exchanfges) rathr than "rolling dates (1m, 3m and 6m). Probability of BTC being above x$ per Maturity This is a tricky one. I don't knwo the details of the calculation of this graph, but I think it is greately misleading. The shape of the graphs looks very like the delta of an option with a given strike. Delta of an option can be tought as the risk-neutral probability of an option of being in the money. Well, the kew is that one: risk neutral probability are very different from real world probability. So, O dosmiss this graph as "manure". Please don't draw conclusion from that particular piece of information. BTCUSD - Implied Volatility vs Realised Volatility, Daily This is a very intresting graphs. It combines the realised volatility with the implied volatility over the same horizon: so this graph answers the following quiestiins: "Which level of volatility are markets pricing in, compared to the one they observed in the past?". The graph plots the volatilites over a 3m horison: currently the Implied volatility is pricing above the realised: market are currently expecting volatility to go up on the next months (probably due to the halving event in 5 months). Deribit BTC Options Volumes Pretty straightforard graph. This is the volume of traded options today on deribit. Please not that this is the notional of the options, not the sum of the premium paid. Deribit BTC Options Flows This graph details if the sign of the flow, buy or sell, and the type of option call or put. Of course for every trade there is a buyer and a seller, but when a trade happens on the ask side of the price it's conventionally clasified as a "buy", while when a trade happens on the bid side ofthe market it's called a "sell". We see that the majority of trades are on the call side (this is actually intresting) without much imbalance between buy and sell, so a nice, liquid two ways market. Trade >50 BTC Option Monitor This graph is actually a blotter of the trades that happened on the exchange. Most relevant trades are highlighted. Can give a sense of how the big swinging dicks are trading, but it is always very difficult to extract meaningful information from those blotter without having a complete view of the position under management (i.e. buying 500 BTC put as leverage trading, is vert different buying 500 BTC put becasue you are also long 1000 BTC and you want to protect from the downside). Deribit BTC Option Call/Put Ratio Put Call Ratio is the ratio of the trades on Calls versus the trades on the Put. Again, it's a graph very common amonsgt traders, but with limited or very diffciult information value, in my humble opinion. |

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 03, 2020, 05:28:12 PM

Last edit: May 16, 2023, 06:50:46 AM by fillippone |

|

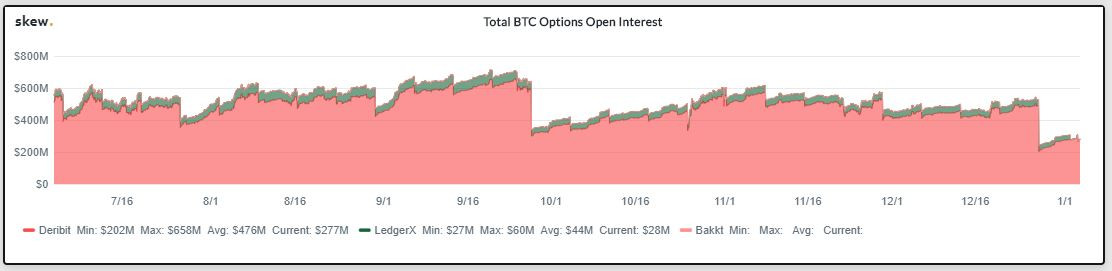

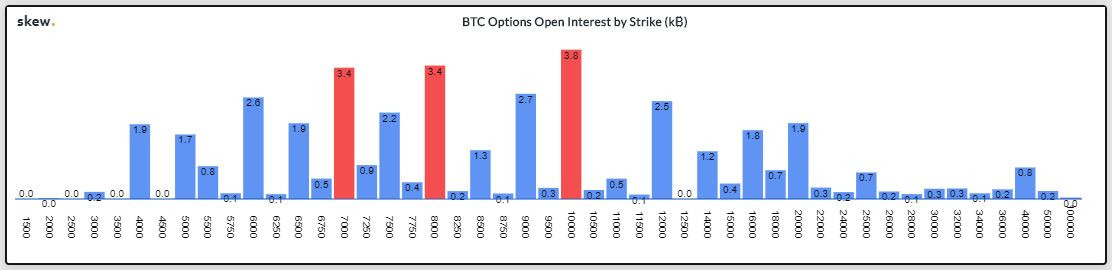

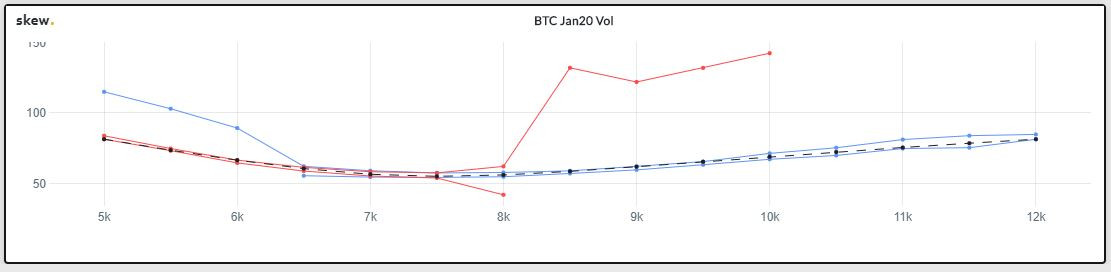

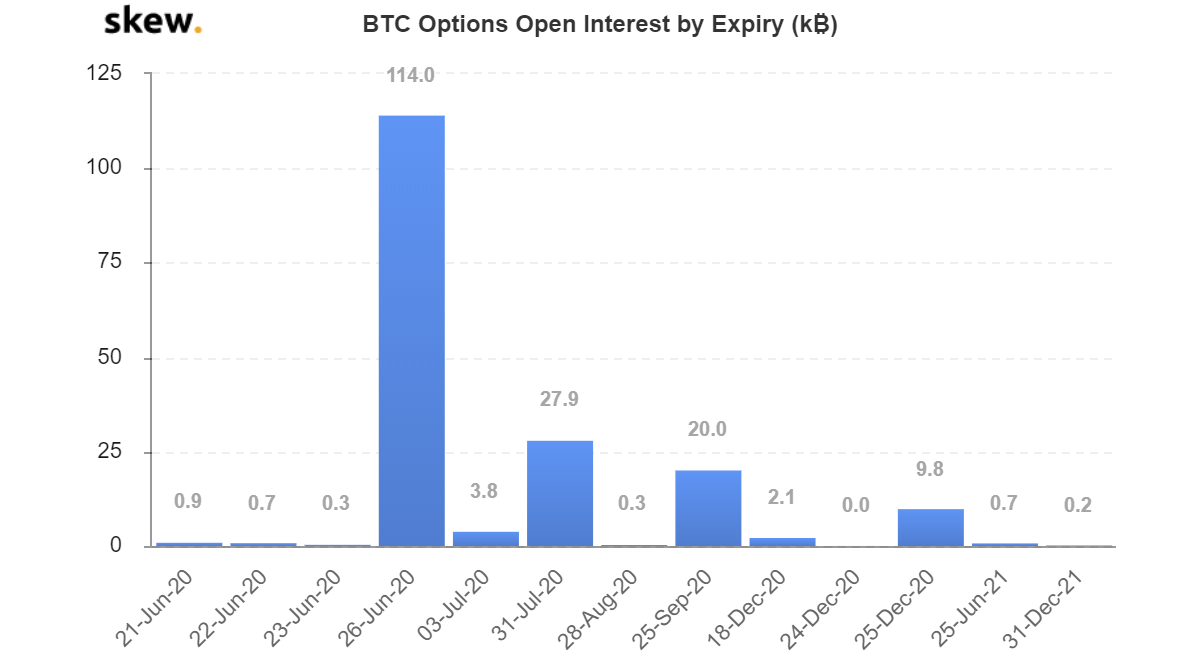

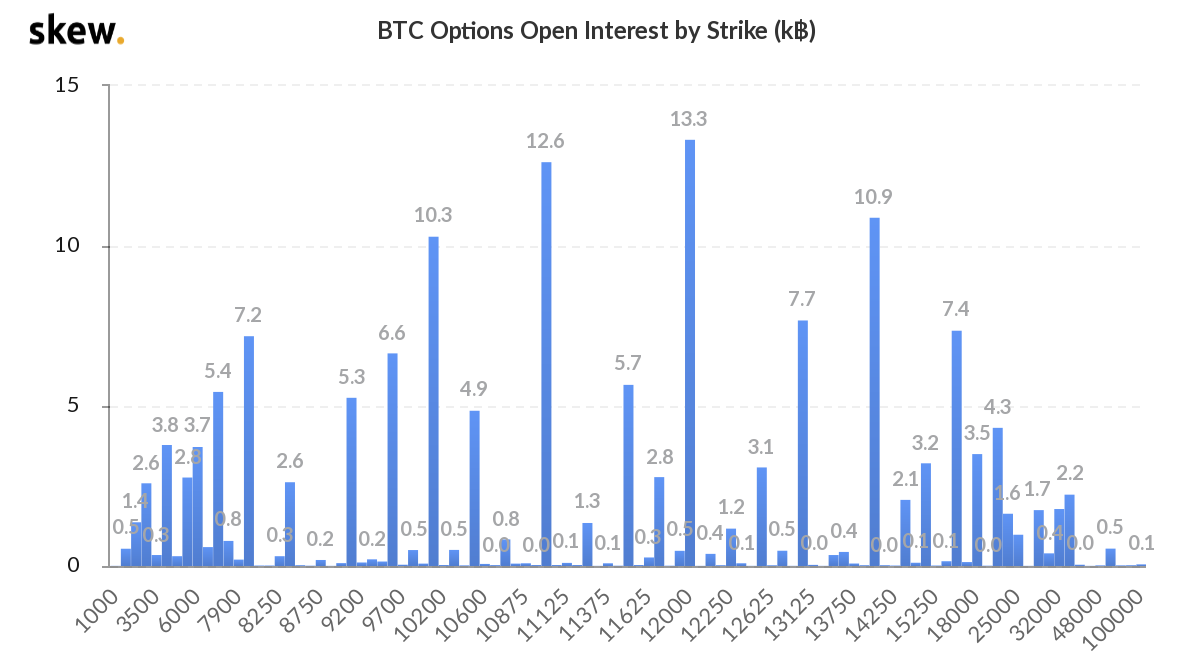

Deribit BTC Options Buy/sell Ratio This graphs details if the trades happened on the buy side (asks lifted) or on the sell side (bids given). Again, it's difficult to understand the final positioning looking only at this kind of graph, but a shift in the current state of ratio can signal a shift in general sentiment. Of course, buys and sells should add to 100%. This is not the case in this graph I have no idea why, sometime the sum is below 100% or sometime is even bigger than 100% (on both case there's a white space above to get to 100%). Deribit BTC Options Short-term/Long-term Ratio This graphs again splits the total trades between short term options and long term options. There's no hint on what they mean by short term, but the fact that short term options are more actively traded could potentially mean the trading aspect of those instrument, as opposed to hedging purpouse, has more appeal to traders. Total BTC Options Open Interest AS i detailed on my thread on future ( Everything you wanted to know about BTC futures but were afraid to ask!) Open Interest is a concept often confused with volume. In reality open interest specify the amount of "Open Positions" on the exchange, or the sum of positions that will ultimately could potentially lead to a future settlement. From here we see again that Deribit is by far the most important exchange, with LedgerX and Bakkt Barely noticeable. Again, I do expect this to change in the near future. BTC Options Open Interest by Strike (kBTC) This graph breaks down the Open Interest by the various strikes each position is written on. Looking at this chart we have a glimpse of the strike levels where lies the more interest of the markets. Also, near expiries, large open interest position could act as "magnets" or "barriers" to BTC price, because the hedging positions of option market participants (even thou the total option volume should be a few times bigger to impact hte more liquid spot BTC market). BTC Options Open Interest by Expiry(kBTC) Same as of above, this time the Open Interest is split by the various expiries. Looking at this chart we have a glimpse of the maturity where lies the more interest of the markets. BTC Jan20 Vol As we have seen in the OP the volatility level is not constant for each strike. Here this graph tries to model an implied volatility skew out of the quoted prices. On the call side (the blue lines) we see the prices being consistently narrow, while on the puts the spread is narrow where the options are in the money, while it widens considerably for in the money puts. As the most actively traded options, i.e. the ones we can expect to have more reliable prices, are the out-of-the-money options, these options are the one we consider to fit a volatility smile: so on the right hand of the graph we use the call implied volatilities, while on the left part of the picture we use the puts implied volatilities. As you can see the sum of the two curves, represented by the black dotted line, is quite well shaped. Back Months Vol Vol These graphs are conceptually identical to the previous one, but they are actually reporting the implied volatilities on back months, or longer expiries. As traded volumes and liquidity here is lesser, the graphs are not really well shaped: basically there are no reasonable offers for many puts, so the Y-axis explodes causing the graph to be actually unreadable.

|

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

|

jostorres

|

|

January 05, 2020, 07:45:56 AM Merited by fillippone (2) |

|

This is really cool and I have to admit that this is one of the greatest things that has happened in the cryptocurrency community, though I have seen some news that relates to Bakkt that once made me lose interest in them, but as time goes on we will get to know the truth.

Option trading is really good and this is not the first time that I have been part of it, I have always made use of Robinhood platform which was a really good choice since its a free and no commission platform. There are also other good platforms that I have known, I stopped option trading a long time , but Im looking back into it.

|

| | .

.Duelbits│SPORTS. | | | ▄▄▄███████▄▄▄

▄▄█████████████████▄▄

▄███████████████████████▄

███████████████████████████

█████████████████████████████

███████████████████████████████

███████████████████████████████

███████████████████████████████

█████████████████████████████

███████████████████████████

▀████████████████████████

▀▀███████████████████

██████████████████████████████ | | | | ██

██

██

██

██

██

██

██

██

██

██ | | | | ███▄██▄███▄█▄▄▄▄██▄▄▄██

███▄██▀▄█▄▀███▄██████▄█

█▀███▀██▀████▀████▀▀▀██

██▀ ▀██████████████████

███▄███████████████████

███████████████████████

███████████████████████

███████████████████████

███████████████████████

███████████████████████

▀█████████████████████▀

▀▀███████████████▀▀

▀▀▀▀█▀▀▀▀ | | OFFICIAL EUROPEAN

BETTING PARTNER OF

ASTON VILLA FC | | | | ██

██

██

██

██

██

██

██

██

██

██ | | | | 10% CASHBACK

100% MULTICHARGER | │ | | │ |

|

|

|

The Sceptical Chymist

Legendary

Offline

Activity: 3332

Merit: 6826

Cashback 15%

|

|

January 05, 2020, 08:00:18 AM Merited by fillippone (3) |

|

Looks like a great summary of options, OP, though I didn't read the entire thing. I never traded options in the stock market and don't have any interest in doing so with bitcoin, so I pretty much know all I'm ever going to need to know about them--and options/futures/derivatives never interested me all that much. I'm of the Warren Buffett school of thought, whereby it's better to own a stock or bond or whatever rather than a derivative of the same.

But I'm sure there are people here who don't really know what options are all about, and it's good that you created this nice summary. It definitely gives you an idea of what goes on at places like Bakkt and the CME.

|

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

exstasie

Legendary

Offline

Activity: 1806

Merit: 1521

|

|

January 05, 2020, 08:27:02 AM Merited by fillippone (2) |

|

Great stuff, fillippone. I've been trading for nearly a decade and I've always avoided options due to the complexity underlying their market pricing. It'll take a while for this to sink in but I really appreciate the breakdown.

|

|

|

|

|

rijaljun

|

|

January 05, 2020, 08:33:04 AM Merited by fillippone (2) |

|

Options are a difficult instrument to trade. This is true on traditional markets, but this is even more true in a wild market like bitcoin.

TL:DR, but I love this statement. People should not doing option trading because it is more complicated, much harder and more risky than spot trading. It would be good to make this as a 'warning' cause we don't want people to lose their money at any trading. If anyone wants to try this, they must be ready for everything that could happen during the journey. |

|

|

|

drlukacs

Sr. Member

Offline

Offline

Activity: 854

Merit: 253

l0tt0.com

|

|

January 05, 2020, 09:41:10 AM Merited by fillippone (1) |

|

Wow, I really admire your understanding. I confess I am a young person and I often learn about the indicators to make money and rarely learn about the volumes of Bitcoin or the options. Now, after reading the entire article, I realized that this is a way for us to look at the whole picture of the market and look further. Thank you for taking the time to create this article so that everyone can understand more about Bitcoin.

|

| | | .

WHIRLWIND | | | █▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀█

█ ▄▄▄██▀▀▀▀▀▄▄ █

█ ▄▄██▀▀▄▄▀▀▀▀▀▄▄▄ █A

█ ▄██▀▄██▀▄▀▀▀ ▄▄ ▄▄▄▄ █

█ ███ ██▀▄▀ ▄▄▀▄▄ ▀█▄ █

█ ███ ███ █ ▀▄ █▄ ██ █

█ ███ ███ █ █ ██ ██ █

█ ███ ███ █ ▄▀ █▀ ██ █

█ ███ ██▄▀▄ ▀▀▄▀▀ ▄█▀ █

█ ▀██▄▀██▄▀▄▄▄ ▀▀ ▀▀▀▀ █

█ ▀▀██▄▄▀▀▄▄▄▄▄▀▀▀ █

█ ▀▀▀██▄▄▄▄▄▀▀ █

█▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄█ | | | .

No Fee Ultimate Privacy | | | | .

ANONYMITY

MINING CAMPAIGN | | | | | | .

MIX NOW | | | | |

|

|

|

|

Blitzboy

|

|

January 05, 2020, 10:49:49 AM Merited by fillippone (1) |

|

Well, it really is a useful knowledge. Now I understand why you have a huge amount of merit after 1 year of activity on this forum. I admire your understanding, I have just learned about the trading options recently, some of the options you have given here are completely new with me. Thanks for your great contribution, not only me but others also need topic like this from you. We have a big picture here to admire and learn.

|

| ..Stake.com.. | | | ▄████████████████████████████████████▄

██ ▄▄▄▄▄▄▄▄▄▄ ▄▄▄▄▄▄▄▄▄▄ ██ ▄████▄

██ ▀▀▀▀▀▀▀▀▀▀ ██████████ ▀▀▀▀▀▀▀▀▀▀ ██ ██████

██ ██████████ ██ ██ ██████████ ██ ▀██▀

██ ██ ██ ██████ ██ ██ ██ ██ ██

██ ██████ ██ █████ ███ ██████ ██ ████▄ ██

██ █████ ███ ████ ████ █████ ███ ████████

██ ████ ████ ██████████ ████ ████ ████▀

██ ██████████ ▄▄▄▄▄▄▄▄▄▄ ██████████ ██

██ ▀▀▀▀▀▀▀▀▀▀ ██

▀█████████▀ ▄████████████▄ ▀█████████▀

▄▄▄▄▄▄▄▄▄▄▄▄███ ██ ██ ███▄▄▄▄▄▄▄▄▄▄▄▄

██████████████████████████████████████████ | | | | | | ▄▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▄

█ ▄▀▄ █▀▀█▀▄▄

█ █▀█ █ ▐ ▐▌

█ ▄██▄ █ ▌ █

█ ▄██████▄ █ ▌ ▐▌

█ ██████████ █ ▐ █

█ ▐██████████▌ █ ▐ ▐▌

█ ▀▀██████▀▀ █ ▌ █

█ ▄▄▄██▄▄▄ █ ▌▐▌

█ █▐ █

█ █▐▐▌

█ █▐█

▀▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▀█ | | | | | | ▄▄█████████▄▄

▄██▀▀▀▀█████▀▀▀▀██▄

▄█▀ ▐█▌ ▀█▄

██ ▐█▌ ██

████▄ ▄█████▄ ▄████

████████▄███████████▄████████

███▀ █████████████ ▀███

██ ███████████ ██

▀█▄ █████████ ▄█▀

▀█▄ ▄██▀▀▀▀▀▀▀██▄ ▄▄▄█▀

▀███████ ███████▀

▀█████▄ ▄█████▀

▀▀▀███▄▄▄███▀▀▀ | | | ..PLAY NOW.. |

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 05, 2020, 12:41:31 PM |

|

Looks like a great summary of options, OP, though I didn't read the entire thing.

<...>

Great stuff, fillippone.

<...>

Options are a difficult instrument to trade. This is true on traditional markets, but this is even more true in a wild market like bitcoin.

TL:DR, but I love this statement. People should not doing option trading because it is more complicated, much harder and more risky than spot trading. <...> Thanks you guys for the appreciation! Yes, it was a long thread to read, but rest assured it was even longer to write! As I had to try to figure out the most important things to describe and explain, please let me know via comment which aspect you want me to dig a little bit more! |

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

1Referee

Legendary

Offline

Activity: 2170

Merit: 1427

|

|

January 05, 2020, 01:58:02 PM Merited by fillippone (2) |

|

I was always recommended to stay away from options by traders who are farther in every facet than I am, which I respected but I kept wondering what made options so complicated and risky to trade. This puts things into perspective and I thank you for that. It kinda makes me happy that I didn't proceed to mess with options despite their utility (utility only for those who understand their workings).

I'll just stay within the areas of trading I'm comfortable with. No point in taking on more risk and complicating the whole process of trading. Simplicity is worth a ton.

Bakkt should provide a similar explanation since their aim is to be a retail platform, but I'm pretty sure that they won't go that far because it may scare off a lot of people.

|

|

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 08, 2020, 12:47:46 PM

Last edit: May 16, 2023, 06:48:40 AM by fillippone |

|

Hello, CME made available the full specification of their BTC options. Of course we are talking about cash settled options here. Options on Bitcoin Futures |

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

|

lixer

|

|

January 09, 2020, 04:44:25 PM |

|

Option trading is really cool and there was a time I used to think that it was the same thing with stock trading and after a bit of research I got to understand that theres a difference between the both of them. Option traders benefit from variety of stock market outcomes as you have explained here.

I havent taken the time to dig into this option trading and understands how it really works, but Im going to do that soon, and thanks for taking your time write down all these, its not easy, not everyone can take out time to break it down like this.

|

|

|

|

|

sisule

|

|

January 10, 2020, 02:09:15 PM |

|

Option trading is really cool and there was a time I used to think that it was the same thing with stock trading and after a bit of research I got to understand that theres a difference between the both of them. Option traders benefit from variety of stock market outcomes as you have explained here.

I havent taken the time to dig into this option trading and understands how it really works, but Im going to do that soon, and thanks for taking your time write down all these, its not easy, not everyone can take out time to break it down like this.

Not always trading can give solution for getting profit because many beginner not understand about how to start trading with bitcoin and altcoin, they look just allowing what other said about which one have to buy and trade, they not really understand about way how to begin with trading and choose best coin can give much profit with their way in trading. |

|

|

|

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 10, 2020, 07:57:51 PM

Last edit: May 16, 2023, 06:47:55 AM by fillippone Merited by Micio (11), Last of the V8s (1) |

|

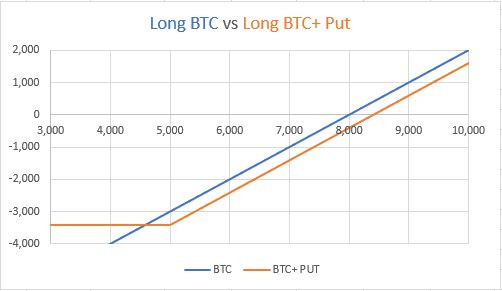

This is very interesting example, and one of the classic use case (wondering why I didn't add it to the OP). Basically a miner is exposed to Bitcoin price fluctuation. They have to pay huge costs in fiat (hardware cost is still anchored in USD -even if paid in BTC-, other costs are mainly paid in fiat (electricity, other costs, workforce etc). Their income is instead denominated in bitcoin. Miners are then forced to sell a certain amount of their BTC income to cover their fiat expenses. In case bitcoin goes up, they will be able to sell bitcoin higher for higher profit. In the opposite scenario they have to sell bitcoin lower to cover they cost, thus reducing their margins. Basically, they are LONG BITCOIN: their profits move with bitcoin price. Graphically the situation is the following. Today the price of bitcoin is USD 8,000. If BTCUSD goes to 10,000 they can sell this bitcoin for a USD 2,000 profit, compared to today. If BTCUSD goes to 5,000 they can sell this bitcoin for a USD 3,000 loss, compared to today. Basically their profit analysis is something like that:  At 8,000 they are at breakeven, they lose below USD 8,000 and they gain above. They are totally exposed to BTC price fluctuation, they get the swings on both sides. if a price goes up there is no problem, the miner can pay his bill, and enjoy the profit. If the price goes down, there are serious problems: not only the miner is forced to sell at loss to cover his expenses, but he will be forced to sell more BTC to cover the same amount of USD costs, forcing him into an a death spiral. The solution is buying an insurance, or buying a put. The miner pays a premium in every state of the world to cover himself from a negative outcome (BTC USD Price going down). The negative outcome is avoided with a payoff when the BTC USD goes below a certain level. This payoff is the put option we saw earlier: Put=max(0, Strike- BTC) In the example in the article, Bitmain embedded a MARCH 5000 put in the package (Bitmain sells the put to the miner, who buys it). In the OP I reported the JUN prices, so imagine the same structure , but on JUN expiry. The offer for a 5,000 PUT on JUN is 400 USD (399,97 for the nitpickers, let's round it). What happens at various levels of BTC price: Let's do some calculations. I prepared a sspreasheet with some levels:  At 3,000 BTCUSD being long the BTC would imply a loss of 5,000 USD. Having bough a PUT option would have implied an additional cost of 400 USD, and a positive payoff of 2000=max(0, 5,000-3,000), for a total of a-5,000-400+2,000= -3,400 At 5,000 BTCUSD being long the BTC would imply a loss of 3,000 USD. Having bough a PUT option would have implied an additional cost of 400 USD, and zero payoff as max(0, 5,000-5,000), for a total of a-3,000-400+0= -5,400 At 8,000 BTCUSD being long the BTC would imply a breakeven. Having bough a PUT option would have implied an additional cost of 400 USD, and a zero payoff as 0=max(0, 5,000-8,000), for a total of 0-400+0= -400 At 8,400 BTCUSD being long the BTC would imply a gain of 400 USD. Having bough a PUT option would have implied an additional cost of 400 USD, and a zero payoff as 0=max(0, 5,000-8,400), for a total of 400-400+0= 0 At 10,000 BTCUSD being long the BTC would imply a gain of 2,000 USD. Having bough a PUT option would have implied an additional cost of 400 USD, and a positive payoff of 2000=max(0, 5,000- 8,400), for a total of 2,000-400+0= 1,600 Summing up, the payoff would have been:  AS you can see , the miner , the buyer of the put options gives up a little bit of gain upside, to buy a protection in case of a lower catastrophic BTC price event. This is the typical example of an option bought for hedging purpose. Please note as the total payoff has a lower risk for the miner: the miner has decreased his risk using this derivatives: this is quite opposite of the mainstream version of derivatives as dangerous instruments. |

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

pugman

Legendary

Offline

Activity: 2383

Merit: 1551

dogs are cute.

|

|

January 10, 2020, 11:57:40 PM

Last edit: January 11, 2020, 12:08:41 AM by pugman |

|

Dude this is amazinnnngggg!! Its a very good,elaborated and a very neat explanation of options. I didn't read through all the practical thingies you wrote, cause it will fuck with my brain, and thanks for the heads-up cause I am never gonna trade options cause it is definitely not something I would want to risk my money into. But the concept in general isn't quite so bad.

You did a phenomenal job in explaining the meaning of what options are, and how they work. Its not everyday where you see proper threads with proper explanations here on bitcointalk.

I am still a little confused about the whole thing, I like understood it for a minute, and went like, wait hold on a minute, "How, what, HUH?" and its full Chinese noodles in my head :/

I am gonna read the whole thread again, for a hopeful better understanding. Seems interesting, not gonna lie.

|

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 13, 2020, 09:25:06 AM

Last edit: January 13, 2020, 10:03:35 AM by fillippone Merited by El duderino_ (2), Vispilio (1) |

|

Gentle reminder: today CME is starting to trade option: CMEs Bitcoin Options Launch Today, Heres What To ExpectCME recently announced the launch of its newest product that will allow customers to trade options on Bitcoin futures. Its scheduled for release today, January 13th. Some believe that it will attract further attention from institutional investors.

In fact, a group of JP Morgan analysts, led by Nikolaos Panigirtzoglou, expressed their views on the matter. He noted that the total interest towards CME has grown with almost 70% from year-end. This could be coming as a result of the options contracts:

There has been a step increase in the activity of the underlying CME futures contract. This unusually strong activity over the past few days likely reflects the high anticipation among market participants of the option contract.

Its worth noting that Bakkt, the Bitcoin Futures trading platform of the Intercontinental Exchange (ICE), previously launched Bitcoins monthly options. Panigirtzoglou acknowledges this, but he doesnt consider Bakkts volume to be sufficient enough at the moment, calling it rather small. The researchers believe that since CME has been more dominant in the Futures market, its options on Bitcoin will have a more significant impact.

Indeed Bakkt has been quite downbeat about their launch, and data on skew.com have struggled to show any relevance of their option volume. So yes, I think the BAkkt launch has been quite disappointing. EDIT: Apparently a block trade already went trough: 5 options maturing on FEB 20 (expiry 28 Feb 2020) 8,500 strike went togh at a level of 630, corresponding to an implied level of 65.15% with the future at 8220. This implied level is totally compatible with the one observed on deribit. Nice! |

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

Saint-loup

Legendary

Offline

Activity: 2604

Merit: 2353

|

|

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 13, 2020, 11:14:22 AM |

|

Thank you for these updates.

Very interesting seeing new competition in the market heating up.

Of course one big question mark is the accessibility of these markets for institutional and private customers and their adherence to KYC/AML regulations.

Deribit is having some issue on the matter as we speak and they are going to transfer to Panama (effectively cutting out every institutional clients.

Ps. Out of merits now! Will provide as soon as I get some!

|

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 13, 2020, 01:02:04 PM |

|

Some more detail on FTX. Crypto Derivatives Exchange FTX Launched Bitcoin Options TradingCryptocurrency derivatives exchange FTX has launched Bitcoin (BTC) options trading on Jan. 11.

FTX CEO Sam Bankman-Fried announced in a tweet yesterday that options were listed on the trading platform. Furthermore, later the same day he also claimed that options trading volume on the exchange reached $1 million in about 2 hours.

|

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 13, 2020, 06:17:04 PM

Last edit: May 16, 2023, 06:47:32 AM by fillippone |

|

Finally CME released a statement on Bitcoin Options: Options on Bitcoin futures are now live A new way to manage bitcoin exposure is here Options on Bitcoin futures are now available to trade on CME Globex, providing a new way for traders to diversify their trading strategy and manage bitcoin exposure. Based on actively traded Bitcoin futures, our new contract offers a cost-efficient tool to hedge uncertain markets. Bitcoin options at a glance: Regulated Reference Rate Track to the regulated and robust CME CF Bitcoin Reference Rate Counterparty risk mitigation Reduce counterparty default risk through CME Clearing Greater capital efficiency Save on potential margin offsets between Bitcoin futures and options Limited-time fee discount Effective through February 29, exchange fees for options on Bitcoin futures will be discounted by 50%. View fee schedule. Learn more about options on Bitcoin futures, including Frequently Asked Questions and contract specifications. Teey also released a quite interesting video: Trader's Edge video: options on Bitcoin futures

Join Dave Lerman as he walks through the highlights of the Bitcoin options contract, the importance of volatility, and the factors behind the success of the underlying Bitcoin futures in 2019.

Trader's Edge: Options on Bitcoin Futures

9 Jan 2020 By Dave Lerman Topics: General Education

Join Dave Lerman as he begins 2020 with a new Trader's Edge video, covering the January 13th launch of Bitcoin options.

This nine minute video covers:

The factors behind the success of the underlying bitcoin futures in 2019

Options Contract Highlights

How to use the QuikStrike tool for analysis of bitcoin options

The importance of volatility with options on bitcoin

Watch it here: Trader's Edge: Options on Bitcoin Futures |

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 14, 2020, 10:09:00 AM

Last edit: January 14, 2020, 10:32:13 AM by fillippone |

|

Quite a successful start for Bitcoin options trading at the CME: CME Bitcoin Options Trade $2.3M in Debut, BTC Price Hits 2-Month HighBitcoin (BTC) futures options from CME Group saw volumes in excess of $2.3 million on the products first day of public trading, the company has confirmed.

Data from CMEs official website confirmed the successful rollout on Jan. 13, which began as scheduled and ultimately saw 55 contracts change hands. On an andedoctical record, there are the structures traded according to skew:

Looks like 55 contracts went through on CME's BTC Options first day of trading, approx. $2.3mln notional.

100% were Calls.

Source: CME (preliminary estimates)

https://twitter.com/skewdotcom/status/1216867057670795267?s=21 |

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 14, 2020, 12:43:02 PM |

|

LOL someone really bought 250$ a call for $10 000 in february?  Exactely. 65.20% implied vol. Not really high actually. Today volatility is even higher, so the price would have been higher (if we had the same BTC market as yesterday, being the volatility higher, the price of the ptions would have been higher too). I don't understand the volumes of the order book. It's for the bids and the asks? So when they write "1" it means there is only one bid or ask for this call...  PS: In fact these trades are only the Privately Negotiated Trades(PNT) according to this CME table Well, The order book is quite thin (not to use other denigratoy terms) right now. THose are actually offers on those options, and I think that are irrelevant as market liquidity. This for sure has pushed people wanting to test the market not to show prices on the engine, but "pre-arrange" the trade and the have it crossed on the exchange afterwards. |

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 14, 2020, 12:57:31 PM |

|

Anyway apparently everyone (but Bakkt) is trading options now! We crossed 3000BTC options volume in the last 24 hours! We are excited for the growth of the options market in 2020, and will continue to build FTX into the best place to trade them. 24H volume added to the top of the chart: https://ftx.com/optionsIn this graph a recap of volumes: In the last day, both

@CMEGroup

and

@FTX_Official

, two well-known but vastly different exchanges which both offer crypto asset derivatives, launched their #Bitcoin Options product. /1

https://twitter.com/AmunAG/status/1217041230829408256?s=20 Word of caution: Options Volumes are quaite an irrelevant metric. Open Interest is a more intresting metric, and also is very easy to "manifacture" appealing metrics. |

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 21, 2020, 11:36:52 AM

Last edit: January 21, 2020, 12:21:25 PM by fillippone |

|

Skew. com has finally added CME to their Open Interest Monitor for Bitcoin Options: Just added CME to our bitcoin options open interest radar 📡

Market on aggregate has already filled the gap from the December expiry

Growing!  https://twitter.com/skewdotcom/status/1219545917671530496?s=20 https://twitter.com/skewdotcom/status/1219545917671530496?s=20This is a very useful tool to monitor market activity, far beeeter than trading volumes. As stated in the OP is difficult to invert market trands from here thou. Edit: Someone at cointelegraph is reading this thread: CME Bitcoin Options Volume Doubles One Week After Launch, Hits $5.3MBitcoin (BTC) options from CME Group more than doubled their traded volume in the first week after going live, data shows.

According to figures supplied by the company, Bitcoin options volumes skyrocketed in the seven days since they went live on Jan. 13.

BTC futures options surge higher

As of Jan. 17, volume was 122 contracts, worth 610 BTC ($5.27 million). By comparison, on day one, volume was 55 contracts, or 275 BTC (currently worth $2.37 million).

Open interest on options stood at 219 contracts on Friday, equivalent to 1,095 BTC ($9.45 million).

|

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 21, 2020, 10:37:21 PM |

|

When I said option can lead to gains even if markets doesnt move to in-the-money region, I was referring also to this: arbitrage. We are still in the first days of options market making, so we can find some gems like this one:

Short on deribit for $77 + long on ftx for $41? Arbitrage anyone?

https://twitter.com/ceterispar1bus/status/1218639096853086208?s=21 https://twitter.com/ceterispar1bus/status/1218639096853086208?s=21What are we looking at? The same MAR 20 18,000 Call on two different market. On Deribit the quote is 77.29 bid to 95.48 offer. On FTX the same options is offered at 41 USD. The plan is then to sell the options on FTX and buy back the same option on Deribit. Maximum size is 50. So we sell 50 18,000 MAR20 CALLS@77 on Deribit, cashing in 3,850 USD in premium. We also pay 41 for 50 18,000 MAR20 CALLS on FTX, paying 2,050 USD in premium. As we bought and sold the same option, we have no open risk, but we actually cashed in 1,800 USD in profit, as premium difference. Wonderful, isnt it? There are at least a couple of things to consider: - Margins. Opening a short position (on Deribit in this case, involves an unlimited loss. So exchanges are requiring huge capital allocated as margin to cover unrealised loss. At certain levels they even could pull the trigger on loss incurring positions, Id not properly covered by additional margins. This adds a layer of complexity, leaving us of the choice of posting more margins on the exchange (if we have enough liquidity) or immediately close the mirror position on FTX cashing in the positive payout. in this case the two positions must be closed at the same time not to incur in p&l swings (either positive or negative).

- Expiry dates. the two options are not exactly identical. The option on Deribit it is actually a day shorter than the one on FTX. So if we take this trade to expiry we have a mismatch. In this case it is a good mismatch because we bought the longer option, leaving us without downside. We can either let the time pass until expiry, or even sell the option for a premium (if in the money). In the opposite case we should consider the eventual cost to close the position, buying the one day option because there, selling the longer option, would have left us with an infinite downside.

- This trade looks good, maybe too good. Two market makers are pricing too differently the forward volatility of bitcoin and one of the two is going to be rekkt by the end of month.

Disclaimer: I am not registered on FTX, I assumed good faith of the person who posted this example and didnt check the reality. Its anyway a good textbook example on how to use options. |

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 23, 2020, 10:14:09 PM

Last edit: May 16, 2023, 06:43:15 AM by fillippone |

|

Regarding the above example we can try to figure out what the above arbitrage is equivalent in terms of implied volatility. As we can see from the figure, the Implied volatility on Deribit is quoted as the following: BID: 89.6% OFFER: 93.3% The option calculation at http://www.option-price.com/implied-volatility.phpconfirms those calculations:  (some roundings here) On FTX instead the offfer in terms of volatility is 79.98%:  Please note there is one added day to expiry. This means that we arbitraged almost 10% volatility spread when the bid- offer is less than 4%. This is huge. |

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█

█

█

█

▄▄▄▄█ | | |

|

|

|

VB1001

Legendary

Offline

Activity: 938

Merit: 2540

<<CypherPunkCat>>

|

|

January 25, 2020, 06:06:36 AM Merited by fillippone (2) |

|

Effect of CME Futures Options on BTC Price Depends on HalvingIt shows the confidence CME has in the Bitcoin market

CME, as a multi-billion dollar derivatives company, has no incentive to push for Bitcoin options and other investment vehicles if there simply is no traction or demand from the market. As the companys executive Tim McCourt said, CMEs Bitcoin futures market facilitated around $270 million per day:

Were pleased our CME Bitcoin futures have rapidly evolved over the last two years to become one of the most liquid, listed Bitcoin derivatives products in the world, averaging nearly 6,400 contracts (equivalent to 31,850 Bitcoin) traded each day in 2019.

31,850 BTC at the current price of $8,500 is equivalent to $270 million and that is similar to the spot volume of major exchanges in the global market. https://cointelegraph.com/news/effect-of-cme-futures-options-on-btc-price-depends-on-halvingAccording to CME Group, the good figures for a recent market with the participation of Bitcoin will continue to increase interest in the BTC futures and options market, since the article says that it remains to be seen whether the institutional market will influence before or after the Bitcoin value in the period of halving. Soon the doubts will be cleared, there are 108 days left for halving.

|

1PCm7LqVkhj4xRpKNyyEeekwhc1mzK52cT

|

|

|

|

HabBear

|

|

January 25, 2020, 03:33:45 PM |

|

Word of caution.

Options are a very complicated topic.

I tried my best effort to explain this topic in the most simple and intuitive way.

This is an incredible overview! All of it is accurate and there's enough information here for it to be considered a course on the investment security that is "options". All of this information applies well beyond Bitcoin. With options, you can [insert specific investment here]. The first question I (and perhaps others) have is... If we're a first time option buyer, how do we make sense of all of your knowledge to make our first move? How do we get started? Assuming one already has their account established, I think the best option play for a first timer is to choose one direction of the price - will it go up or will it go down? And then buy 1 options contract to call or put the price (above or below) the current price, maybe with a 1 month time horizon. Would this be a fair way to get started? |

|

|

|

|

fillippone (OP)

Legendary

Offline

Activity: 2156

Merit: 15459

Fully fledged Merit Cycler - Golden Feather 22-23

|

|

January 25, 2020, 04:30:58 PM |

|

<...>

Last thing I want is getting people trading options because they read this two pages. With this post I just scratched the surface, while deeper technical topics remain uncovered (anyone fancy explanation on delta bleed and cross vega exposures?). If you want to use options to bet your money one positive aspect is that you know how much you will lose at maximum (option premium). I would strongly recommend start paper trading options, and only later starting buying 1 option as a bet. Option selling or more complex structures are more advanced, and should be approached with a little bit of patience. Same thing for some more complex trading style different from buy your option and hodl until expiry. |

.

.HUGE. | | | | | | █▀▀▀▀

█

█

█

█

█

█

█

█

█

█

█

█▄▄▄▄ | ▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀▀

.

CASINO & SPORTSBOOK

▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄▄ | ▀▀▀▀█

█

█

█

█

█

█

█

█